The Long View: When Will Traders Jump Off The Bullish USD Trend?

Faraday Research | Jul 12, 2018 05:25PM ET

Heading into this year, there was a convincing case for a dollar rally. After all, the world’s reserve currency had fallen sharply against most of its major rivals in 2017 as the luster of the pro-dollar “Trump Trade” wore off and the realities of governing set in. As a result, speculative futures traders had flipped to a net short position of 7,000 contracts according to the CFTC’s Commitment of Traders (COT) report at the start of this year, the most bearish positioning since mid-2014. In other words, expectations for any dollar-positive developments were extremely subdued as we flipped our calendars to 2018.

As any pole vaulter will tell you, it’s relatively easy to clear the bar when it’s set too low. In this case, dollar bulls capitalized on the lopsided positioning and continued run of solid economic data in the first half of the year, driving the US dollar index to rally 7.5% off its February lows. The greenback has rallied by even more against currencies that traders were heavily net long such as the Canadian and Australian dollars (+8% and +9% off the February lows, respectively).

Unfortunately for US dollar bulls, the strong positioning tailwind at the start of the year is starting to peter out. According to the COT report, futures traders have now shifted back to a net long position in the dollar index, to the tune of 23,000 contracts. This is the most bullish reading in over a year and closer to the middle of the middle of the three-year range. In other words, the dollar

Make No Mistake

The Fed is still likely to raise rates at least once more this year, with the potential for another two hikes by the end of the second quarter of 2019, but the outlook beyond that is murky. In fact, as of writing in mid July, the eurodollar curve has inverted, signaling that traders believe the Fed is more likely to cut its benchmark interest than raise it in 2020!

As CNBC commentators remind us daily, the market is a discounting machine, meaning that the greenback is likely to peak well before the Fed switches to a more dovish outlook – whether that’s in H2 2019 or 2020. Indeed, the market’s skepticism over continued Fed rate hikes is the primary reason for the much-ballyhooed flattening of the US yield curve.

In contrast, the Fed’s biggest rival is likely to shift to a more hawkish posture over the next year. The European Central Bank is planning on winding down its asset purchases by the end of this year, with a new rate hike cycle set to kick off in 2019, assuming everything goes to script (always a big assumption when looking out at future economic developments). Sooner or later, forward-looking FX traders may start pondering the potential for the US-Eurozone interest rate spread to start tightening after spending the last three years growing wider.

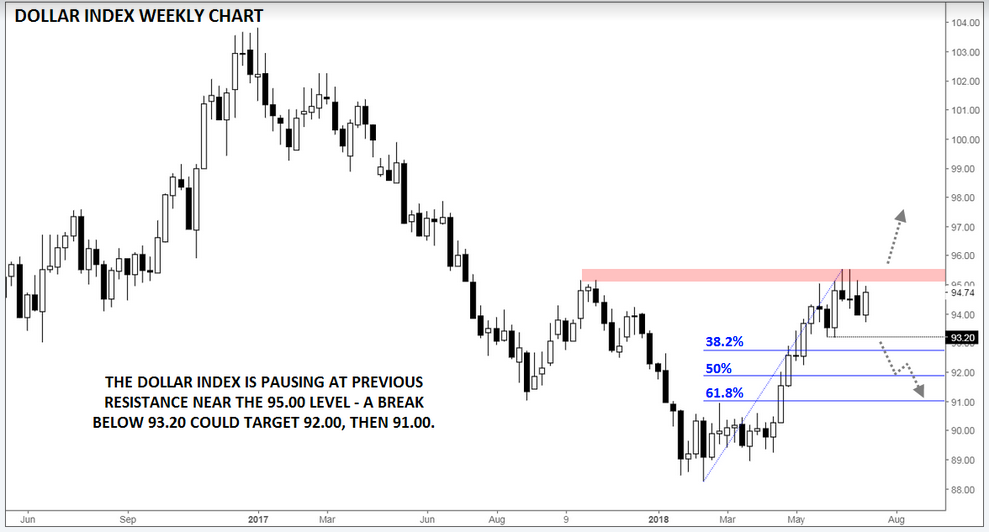

Of course in trading, being right but early on a thesis is the same thing as being wrong. Accordingly, readers may want to wait for a sign that the dollar index is resuming its long-term downtrend before growing too bearish. The first level of potential support to watch will be the 2-month low near 93.20, followed by the 61.8% Fibonacci retracement of this year’s rally near 91. Alternatively, a break above the 1-year high in the mid 95s would show that strong bullish momentum is trumping any fundamental concerns and could open the door for a continuation higher toward 98 in time.

Source: TradingView, FOREX.com

Cheers

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.