WTI In A Consolidative Mode

IronFX Strategy Team | Nov 20, 2014 05:40AM ET

Fed minutes: Little desire to shift the language The minutes from the Fed October 28-29 FOMC meeting showed that policy-makers saw little reason to shift the language in the post-meeting statement. Over the “considerable time” phrase there were plenty of opinions and some participants preferred to eliminate language in the statement. These participants were concerned that such a characterization could be misinterpreted as suggesting that the Committee's decisions would not depend on the incoming data. However, other participants thought that the "considerable time" phrase was useful in communicating the Committee's policy intentions or that additional wording could be used to emphasize the data dependence of the Committee's decision process. I believe that since there was no press conference following the October’s meeting, it would be difficult for the Committee to remove this phrase without giving further clarifications. This could happen at their December meeting, which is associated with a press conference.

In discussing economic developments abroad, participants pointed to a somewhat weaker economic outlook and increased downside risks in Europe, China, and Japan, as well as to the strengthening of the dollar over the period. Nonetheless, many participants suggested that the share of external trade in the US economy is relatively small, thus the effects of changes in the value of the dollar on net exports are modest. Several participants also judged that the decline in the prices of energy and other commodities as well as lower long-term interest rates would likely provide an offset to the higher dollar and the weaker global growth. They argued that the US recovery remains on a stable path.

Market reaction was limited following the minutes, the S & P 500 jumped 0.30% at the release only to retreat in the following hour and end the day virtually unchanged from TUESDAY ’s closing. Major currency pairs reacted somewhat on the news, EUR/USD touched 1.2600 but fell back to take sideways, GBP/USD bounced briefly only to set aside the gains and gyrate around 1.5670. The USD/JPY was the only currency that kept its strength breaking above 118.00.

Overnight, the preliminary HSBC China manufacturing PMI fell to 50.0, down from the October final reading of 50.4 and below expectations of a decline to 50.2. The six-month low reading, just in between contractionary and expansionary levels added to concerns over the nation’s slowdown. The NZD and AUD weakened marginally at the release of the figure, but recovered immediately in the following minutes to trade unchanged against the dollar.

As for today’s activity, PMIs will take center stage. Eurozone’s preliminary PMIs, also for November, are released just after the figures from Germany and France are announced. The bloc’s manufacturing PMI is projected to remain above its 50 line, while the manufacturing PMI from its strongest economy, Germany, is anticipated to move slightly further into its expansionary territory. Eurozone’s preliminary consumer confidence for November is also due out.

In Norway, GDP for Q3 is expected to decelerate adding to the recent batch of poor data coming from the country.

In the UK, retail sales excluding gasoline are expected to have risen in October, a turnaround from the previous month.

Later in the day, we get the US preliminary Markit manufacturing PMI for November and the Philadelphia Fed business activity index for November. Existing home sales for October are also coming out and the forecast is for the figure to show a marginal decrease. Following Wednesday’s mixed housing data, existing home sales should shed some light in the recent housing activity. The CPI for October is forecast to have decelerated, adding to concerns whether the Fed is on track to meet its inflation target. Initial jobless claims for the week ended on Nov. 15 and the Conference Board leading index for October are also coming out.

We have three speakers on Thursday’s agenda. Riksbank Deputy Governor Martin Floden, ECB Executive Board member Yves Mersch and Cleveland Fed President Loretta Mester speak.

The Market

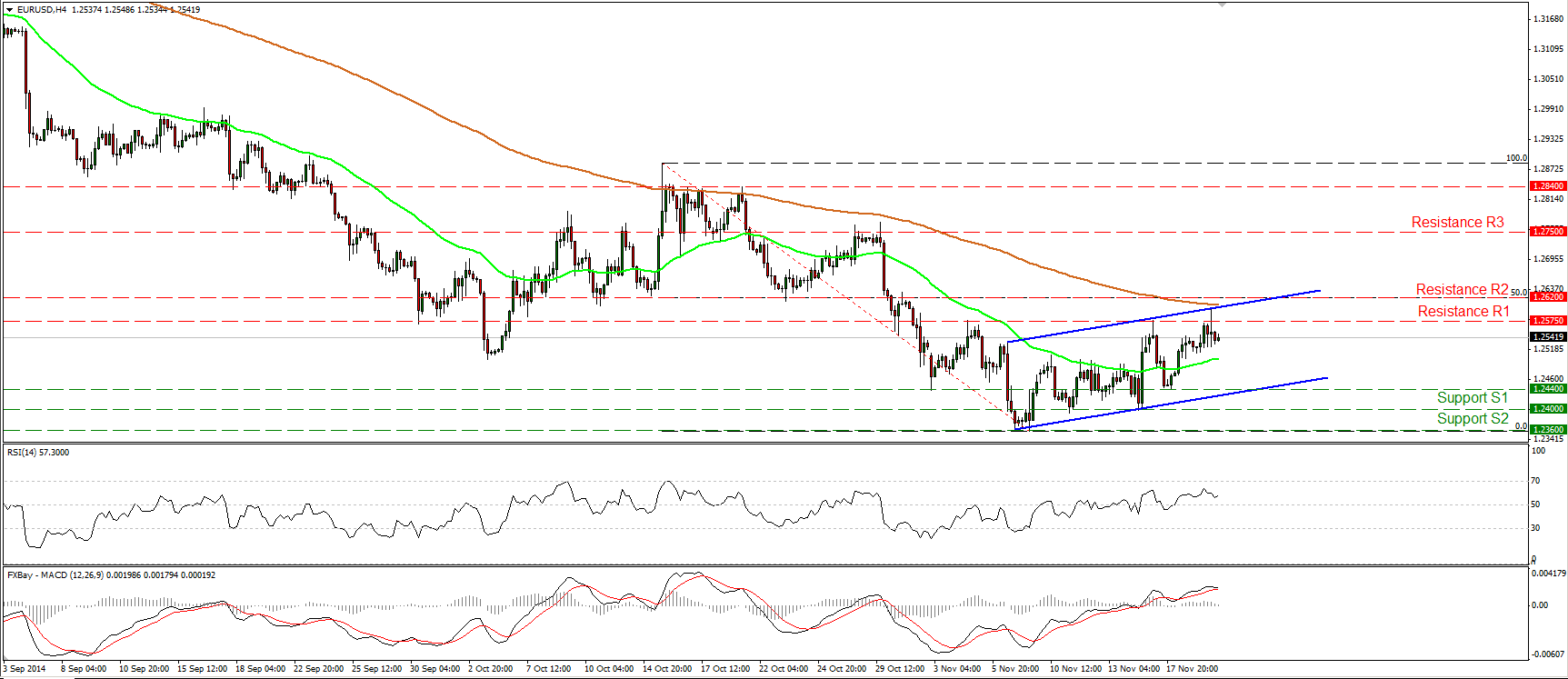

EUR/USD finds resistance at the upper bound of the channel

EUR/USD edged higher on Wednesday to find resistance near the 200-period moving average and the upper boundary of the blue upward sloping channel. I would stick to my neutral stance and I would treat the recovery from 1.2360 as an upside retracement of the longer-term down path. On the daily chart, although the price structure remains lower peaks and lower troughs below both the 50- and the 200-day moving averages, there is still positive divergence between both of our daily momentum studies and the price action. The positive divergence give me extra reasons to sit on the sidelines and wait for more actionable signs to convince me that the downtrend is back in force and likely to continue.

• Support: 1.2440 (S1), 1.2400 (S2), 1.2360 (S3)

• Resistance: 1.2575 (R1), 1.2620 (R2), 1.2750 (R3)

GBP/JPY breaks above 185.00

GBP/JPY continued its rally on Wednesday, exiting the sideways path it’s been trading since the beginning of the month and breaking above the psychological line of 185.00 (S1). I would now expect the move above 185.00 (S1) to see scope for larger bullish extensions and target the high of the 3rd of October 2008, at 189.00 (R1). Both our near-term oscillators violated their black downside resistance line and firmed up, designating strong bullish momentum. As long as the rate remains above the black uptrend line taken from back at the low of the 15th of October, and above both the 50- and the 200-period moving averages, the overall path of GBP/JPY stays to the upside in my view.

• Support: 185.00 (S1), 184.30 (S2), 181.00 (S3)

• Resistance: 189.00 (R1), 190.00 (R2), 192.00 (R3)

NZD/USD finds support at 0.7820

NZD/USD tumbled on Wednesday reaching the support line of 0.7820 (S1). A clear dip below that line could have larger bearish implications and perhaps open the way for our next support line at 0.7700 (S2). Our near-term momentum studies maintain a negative tone. The RSI moved lower after finding resistance slightly below its 50 line, while the MACD, already below its trigger line, obtained a negative sign. I also see negative divergence between both the indicators and the price action. In the bigger picture, the rate oscillates between the 0.7700 (S2) support zone and the resistance of 0.7980 (R1), thus I would maintain a neutral stance as far as the overall path of this rate is concerned.

• Support: 0.7820 (S1), 0.7700 (S2), 0.7660 (S3)

• Resistance: 0.7980 (R1), 0.8100 (R2), 0.8230 (R3)

Gold tumbles back near 1180

Gold fell sharply yesterday, finding support near the 1180 (S1) line and the 50-period moving average. A clear move below 1180 (S1) is likely to trigger extensions perhaps towards the 1160 (S2) barrier and the lower line of the black upside channel. Taking a look at our short-term oscillators, I see that the RSI fell near its 50 while the MACD has topped and crossed below its signal line. Moreover, both of the indicators violated their black upside support lines. As for the broader trend, I still see a longer-term downtrend. Hence I would treat the recovery from 1132 as a corrective move for now. In the absence of any major bullish trend reversal signal, I would prefer to adopt a “wait and see” stance as far as the overall outlook of the precious metal is concerned.

• Support: 1180 (S1), 1160 (S2), 1146 (S3)

• Resistance: 1205 (R1), 1222 (R2), 1235 (R3)

WTI in a consolidative mode

WTI moved in a consolidative manner on Wednesday, staying between the support line of 73.35 (S1) and the resistance of 76.00 (R1). I still believe that the near-term outlook remains negative and I would expect a clear move below the support obstacle of 73.35 (S1) to confirm a forthcoming lower low and perhaps set the stage for extensions towards our next support at 71.00 (S2), defined by the lows of July and August 2010. In the bigger picture, the price structure on the daily chart remains lower peaks and lower troughs below both the 50- and the 200-day moving averages, keeping the overall downtrend intact.

• Support: 73.35 (S1), 71.00 (S2), 70.00 (S3)

• Resistance: 76.00 (R1), 78.00 (R2), 80.00 (R3)

BENCHMARK CURRENCY RATES - DAILY GAINERS AND LOSERS

MARKETS SUMMARY

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.