The Key Tail-Risk The FOMC Missed (But You Should Note)

Cam Hui | Feb 18, 2015 11:36PM ET

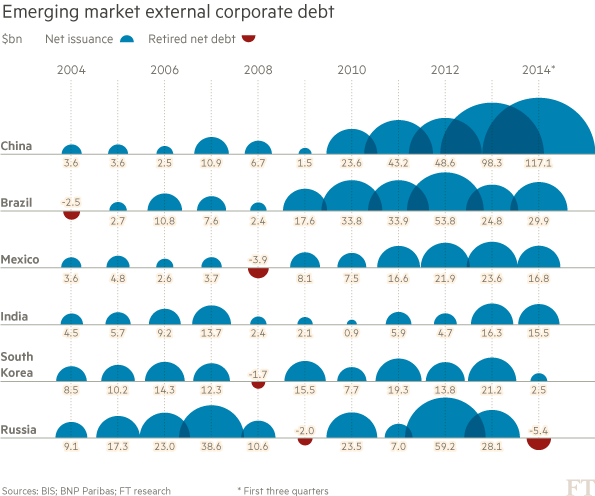

The release of the latest FT warned about the explosion in EM corporate debt, much of which was issued by corporations based in EM resource-based economies, as well as China (emphasis added):

A decade ago, the market for EM hard currency corporate bonds hardly existed. Today, it is bigger than the US high-yield corporate bond market, an asset class familiar to investors for decades, and more than four times the size of Europe’s high-yield bond market.What has driven such extraordinary growth? In just a few years before the global financial crisis of 2008-09, emerging markets won over the world’s investors. In 2001, Goldman Sachs (NYSE:GS) identified the Bric economies — Brazil, Russia, India and China — as the new engines of global growth. Chinese demand drove a commodity boom that helped billions of people rise out of poverty and into the consuming classes.

After the crisis, the developed world’s expansionary monetary policies kept the party going, pushing cheap credit to EM consumers and sending ever more foreign money into EM assets. Emerging companies, many able to tap overseas markets for the first time, embarked on a borrowing spree. Yield-hungry foreign investors were happy to help.

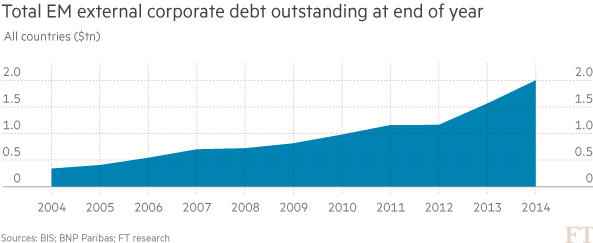

David Spegel, global head of EM sovereign and corporate bond strategy at BNP Paribas (PARIS:BNPP), has been following hard currency EM corporate bonds since 1994. His figures show that the value of such bonds in the market has grown from $107bn then to more than $2tn today.

But with Brazil’s economy imploding, China slowing and dark shadows over markets from Venezuela to Russia and Ukraine, some analysts worry that the party has gone on too long.

Stuart Oakley, global head of EM foreign exchange trading at Nomura in London, points to how easily things could go wrong. “It is entirely possible that we could see a default by a big, emerging market commodity exporting corporate,” he says.

“In that scenario you would get people redeeming money from big EM asset managers, bids for the bonds from banks would dry up, there would be sharp price drops on those and all associated assets and a sell-off across this or another asset class.”

As the chart shows, EM external corporate debt has skyrocketed over the years. What about the liquidity concerns voiced by FOMC staff over mass mutual fund redemptions, wouldn't an EM bond market rout be even worse?

With commodity prices in freefall, what happens next? Izabella Kaminska at post , Kaminska highlighted a Citi research report which postulated a collapse in USD offshore liquidity because oil exporting countries lack the petrodollars to recycle back into the USD credit markets. (And this was written in November 2014, before the collapse in oil prices, emphasis added):

One somewhat novel theory is that sharply lower crude prices might have something to do with the change in the technicals. It seems plausible to us that lower crude prices have led to a slower rate of petrodollar accumulation by oil-exporting countries and less recycling of those funds back into global financial markets—amounting to a non-negligible retraction in liquidity.There’s little doubt the petrodollar bid for fixed income securities has been tremendous during the last five years. The FX reserves of OPEC members have increased nearly 60% since 2009 to more than $1.3tn—a figure that would surpass $2tn if certain non-OPEC members, like Russia, were included. Likewise, sovereign wealth funds that are primarily funded by crude sales have increased nearly 80% over the same time period to more than $4tn (see figure). Taken together, the AUM of petrodollar investors has increased by $2.5tn in the space of 5 years, or roughly $500bn per year.

While the drop in oil prices amounts to a redistribution of wealth from oil producers to consumers, Citi believes that the net effect is not neutral when it comes to the USD credit markets:

While that’s certainly the case, what matters is how the savings from lower crude oil prices end up getting invested relative to the investments made by sovereign wealth funds and FX reserve managers. And on that score, we suspect that petrodollar investors generally make conservative investments that are inherently fixed income-friendly, while the savings from lower gasoline prices tend to grow the top line revenue of consumer-oriented companies and the margins of those companies with significant transportation costs. As such, forsaken petrodollars rarely find their way back into fixed income markets.

Vulnerable EM

The current environment leaves a number of EM economies highly vulnerable to the triple whammy of a strong USD, rising interest rates and worsening USD liquidity and falling export earnings because of lower commodity prices. The chart below shows the tight correlation the EM equities (iShares MSCI Emerging Markets ETF (ARCA:EEM)) have had with the USD and industrial metal prices. EEM is now experiencing a negative divergence with these indicators, which leaves this asset class vulnerable to more price weakness.

To be sure, not all EM economies are exposed the same way to falling commodity prices. Benn Steil and Dinah Walker at CFR analyzed the level of sensitivity of EM economies to US rate hikes, based on the Taper Tantrum episode:

They concluded:

As the bottom figure suggests, many of the same countries are likely to be in the firing line – in particular, Ukraine, Turkey, South Africa, Peru, Brazil, Indonesia, Colombia, Mexico, and India. Of these, only Ukraine has seen a significant improvement in its current account deficit, which has fallen from a whopping 9.2% to 2.5%. Poland and Romania have moderate (2%) but higher deficits, and could receive a larger jolt this time around. Only Thailand has moved into surplus, and looks likely to be spared.

In addition, I am concerned about the possible effects on China. The BIS study estimated total USD offshore loans to China, which includes government and corporate borrowers, to be $1.1 trillion - that`s not an insignificant amount.

So far, neither the EM bond markets nor equity markets have been spooked by the prospect of Fed tightness. Nevertheless, I was surprised by the tone of the FOMC minutes as the Fed does not appear to have considered this second-order effect tail-risk to the global financial system.

Disclosure: Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. ("Qwest"). This article is prepared by Mr. Hui as an outside business activity. As such, Qwest does not review or approve materials presented herein. The opinions and any recommendations expressed in this blog are those of the author and do not reflect the opinions or recommendations of Qwest.

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this article constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or Mr. Hui may hold or control long or short positions in the securities or instruments mentioned.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.