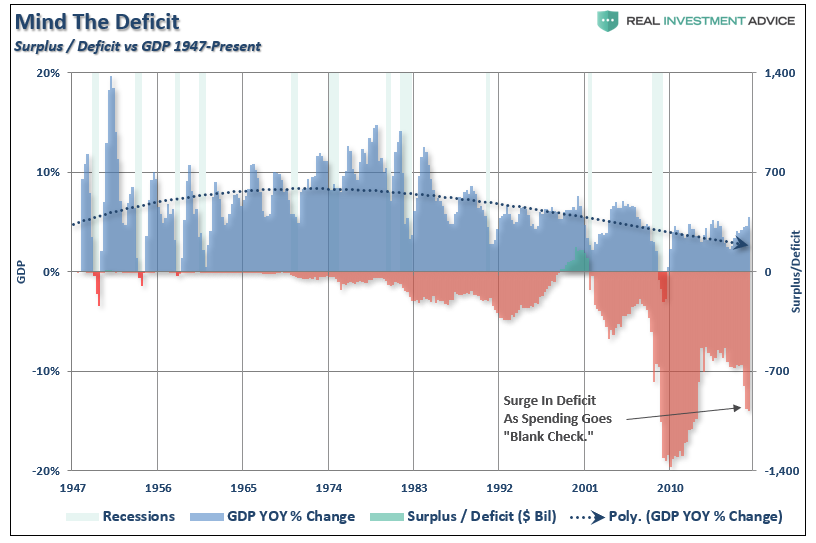

There has been a lot of angst lately over the rise in interest rates and the question of whether the government will be able to continue to fund itself given the massive surge in the fiscal deficit since the beginning of the year.

While “spending like drunken sailors” is not a long-term solution to creating economic stability, unbridled fiscal stimulus does support growth in the short-term. Spending on natural disaster recovery last year (3-major hurricanes and two wildfires) led to a pop in Q2 and Q3 economic growth rates. The two recent hurricanes that slammed into South Carolina and Florida were big enough to sustain a bump in activity into early 2019. However, all that activity is simply “pulling forward” future growth.

But the most recent cause of concern behind the rise in interest rates is that there will be a “funding shortage” of U.S. debt at a time where governmental obligations are surging higher. I agree with Kevin Muir on this point who recently noted:

“Well, let me you in on a little secret. The US will have NO trouble funding itself. That’s not what’s going on.

If the bond market was truly worried about US government’s deficits, they would be monkey-hammering the long-end of the bond market. Yet the US 2-year note yields 2.88% while the 30-year bond is only 55 basis points higher at 3.43%. That’s not a yield curve worried about US fiscal situation.

And let’s face it, if Japan can maintain control of their bond market with their bat-shit-crazy debt-to-GDP level of 236%, the US will be just fine for quite some time.”

That’s not a good thing by the way.

Let’s Be Like Japan

“Bad debt is the root of the crisis. Fiscal stimulus may help economies for a couple of years but once the ‘painkilling’ effect wears off, U.S. and European economies will plunge back into crisis. The crisis won’t be over until the nonperforming assets are off the balance sheets of US and European banks.” – Keiichiro Kobayashi, 2010

While Kobayashi will ultimately be right, what he never envisioned was the extent to which Central Banks globally would be willing to go. As my partner Michael Lebowitz pointed out previously:

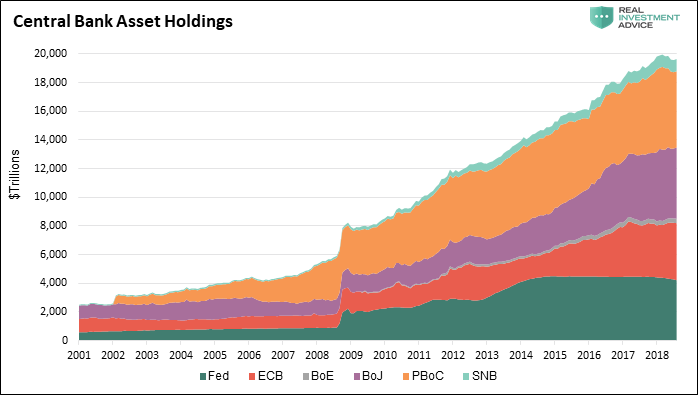

“Global central banks’ post-financial crisis monetary policies have collectively been more aggressive than anything witnessed in modern financial history. Over the last ten years, the six largest central banks have printed unprecedented amounts of money to purchase approximately $14 trillion of financial assets as shown below. Before the financial crisis of 2008, the only central bank printing money of any consequence was the Peoples Bank of China (PBoC).”

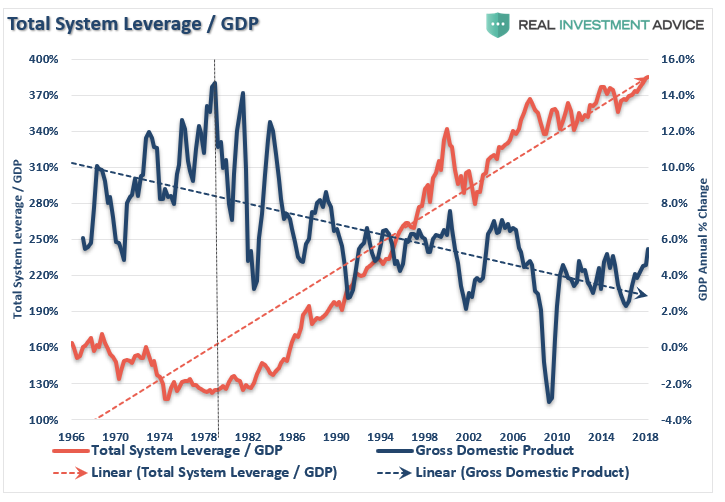

The belief was that by driving asset prices higher, economic growth would follow. Unfortunately, this has yet to be the case as debt both globally and specifically in the U.S. has exploded.

“QE has forced interest rates downward and lowered interest expenses for all debtors. Simultaneously, it boosted the amount of outstanding debt. The net effect is that the global debt burden has grown on a nominal basis and as a percentage of economic growth since 2008. The debt burden has become even more burdensome.”

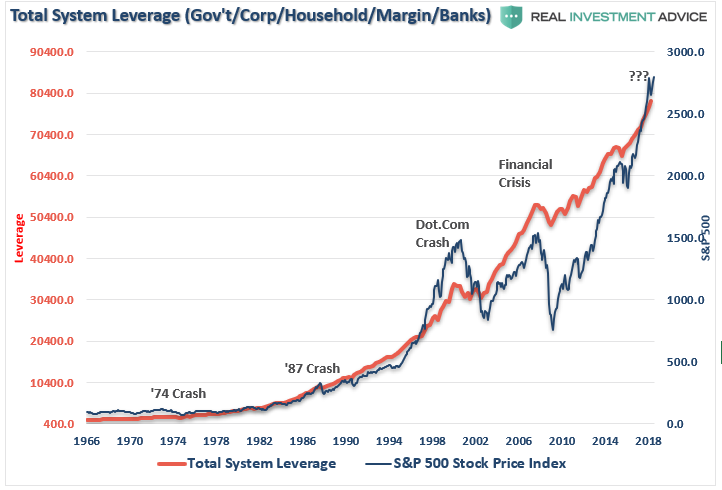

Not surprisingly, the massive surge in debt has led to an explosion in the financial markets as cheap debt and leverage fueled a speculative frenzy in virtually every asset class.

The continuing mounting of debt from both the public and private sector, combined with rising health care costs, particularly for aging “baby boomers,” are among the factors behind soaring US debt. While “tax reform,” in a “vacuum” should boost rates of consumption and, ultimately, economic growth, the economic drag of poor demographics and soaring costs, will offset many of the benefits.

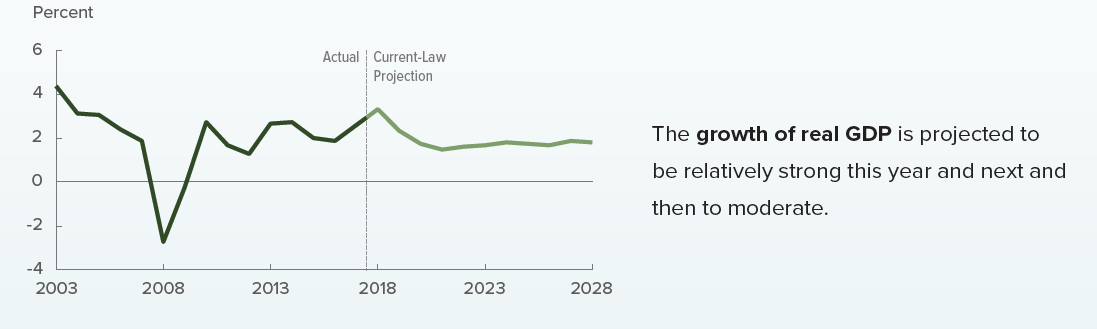

The complexity of the current environment implies years of sub-par economic growth ahead as noted by the Fed last week as their long-term projections, along with the CBO, remain mired at 2%.

The US is not the only country facing such a gloomy outlook for public finances, but the current economic overlay displays compelling similarities with Japan in the 1990s.

Also, while it is believed that “tax reform” will fix the problem of lackluster wage growth, create more jobs, and boost economic prosperity, one should at least question the logic given that more expansive spending, as represented in the chart above by the surge in debt, is having no substantial lasting impact on economic growth. As I have written previously, debt is a retardant to organic economic growth as it diverts dollars from productive investment to debt service.

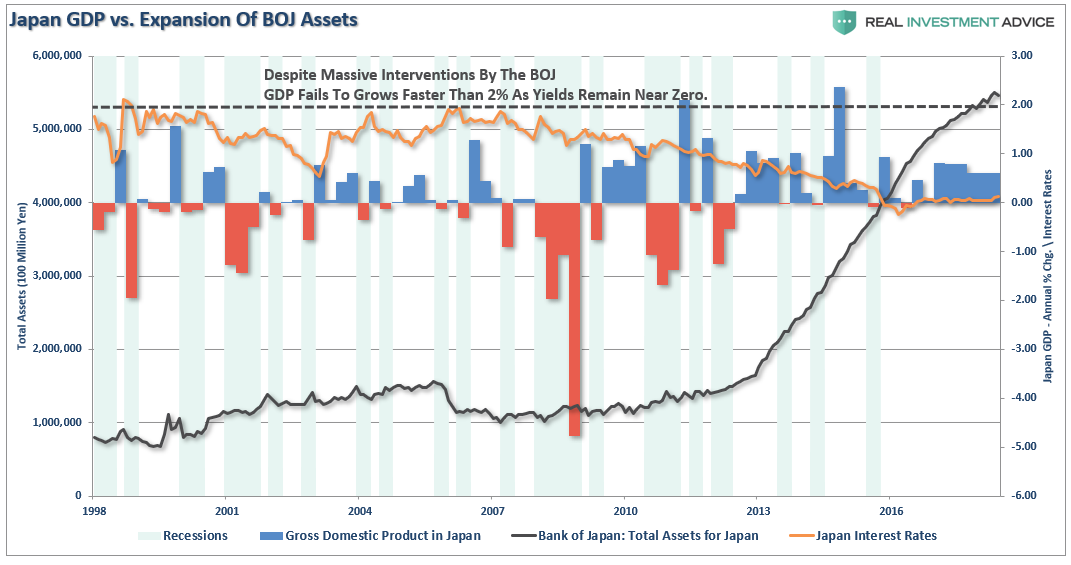

One only needs to look at Japan for an understanding that QE, low-interest rate policies, and expansion of debt have done little economically. Take a look at the chart below which shows the expansion of the BOJ assets versus the growth of GDP and levels of interest rates.

Notice that since 1998, Japan has not achieved a 2% rate of economic growth. Even with interest rates still near zero, economic growth remains mired below one-percent, providing little evidence to support the idea that inflating asset prices by buying assets leads to stronger economic outcomes.

But yet, the current Administration believes our outcome will be different.

With the current economic recovery already pushing the long end of the economic cycle, the risk is rising that the next economic downturn is closer than not. The danger is that the Federal Reserve is now potentially trapped with an inability to use monetary policy tools to offset the next economic decline when it occurs.

This is the same problem that Japan has wrestled with for the last 25 years. While Japan has entered into an unprecedented stimulus program (on a relative basis twice as large as the U.S. on an economy 1/3 the size) there is no guarantee that such a program will result in the desired effect of pulling the Japanese economy out of its 30-year deflationary cycle. The problems that face Japan are similar to what we are currently witnessing in the U.S.:

- A decline in savings rates to extremely low levels which depletes productive investments

- An aging demographic that is top heavy and drawing on social benefits at an advancing rate.

- A heavily indebted economy with debt/GDP ratios above 100%.

- A decline in exports due to a weak global economic environment.

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases to offset reduced employment

The lynchpin to Japan, and the U.S., remains demographics and interest rates. As the aging population grows becoming a net drag on “savings,” the dependency on the “social welfare net” will continue to expand. The “pension problem” is only the tip of the iceberg.

If interest rates rise sharply it is effectively “game over” as borrowing costs surge, deficits balloon, housing falls, revenues weaken and consumer demand wanes. It is the worst thing that can happen to an economy that is currently remaining on life support.

Japan, like the U.S., is caught in an on-going “liquidity trap” where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the ongoing battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments and risk begins to outweigh the potential return.

More importantly, while there are many calling for an end of the “Great Bond Bull Market,” this is unlikely the case for two reasons.

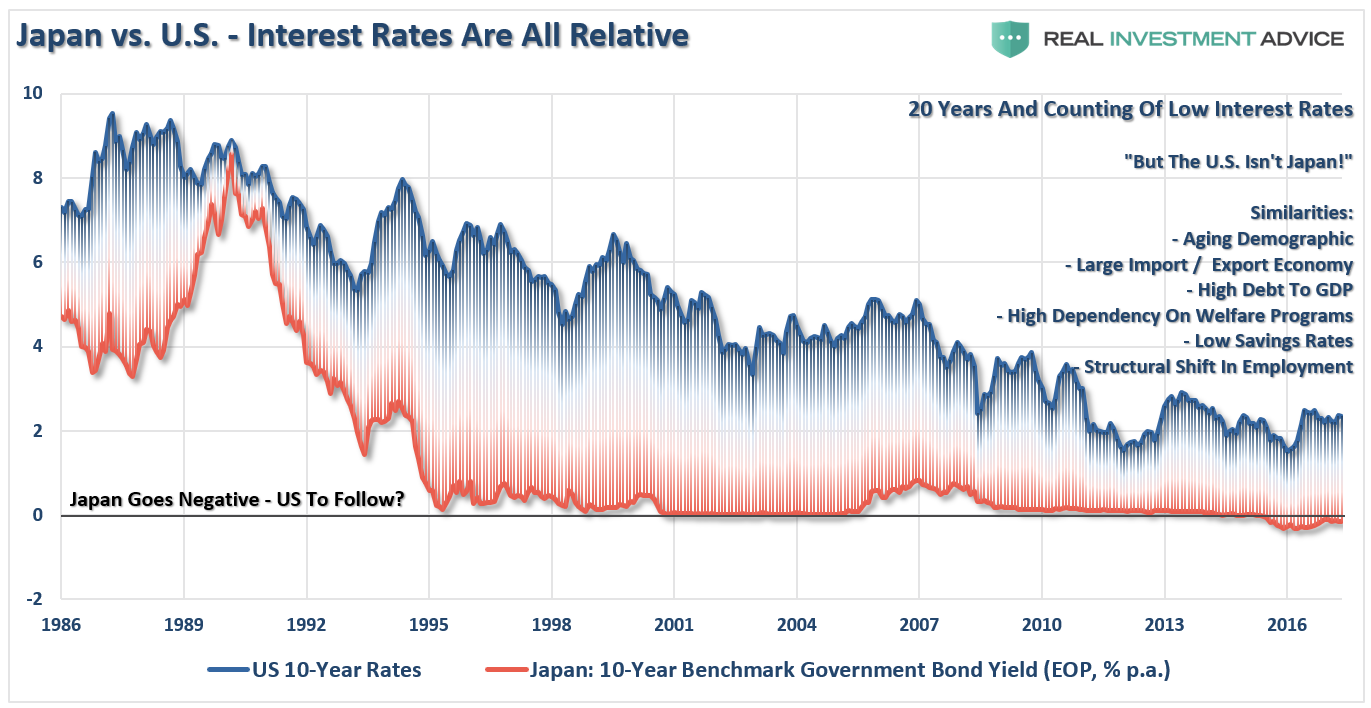

- As shown in the chart below, interest rates are relative globally. Rates can’t rise in one country while a majority of global economies are pushing low to negative rates. As has been the case over the last 30-years, so goes Japan, so goes the U.S.

- Increases in rates also kill economic growth which drags rates lower. Like Japan, every time rates begin to rise, the economy rolls into a recession. The U.S. will face the same challenges.

Unfortunately, for the current Administration, the reality is that cutting taxes, tariffs, and sharp increases in debt, is unlikely to change the outcome in the U.S. The reason is simply that monetary interventions, and government spending, don’t create organic, sustainable, economic growth. Simply pulling forward future consumption through monetary policy continues to leave an ever-growing void in the future that must be filled. Eventually, the void will be too great to fill.

But hey, let’s just keep doing the same thing over and over again, which hasn’t worked for anyone as of yet, but we can always hope for a different result.

What’s the worst that could happen?