- Fed rate cut bets scaled back after upbeat US data

- Wall Street rally loses steam, dollar edges up as yields rebound

- Global growth worries and disappointing US-China summit also dent mood

Post-CPI euphoria fizzles out

Equities were muted while the greenback was broadly firmer on Thursday as the relief rally on the back of this week’s cooler-than-expected US CPI readings lost steam following some not-so-soft data yesterday. Treasury yields regained their footing to bounce higher from the CPI-led slump as stronger-than-expected retail sales and manufacturing figures undermined the market’s conviction that the Fed will begin slashing rates next year.

The US dollar rebounded from more than two-month lows against a basket of currencies while shares on Wall Street pared earlier gains to close only marginally higher.

But the reaction was nevertheless modest, and rate cut expectations were only slightly reduced, once again underscoring the fact that investors are quicker to price in rate cuts than to price them out. Although this inclination poses a significant risk to Wall Street’s impressive comeback from the depths of October’s five-month trough, yesterday’s data also supports the soft-landing narrative for the US economy, so there isn’t a case of doom and gloom in either scenario.

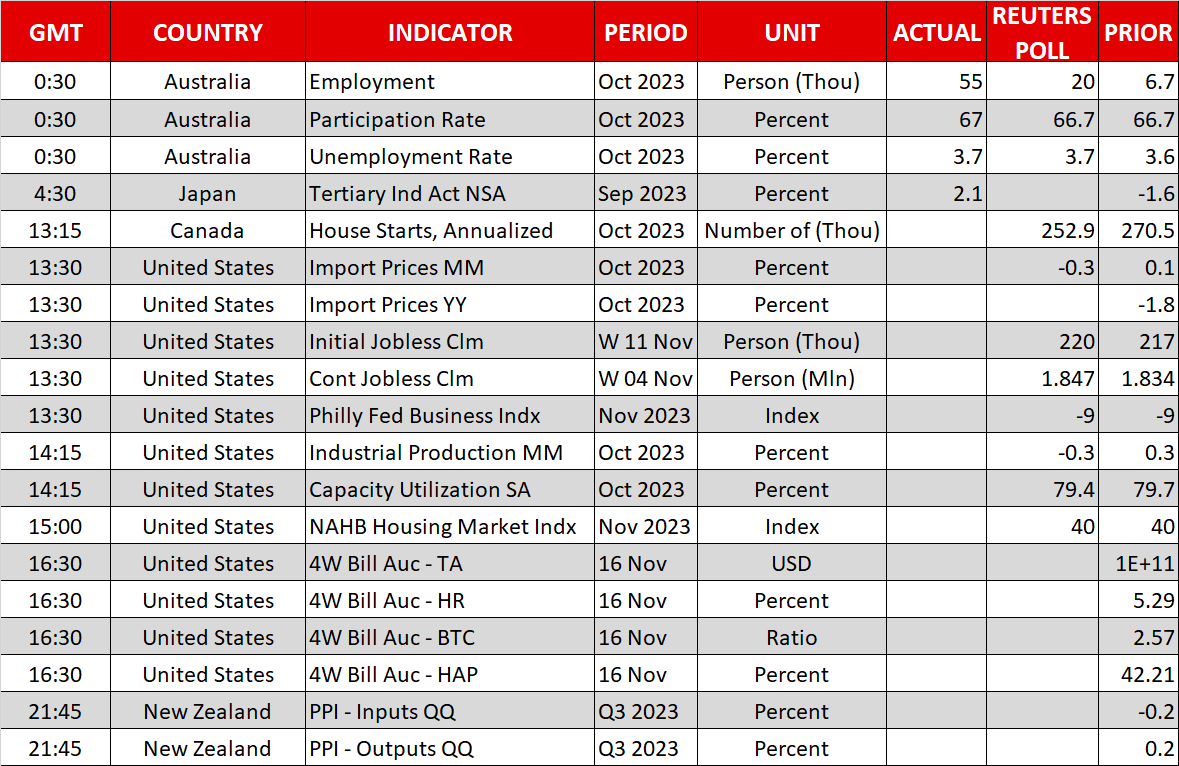

More data, Fed speakers and retail earnings on tap

However, a further pullback in stocks is possible today should the latest weekly jobless claims numbers as well as other data releases that will include the Philly Fed index and October industrial production also beat expectations. Investors will be on guard too for any policy related comments from the Fed’s Waller and Williams who are due to speak later in the day.

But as was the case on Wednesday, there could be some upside from the earnings front. Retailers are in focus this week and after Target’s strong results set the bar high yesterday, it will be Walmart’s and Macy’s’ turn to post their earnings before the market open. Alibaba’s earnings will also be watched.

Meanwhile, there’s been some relief for investors after Congress passed a stopgap spending bill that keeps the government funded at least until January 19.

China woes weigh on Asian stocks, aussie

In Asia, however, traders were not impressed by the outcome of the much-anticipated face-to-face meeting between the US and Chinese presidents at an APEC summit yesterday. Although Biden and Xi made progress on certain matters such as military cooperation, the talks marked only a slight thawing of relations between the two superpowers.

For Chinese investors, there was a lot more at stake from this meeting than for their US counterparts, as the country’s leaders are struggling to kickstart the stalled economy. Data out today showed the slump in the housing market deepened in October, pointing to a slow and long recovery ahead.

Chinese and Hong Kong indices underperformed while the China-sensitive Australian dollar slipped, though there was some support for the aussie from a bigger-than-expected jump in domestic employment in October.

Light at the end of the euro and pound tunnel?

Overall, the economic picture outside of the US isn’t looking particularly encouraging at the moment, with GDP contracting in both the Eurozone and Japan in the third quarter and China’s recovery still appearing very patchy.

If there is a silver lining, it is that inflation is firmly on the way down and for currencies such as the euro and pound, this may not be entirely negative. Both currencies suffered when fears of overtightening intensified. Now that inflation is seemingly coming under control for the ECB and Bank of England, recession risks are being priced out somewhat, cushioning the blow from rate cut expectations being brought forward.

This may also explain why the euro and pound rallied just as much as other majors when the US dollar plunged after the CPI report, with only the yen being a laggard.