The Myth Of “Buy & Hold”: Why Starting Valuations Matter

Lance Roberts | May 07, 2018 09:21AM ET

If you repeat a myth often enough, it will eventually be believed to be the truth.

“Stop worrying about the market and just buy and hold stocks.”

Think about this for a moment. If it were true, then:

- Why do major Wall Street firms have proprietary trading desks? (They aren’t buying and holding.)

- Why are there professional hedge fund managers? (They aren’t buying and holding either)

- Why is there volatility in the market? (If everyone just bought and held, prices would be stable.)

- Why does Warren Buffett say “buy fear and sell greed?” (And why is he holding $115 billion in cash?)

- Why are there financial channels like CNBC? (If everyone bought and held, there would be no viewers.)

- Most importantly, why isn’t everyone wealthy from investing?

Because “buying and holding” stocks is a “myth.”

Wall Street is a business. A very big business which generates huge profits by creating products and selling it to their consumers – you. Just how big? Here are the sales and net income for some of the largest purveyors of investment products:

- Goldman Sachs (NYSE:GS) – Sales: $45 Billion / Income: $8.66 Billion

- JPMorgan Chase & Co (NYSE:JPM) – Sales: $67 Billion / Income: $26.73 Billion

- Bank of America Corp (NYSE:BAC) – Sales: $59.47 Billion / Income: $20.71 Billion

- The Charles Schwab Corporation (NYSE:SCHW) – Sales: $9.38 Billion / Income: $2.45 Billion

- Blackrock (NYSE:BLK) – Sales: $13.25 Billion / Income: $4.02 Billion

There is nothing wrong with this, of course. It is simply “the business.”

It is just important to understand exactly which side of the transaction everyone is on. When you sell your home, there is you, the buyer and Realtor. It is clearly understood that when the transaction is completed the Realtor is going to be paid a commission for their services.

In the financial world the relationship isn’t quite as clear. Wall Street needs its customers to “sell” product to, which makes it less profitable to tell “you” to “sell” when they need you to “buy the shares they are selling for the institutional clients.”

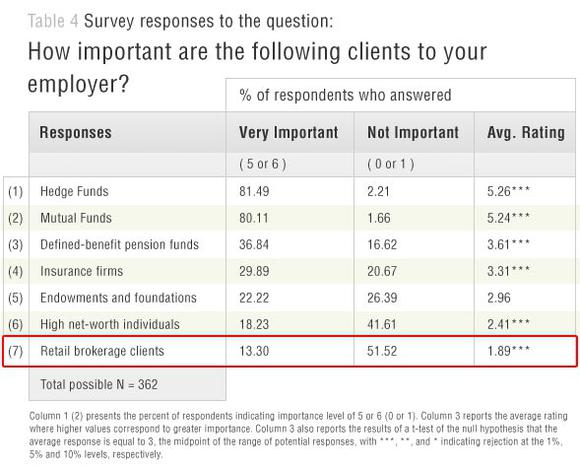

Don’t believe me? Here is a survey that was conducted on Wall Street firms previously.

“You” ranked “dead last” in importance.

Most importantly, as discussed previously, the math of “buy and hold” won’t get you to your financial goals either. (Yes, you will make money given a long enough time horizon, but you won’t reach your inflation-adjusted retirement goals.)

“But Lance, the market has historically returned 10% annually. Right?”

Correct. But again, it’s the math which is the problem.

- Historically, going back to 1900, using Robert Shiller’s historical data, the market has averaged, more or less, 10% annually on a total return basis. Of that 10%, roughly 6% came from capital appreciation and 4% from dividends.

- Average and Annual or two very different things. Investors may have AVERAGE 10% annually over the last 118 years, but there were many periods of low and negative returns along the way.

- You won’t live 118 years unless you are a vampire.

The Entire Premise Is Flawed

If you really want to save and invest for retirement you need to understand how markets really work.

Markets are highly volatile over the long-term investment period. During any time horizon the biggest detractors from the achievement of financial goals come from five factors:

- Lack of capital to invest.

- Psychological and behavioral factors. (i.e. buy high/sell low)

- Variable rates of return.

- Time horizons, and;

- Beginning valuation levels

I have addressed the first two at length in “Dalbar 2017 Investors Suck At Investing” but the important points are these:

Despite your best intentions to “buy and hold” over the long-term, the reality is that you will unlikely achieve those promised returns.

While the inability to participate in the financial markets is certainly a major issue, the biggest reason for underperformance by investors who do participate in the financial markets over time is psychology.

Behavioral biases that lead to poor investment decision-making is the single largest contributor to underperformance over time. Dalbar defined nine of the irrational investment behavior biases specifically:

- Loss Aversion – The fear of loss leads to a withdrawal of capital at the worst possible time. Also known as “panic selling.”

- Narrow Framing – Making decisions about on part of the portfolio without considering the effects on the total.

- Anchoring – The process of remaining focused on what happened previously and not adapting to a changing market.

- Mental Accounting – Separating performance of investments mentally to justify success and failure.

- Lack of Diversification – Believing a portfolio is diversified when in fact it is a highly correlated pool of assets.

- Herding– Following what everyone else is doing. Leads to “buy high/sell low.”

- Regret – Not performing a necessary action due to the regret of a previous failure.

- Media Response – The media has a bias to optimism to sell products from advertisers and attract view/readership.

- Optimism – Overly optimistic assumptions tend to lead to rather dramatic reversions when met with reality.

The biggest of these problems for individuals is the “herding effect” and “loss aversion.”

These two behaviors tend to function together compounding the issues of investor mistakes over time. As markets are rising, individuals are lead to believe that the current price trend will continue to last for an indefinite period. The longer the rising trend last, the more ingrained the belief becomes until the last of “holdouts” finally “buys in” as the financial markets evolve into a “euphoric state.”

As the markets decline, there is a slow realization that “this decline” is something more than a “buy the dip” opportunity. As losses mount, anxiety increases until individuals seek to “avert further loss” by selling.

This is the basis of the “Buy High / Sell Low” syndrome that plagues investors over the long-term.

However, without understanding what drives market returns over the long term, you can’t understand the impact the market has on psychology and investor behavior.

Over any 30-year period the beginning valuation levels, the price you pay for your investments has a spectacular impact on future returns. I have highlighted return levels at 7-12x earnings and 18-22x earnings. We will use the average of 10x and 20x earnings for our savings analysis.

As you will notice, 30-year forward returns are significantly higher on average when investing at 10x earnings as opposed to 20x earnings or where we are currently near 25x.

For the purpose of this exercise, I went back through history and pulled the 4-periods where valuations were either above 20x earnings or below 10x earnings. I then ran a $1000 investment going forward for 30-years on a total-return, inflation-adjusted, basis.

At 10x earnings, the worst performing period started in 1918 and only saw $1000 grow to a bit more than $6000. The best performing period was not the screaming bull market that started in 1980 because the last 10-years of that particular cycle caught the “dot.com” crash. It was the post-WWII bull market than ran from 1942 through 1972 that was the winner. Of course, the crash of 1974, just two years later, extracted a good bit of those returns.

Conversely, at 20x earnings, the best performing period started in 1900 which caught the rise of the market to its peak in 1929. Unfortunately, the next 4-years wiped out roughly 85% of those gains. However, outside of that one period, all of the other periods fared worse than investing at lower valuations. (Note: 1993 is still currently running as its 30-year period will end in 2023.)

The point to be made here is simple and was precisely summed up by Warren Buffett:

“Price is what you pay. Value is what you get.”

This is shown in the chart below. I have averaged each of the 4-periods above into a single total return, inflation-adjusted, index, Clearly, investing at 10x earnings yields substantially better results.

So, with this understanding let me return once again to those that continue to insist the “buy and hold” is the only way to invest. The chart below shows $3000 invested annually into the S&P 500 inflation-adjusted, total return index at 10% compounded annually and both 10x and 20x valuation starting levels. I have also shown $3000 saved annually in a mattress.

The red line is 10% compounded annually. You won’t get that, but it is there so you can compare it to the real returns received over the 30-year investment horizon starting at 10x and 20x valuation levels. The shortfall between the promised 10% annual rates of return and actual returns are shown in the two shaded areas. In other words, if you are banking on some advisors promise of 10% annual returns for retirement, you aren’t going to make it.

I want you to take note of the following.

When investing your money at valuations above 20x earnings, it takes 22-years before it has grown more than money stuffed in a mattress.

Why 22 years?

Take a look at the chart below.

Historically, it has taken roughly 22-years to resolve a period of over-valuation. Given the last major over-valuation period started in 1999, history suggests another major market downturn will mean revert valuations by 2021.

The point here is obvious, but difficult to grasp from a mainstream media that is continually enticing young Millennial investors to mistakenly invest their savings into an overvalued market. Saving your money, and waiting for a valuation based opportunity to invest those savings in the market, is the best, safest way, to invest for your financial future.

Of course, Wall Street won’t like this much because they can’t charge you a fee if you are sitting on a mountain of cash awaiting the opportunity to “buy” their next misfortune.

But isn’t that what Baron Rothschild meant when quipped:

“The time to buy is when there’s blood in the streets.”

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.