Ukranian Fear Leads To Uneasy Open

Jeremy Cook | Feb 27, 2014 04:22AM ET

Concerns over the use of the issues in Ukraine as an East/West proxy and a rather large amount of Russian sabre rattling in the past 24hrs has seen money retreat from emerging markets once again with the USD the beneficiary. Second guessing political movements at the moment in that part of the world leaves analysts on a hiding to nothing. Initial reports this morning have suggested that the parliament building in the Crimea has been overrun and the Russian flag is now being flown. Russia announced yesterday that it was ordering a comprehensive check of troop readiness in its Western and Central military districts. It conducted similar exercises and drills in 2008, before it marched its way into Georgia.

USD gained at the expense of emerging markets with Russian ruble, Ukranian hyrvnia, South African rand and Turkish lira all taking a bath on the day’s trade. Euro normally benefits from a little bit of emerging market but given the skin the EU will have in this game soon, the single currency stayed unloved.

Yesterday morning saw UK GDP unrevised at 0.7% for Q4. There was a fairly small chance that last quarter’s number was going to be revised higher – December’s 2.6% increase in retail sales could have easily done that – but yesterday we got to see how the UK is growing and not just by how much. Construction spending has been revised to a 0.2% from -0.3% previously while business investment has leapt higher by 2.4%. This last number is very encouraging as we would hope that businesses are finally peeking out from under the covers and getting involved in the UK economy once again.

Commonly, people will look to see employment as an indicator of business confidence but more often than not it is investment; employees are brought in when demand is high, investment is made when profits are goods and confidence in future expansion is strong. We are finally starting to see the latter it seems. Exports are also fighting back despite the recent strength of the pound.

The one disappointment is private consumption which missed expectations in Q4 – rising by 0.4% against a 0.6% expectation. While a miss, if growth is taken up by the business community instead of private individuals then worries over falling savings ratios and expansion of consumer credit may too fall away.

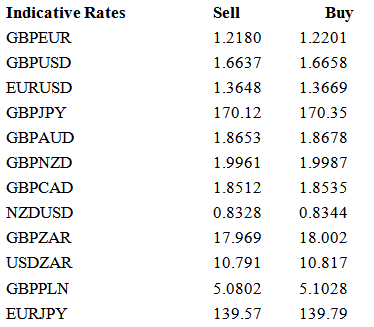

GBP was relatively unchanged on the news but allowed it a bit of backbone when the USD strength came on later in the day.

If we are starting to see business investment increase in the UK then one place we are not seeing similar is Australia. Capital expenditure by domestic businesses fell 5.2 per cent last quarter, a much wider drop than the 1.3 per cent fall the market was looking for and you’d have to go back to 2009 to find a similar decline. China’s slowdown is obviously hurting mining interests while other industries are happy to blame the strong AUD for a lack of investment. So much for a rebalancing of the economy for now. The AUD is down 0.4% against the USD, 0.6% against GBP and 0.8% versus the NZD.

NZD is on a bit of a tear this morning as Chinese demand for Kiwi milk products allowed the country to report its first 12 month trade surplus in nearly 2 years. Growth also came from inward migration and a strong rebuilding effort in response to the Christchurch earthquake. Bets are increasing that the Reserve Bank of New Zealand will raise rates at its meeting in 2 weeks; OIS swaps this morning are pricing in a 25bps hike to a 88.8% probability with the remaining 11.2% focused on 50bps hike.

While news cameras will remain focused on Ukraine and the movements of men in camouflage gear, economic matters will hone in on Eurozone M3 money supply at 09.00 this morning. Money growth has been slipping since the beginning of 2013 and will be further contributing to the deflationary pressures within the Eurozone. EZ consumer confidence is due at 10am with German CPI at 1pm.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.