The price of Gold is particularly important at this juncture for a number of reasons.

I have recently written of the decline in Gold's price and its significance with regard to "deflationary pressures," most recently in the June 10 post titled The Prospect Of Deflation as well as the May 20 post (seen on Doug Short's blog) titled The Recent Decline In Gold.

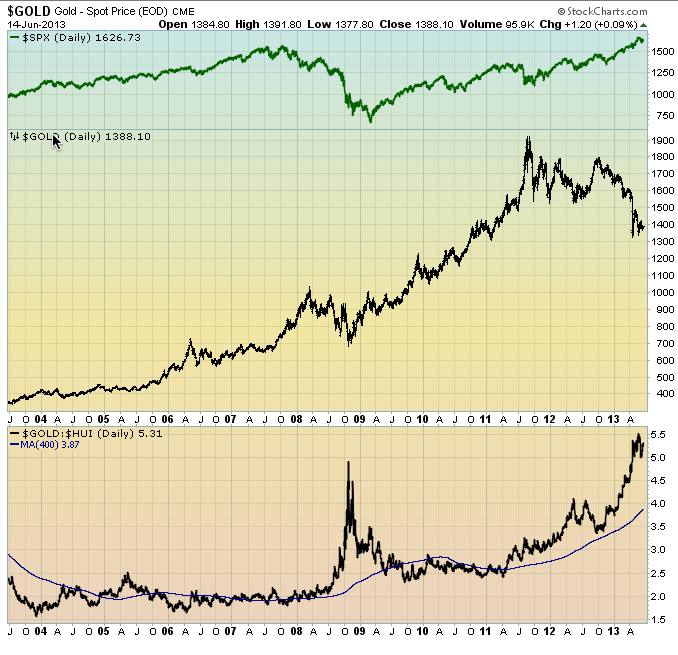

A daily price chart of Gold for the last 10 years (through June 14) is seen below. Gold's price is depicted in the middle plot of the chart, with the S&P 500's price seen above it (in green) and the Gold:HUI ratio on the bottom plot:

Vulnerable To More Decline

As one can see, Gold's recent price action appears to be in a downward consolidation, which appears particularly poor in light of the strong upward price movements of the S&P 500. From a variety of technical perspectives, it appears that Gold's price is vulnerable to further decline, likely substantial.

Further supporting the idea that Gold is vulnerable to a significant decline is the price of the HUI Index, if one assumes that Gold stocks augur the future price of Gold. As one can see in the bottom Gold:HUI plot, the 400-day moving average (the thin blue line) of the Gold:HUI ratio has been increasing since roughly mid-2011. I think that it is important to note that during Gold's advance from 2005 through mid-2011, this 400-day moving average (DMA) largely stayed in a range of roughly 2-2.5.

Potential Downside

As one can see, the ratio is at 3.87. If Gold were to decline back to the 2.5 level of the Gold:HUI 400-DMA, Gold would be at $651/oz, based upon a current HUI price of 260.55. (The 2.0 level of the 400-DMA would equate to a Gold price of $521.) While these Gold prices of $651 and $521 are simply rough projections, they do speak to not only a potential downside in Gold's price, but also to the potential magnitude of the "deflationary pressures" that may (likely) accompany such a strongly declining Gold price.

It should also be noted that various other commodities also exhibit poor "price action" and seeming further downside price vulnerability.

While I believe that Gold is influenced by many complex factors, as I wrote in my April 27, 2011 post (Reason's Behind Gold's Ascent), I continue to believe that Gold's greatest upside factor is that of a "safe haven."

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Gold’s Declining Price: What It Means

Published 06/17/2013, 03:38 PM

Updated 07/09/2023, 06:31 AM

Gold’s Declining Price: What It Means

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.