Why Alphabet May Be the Most Misunderstood Big Tech Stock

Masoud Movafaghi | Jul 11, 2025 11:06AM ET

In a market dominated by enthusiasm around AI and tech giants, Alphabet Inc Class A (NASDAQ:GOOGL) appears strangely underappreciated. Despite strong fundamentals and dominant market positions, the stock has trailed behind some of its peers like Nvidia (NASDAQ:NVDA), Microsoft (NASDAQ:MSFT), and Amazon (NASDAQ:AMZN) over the past year.

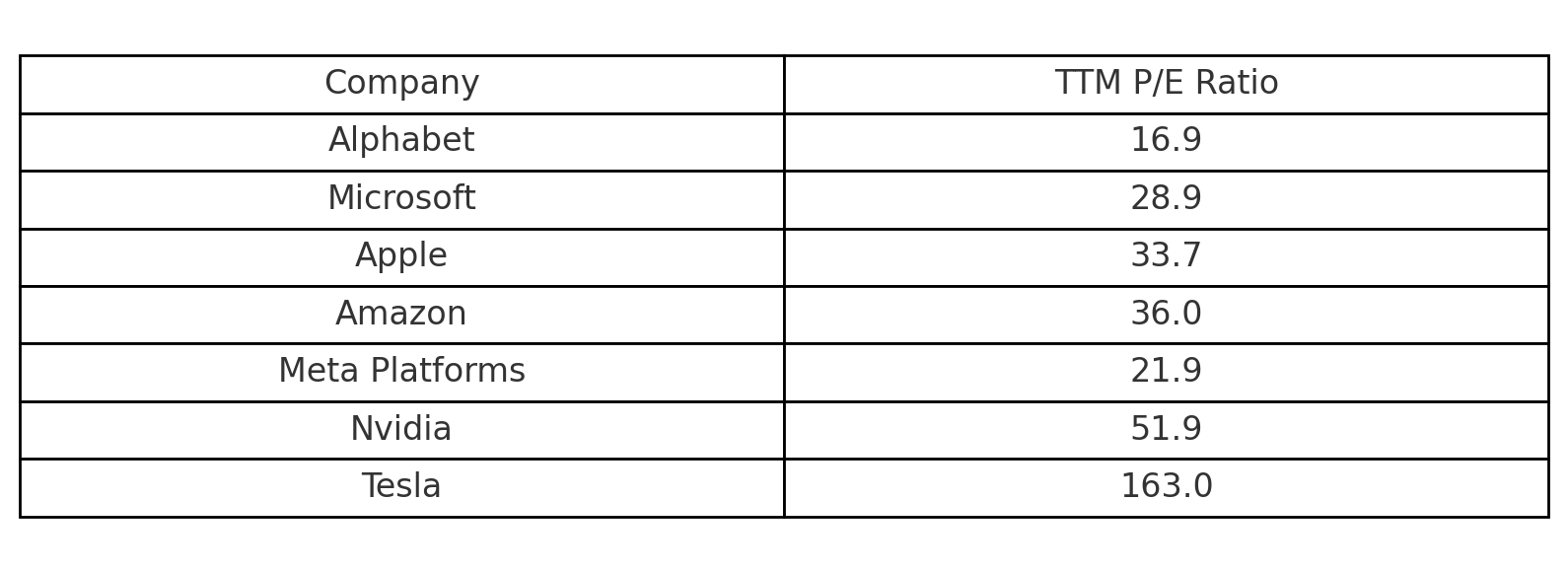

Among the so-called Magnificent Seven tech giants, Alphabet stands out as the most undervalued by a wide margin. It currently trades at a trailing P/E of approximately 16.9, far below Microsoft (~29×), Apple (NASDAQ:AAPL) (~34×), Amazon (~36×), Meta (NASDAQ:META) (~22×), and significantly cheaper than Nvidia (~52×) and Tesla (NASDAQ:TSLA) (~163×). But the discount doesn't end there. On a Price-to-Book (P/B) basis, Alphabet trades at roughly 6×, while peers like Microsoft (~11.6×), Apple (~7.9×), and Nvidia (~47×) command far higher multiples. This dual undervaluation—on both earnings and asset basis—makes Alphabet a clear outlier.

Alphabet reported stronger-than-expected second-quarter results, with key metrics delivering upside surprises across the board:

- Revenue rose approximately 12% year-over-year, reaching around $90.2 billion, exceeding the consensus forecast (~$89.2 billion).

- Net income surged to approximately $34.5 billion, up about 46% YoY, far above analysts’ expectations (~$24.8 billion)

- Earnings per Share (EPS) came in at an estimated $2.01–$2.04, implying a solid increase from Q2 2024 and topping forecasts

Segment Roll-Outs & Growth Drivers

Advertising (about 75% of total revenue) grew 8.5% to ~$66.9 billion, slightly outperforming expectations (~7.7%)—boosted by AI-powered products like AI Overviews, now serving 1.5 billion users monthly.

Google Cloud continued its strong momentum with 28% growth, reaching around $12.3 billion in revenue. Enterprise adoption of AI tools remains the primary tailwind.

Strategic Moves & Capital Allocation

Share buyback program was significantly expanded: Alphabet unveiled a $70 billion repurchase initiative, reinforcing its long-term shareholder value framework.

The company reaffirmed its robust commitment to innovation, targeting $75 billion in capital expenditure through 2025, largely dedicated to AI infrastructure and R&D.

The company simultaneously announced a $70 billion share buyback and reaffirmed $75 billion in capital spending, signaling both financial strength and long-term ambition.

But does this relative underperformance reflect a weakening business—or a rare investment opportunity?

Alphabet currently trades at a forward P/E ratio significantly below that of Microsoft and far below Nvidia. While Nvidia is priced for extreme AI-driven growth, Alphabet's valuation suggests the market is pricing in stagnation or even decline. That view ignores a few key facts:

- Alphabet’s (NASDAQ:GOOGL) core business is still highly profitable, with operating margins above 25%.

- The company holds over $100 billion in cash and equivalents.

- It continues to repurchase shares aggressively, enhancing long-term shareholder value.

In short, you’re getting a world-class company at a reasonable price—something rare in today’s tech sector.

The “Search Is Dead” Narrative Is Overblown

Much of the skepticism around Alphabet centers on fears that AI tools like ChatGPT or Perplexity will erode Google’s dominance in search. But let’s look at the facts:

- Google still controls over 90% of global search traffic.

- Most user queries are transactional, local, or navigational—areas where Google still offers the fastest, most relevant results.

- Shifts in user behavior take years to materialize at scale. Despite the rise of AI assistants, there is no data suggesting mass migration away from Google Search.

Moreover, Alphabet is actively adapting through Search Generative Experience (SGE), integrating AI into its core products with vast computing infrastructure and proprietary data advantages that very few companies can match.

Untapped Growth Engines Beyond Search

While Search and Ads are the core of Alphabet, the company has multiple underappreciated growth drivers:

- YouTube Shorts is now a serious contender to TikTok, gaining massive engagement.

- Google Cloud has become the third-largest cloud provider and recently turned profitable.

- Waymo (autonomous driving) and DeepMind (AI research) have enormous long-term optionality.

Alphabet’s investment in quantum computing, health tech (Verily), and AI infrastructure offers potential that’s barely reflected in its current stock price.

What the Market Is Getting Wrong

In an era where hype often drives valuation, Alphabet is being priced for caution, not innovation. But this misses the point. Alphabet has:

- Unmatched distribution across billions of users.

- One of the world’s strongest AI teams.

- The ability to fund long-term moonshot projects without risking core profitability.

The market may be infatuated with the shiny new tools, but it’s often the proven players who adapt—and win.

While antitrust scrutiny is real, current results show resilience. Unless structural changes are mandated imminently, Alphabet’s earnings engine is intact and flexing strong performance.

A Contrarian Opportunity in Plain Sight

Alphabet may not be the loudest AI story today, but it’s arguably one of the most foundational players. Its ecosystem is deeply embedded in daily digital life. The fears about its decline in Search are speculative, while the upside potential from Cloud, YouTube, and AI integration is very real—and largely unpriced.

For long-term investors, this could be a textbook case of buying quality during market distraction. Several leading analysts continue to forecast meaningful upside for Alphabet in the next 12 months. Oppenheimer recently raised its target to $220, citing rapid adoption of Google’s AI Mode in search (implying ~25% upside from current levels). Other firms such as JMP Securities and D.A. Davidson also point toward a $200+ valuation, while consensus analyst estimates from MarketBeat and StockAnalysis sit in the $200–$207 range—translating to 13–17% upside.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.