European and US equities rebounded yesterday, as a South African doctor said that the symptoms of the new COVID variant were so far mild. However, today, Moderna's (NASDAQ:MRNA) CEO noted that there might be a material drop in vaccine effectiveness against the new strain, reviving concerns.

Today, Fed Chair Powell testifies before the Senate Banking Committee, and we are eager to find out whether the new COVID variant will affect the Fed's future course of action. Eurozone's preliminary inflation data for November are also due to be released.

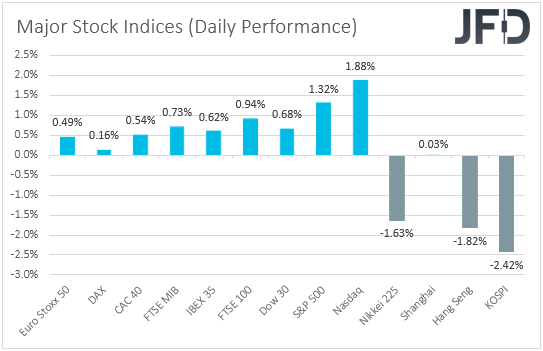

EU and US Equities Rebound, but Appetite Deteriorates Again Today in Asia

The US dollar traded higher against the majority of the other major currencies on Monday and during the Asian session Tuesday. It gained versus NZD, AUD, and CAD in that order, while underperformed versus CHF, EUR, and JPY.

The strengthening of the US dollar and the other safe havens, yen, and franc, combined with the weakening of the risk-linked Kiwi, Aussie, and Loonie, suggests that markets may have continued trading in a risk-off manner following Friday's sell-off.

However, turning our gaze to the equity world, we see that this was not the case. EU and US indices were a sea of green, though sentiment deteriorated again today in Asia.

We believe that the rebound during the EU and US sessions may have been triggered by comments from a South African doctor that the Omicron COVID variant symptoms were so far mild and could be treated at home. Later in the day, US President Joe Biden said that fresh lockdowns due to the new variant were off the table, for now, adding to the investor relief.

In our view, all this shows how sensitive market participants still are when it comes to the coronavirus and its new variant. We believe that this will be the central theme for a while more. With that in mind, we are very reluctant to say that market concerns have diminished and that yesterday's rebound is the beginning of a long-lasting recovery.

Any new negative headline has a high chance of resulting in another leg of massive selling. Indeed, at the time of writing, news hit the wires that Moderna CEO said that there would be a material drop in vaccine effectiveness against Omicron.

We believe that following the subdued sentiment during the Asian session could result in further deterioration. We see the case for European and US indices to reverse south as early as today.

DAX – Technical Outlook

The German DAX traded slightly higher yesterday, but today, the index's futures tumbled again, suggesting that more selling may be looming as early as today. This was reflected in our cash index, which fell slightly below Friday's low of 15030.

Although it rebounded back above that line, the price structure remains of lower lows and lower highs, and thus, we would consider the short-term picture to be still negative. We believe another attempt below 15030 could result in a slide towards the 14815 barrier, which is marked as a support by the low of Oct. 6.

If the bears are not willing to stop there, then a lower break could extend the fall towards the 14515 territory, defined by the lows of Mar. 23 and 24. To start examining whether the bulls have gained complete control, we would like to see a strong recovery back above 15745, marked by the inside swing low of Nov. 24.

The index will already be well above the downside resistance line taken from the high of Nov. 19, and we may see advances towards the high of Nov. 25, at 15965. Another break, above 15965, could encourage extensions towards the 16090 barrier, marked by the inside swing low of Nov. 19, or the peak of Nov. 22, at 16205.

Fed Chief Powell Testifies, Eurozone Cpis Enter the Spotlight

Yesterday, besides headlines surrounding COVID, we also got Powell's testimony which he will present before Congress today and Wednesday. The Fed Chief expressed concerns over the Omicron variant, saying that it muddies the outlook.

Although he did not refer directly to the Fed's monetary policy plans, he said that the new strain poses downside risks to employment and economic activity and increases inflation uncertainty. We will closely monitor today's Q&A session after he testifies before the Senate Banking Committee for more evident clues about how the new variant can affect the Fed's future course of action.

According to the Fed funds futures, markets still expect the first rate increase to be delivered in August. If Powell keeps that option on the table, the dollar could resume its latest uptrend against most of its major peers, especially the risk-linked ones.

However, deep declines could be possible if Powell suggests that he and his colleagues adopt a more cautious stance moving forward. We will get to hear from several other Fed officials during the week, including Vice Chair Richard Clarida, and we are eager to find out whether they have changed their minds or not.

Today, ahead of Powell's testimony, we get Eurozone's preliminary inflation numbers for November. The headline rate was +4.9% YoY from +4.1%, while the HICP excluding energy and food rate moved up to +2.6% YoY from +2.1%.

That said, bearing in mind that Germany's harmonized rate jumped to +6.0% YoY, we see the case for the headline rate of the bloc as a whole to rise by more than anticipated as well. However, with Europe adopting new restrictions due to the fast-spreading coronavirus and its latest variant, we don't expect ECB officials to start thinking about tightening monetary policy anytime soon.

After all, underlying inflation is expected to stay slightly above the bank's objective of 2%. At the same time, President Lagarde has repeatedly highlighted that tightening monetary policy now to rein in inflation could choke off the euro zone's recovery.

On top of that, ECB Executive member Isabel Schnabel said yesterday that the central bank believes inflation peaked in November, which adds to the narrative that it is premature for the Governing Council to start thinking about interest-rate hikes.

Therefore, even if the euro extends its latest recovery due to higher-than-expected numbers, we will not call for a bullish reversal. We will class this as a corrective advance.d

EUR/USD – Technical View

EUR/USD traded slightly higher yesterday after it hit support at 1.1258. After breaking the downside lien taken from the high of Nov. 9, the rate is now forming higher lows above the upside line drawn from the low of Nov. 24. Although in the bigger picture, it remains below the longer-term downside line taken from the high of May 25, the technical chart suggests that there is room for some further recovery for now.

A clear break above Friday's high, at 1.1330, will confirm a forthcoming higher high and may initially target the peak of Nov. 18, at 1.1375. Another break, above 1.1375, could extend the advance towards 1.1432 or 1.1465, whereas another break could allow the bulls to shoot for the 1.1524 zone. That zone acted as a strong floor between Oct. 6 and Nov. 5 before being violated by the bears on Nov. 10.

The outlook may turn back to negative upon a dip below 1.1258. This will confirm a forthcoming lower low on the 4-hour chart and may pave the way towards the low of Nov. 24, at 1.1185. If the bears are unwilling to stop there, we could see them pushing towards the 1.1100 territory, defined as a support by the low of Jun. 1.

Elsewhere

Besides Powell's testimony and Eurozone's inflation data, we also have Canada's GDP for Q3. Expectations are for the QoQ annualized rate to have rebounded to +3.0% from -1.1%, which, combined with a decent employment report on Friday, may increase speculation for a rate hike by the BoC soon.

Remember that Canadian policymakers unexpectedly ended their QE program at their latest gathering, maintaining an optimistic stance. It remains to be seen whether the Omicron variant will be a reason for changing plans.

Tonight, during the Asian session, Australia releases its GDP data for Q3, with the forecasts pointing to a 2.7% QoQ contraction after a 0.7% expansion the previous quarter. Despite market participants anticipating around three rate hikes next year, the RBA has been adamant that the timing suggested by market pricing is not the appropriate one.

Therefore, a negative GDP rate would add more credence to the bank's view that the earliest year for hiking rates may be 2023, thereby adding more pressure to the Aussie, which we expect as a risk-linked currency also to feel the heat of deteriorating broader market sentiment.