Think Like A Bear, Invest Like A Bull

Lance Roberts | Mar 04, 2015 11:18AM ET

You Think Like A Bear But Invest Like A Bull?

The answer to this question is what I have come to term the “Hussman Effect.” There is relatively little argument that Dr. John Hussman is probably one of the smartest individuals in Finance. His analysis of market valuations, understanding of market dynamics and long-term secular cycles is rarely disputed. As a portfolio manager, he has managed his fund relative to his fundamental analysis that suggested over the last six-years market returns should have been low.

However, that was not the case. While his analysis was absolutely correct, the flood of liquidity by Central Banks globally drove asset prices to historic extremes. The “Hussman Effect” is where investment decisions based solely on fundamental analysis can lead to poor outcomes when other dynamics take charge.

Like Hussman, I too am a value-oriented investor and prefer to buy assets when they are fundamentally cheap based on several factors including price to sales, free cash flow yield and high return on equity. However, being a strict value investor can eventually lead to a variety of investment mistakes, which I will discuss momentarily, when markets become both highly correlated and driven by speculative excess.

Currently, there is little value available to investors in the market today as prices have been driven higher by repeated Central Bank interventions and artificially suppressed interest rates. Eventually, the markets will begin a mean reversion process of some magnitude which will suppress the value of highly inflated “value” stocks that have been driven higher by investor’s “yield chase.”

However, when that reversion process occurs is anyone’s guess.

Therefore, while the analysis suggests that portfolios should be heavily underweighted “risk,” having done so would have led to substantial underperformance and subsequent career risk.

This is why a good portion of my investment management philosophy is focused on the control of “risk” in portfolio allocation models through the lens of relative strength and momentum analysis.

The effect of momentum is arguably one of the most pervasive forces in the financial markets. Throughout history, there are episodes where markets rise, or fall, further and faster than logic would dictate. However, this is the effect of the psychological, or behavioral, forces at work as “greed” and “fear” overtake logical analysis.

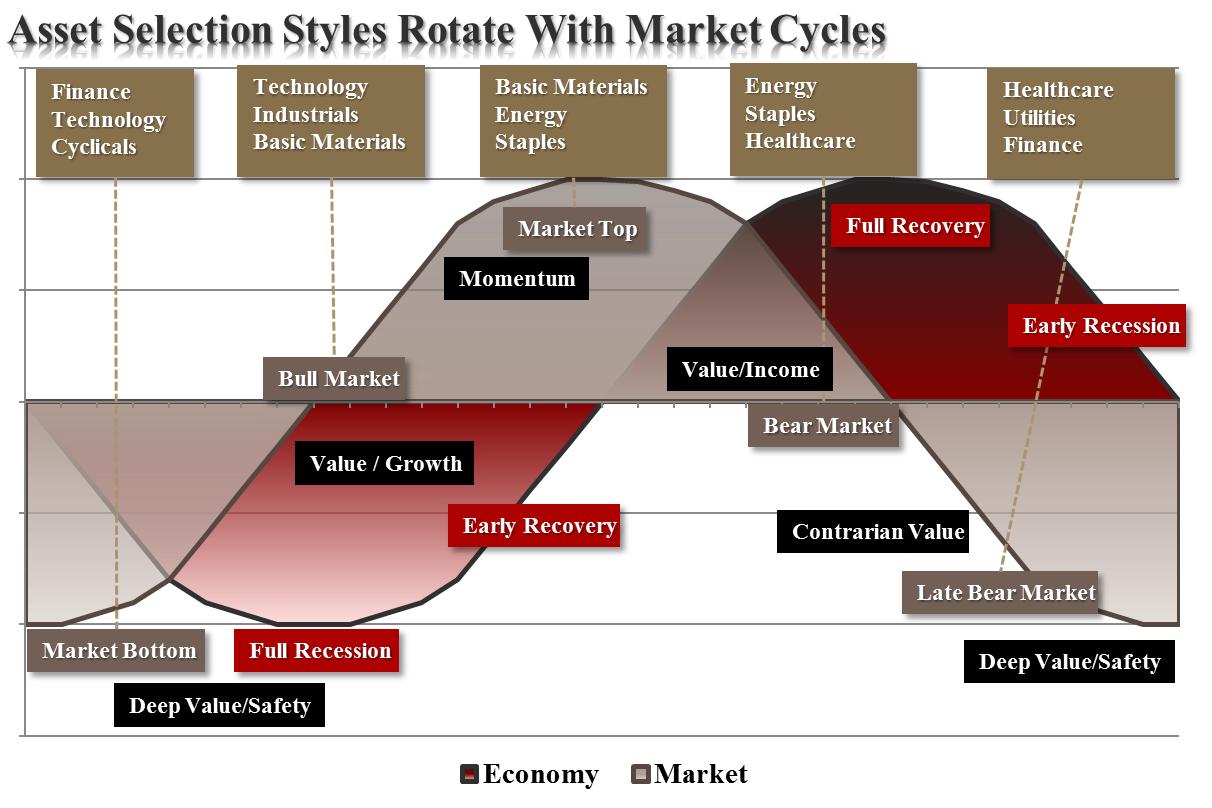

I have discussed previously the effect of “full market cycles” as shown in the chart below.

What is also important to note is that these full market cycles are ultimately driven by the economic cycle. As shown in the next chart the economic cycle leads the sector rotation cycle. However, it is also important to note that investment styles also shift during the broader cycle.

During recessionary bottoms, when assets are truly selling at “bargain basement” prices, deep discount value strategies tend to perform the best as investors are panic selling to find safety over risk. As markets begin to recover investor’s begin to cautiously re-enter the markets and begin to seek some risk with a degree of safety. Value oriented investment strategies will still work during while these early recovery cycles and growth strategies began to gain momentum. During the latter stages of the economic cycle, growth and value give way to pure momentum as investor “greed” and “exuberance” began to view “value” as “out of favor.” It is during this stage of the cycle that “fundamentals appear not matter” as the fundamentally worst stocks lead the markets higher.

This cycle does end, and the reversion process back to value has historically been a painful one.

Currently, there is little doubt that we are in both the late stages of an economic cycle and a momentum driven market. Therefore, investment focus must be adjusted to current market dynamics that requires a focus on relative strength and momentum as opposed to valuation based strategies.

There have been many studies published that have shown that relative strength momentum strategies, in which as assets’ performance relative to its peers predicts its future relative performance, work well on both an absolute or time series basis. Historically, past returns (over the previous 12 months) have been a good predictor of future results. This is the basic application of Newton’s Law Of Inertia, that states “an object in motion tends to remain in motion unless acted upon by an unbalanced force.”

In other words, when markets begin strongly trending in one direction, that direction will continue until an “unbalanced” force stops it. These momentum strategies, which are trend following strategies by nature, have been proven to work well across extreme market environments, multiple asset classes and over historical time frames.

While there is substantial evidence that market valuations and fundamentals are not supportive of asset prices at current levels, investor psychology has likewise reached extremes. In such an environment, investors need to shift focus to momentum based strategies. This is because the most common explanation for profitability of both momentum and trend-following strategies has to do with behavioral factors such as anchoring, herding and the disposition effect.

Fundamentally based investors are slow to react to new information (they anchor), which initially leads to under-reaction but eventually shifts to over-reaction during late cycle stages.

The other inherent problem of primarily data-based investors is the “herding” effect. As prices move higher, valuation arguments lose relevance. However, the need to produce investment performance in a rising market, leads to “justifications” to explain over-valued holdings. In other words, buying begets more buying.

Lastly, as the markets turn, the “disposition” effect takes hold and winners are sold to protect gains, but losers are held in the hopes of better prices later. The end effect is not a pretty one.

By applying momentum strategies to fundamentally derived investment portfolios it allows the portfolio to remain allocated during rising markets while managing the inherent risk of behavioral dynamics.

This is why, despite the fact that I write like a “bear,” the portfolio model has remained allocated like a “bull” during the markets advance. The point is simple, our job as investors is to make money when markets are rising. We can debate the valuation metrics and argue with each other why markets should not be rising, and eventually those arguments will be correct. However, for now markets are rising, and we need to participate until the trends change to the negative. Of course, if your current portfolio management philosophy doesn't have a method to understand when “trends” have changed, how will you know when it is time to step away from the poker table?

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.