Tech Stocks May Have Topped: Time to Rotate Into Commodities, Pro-Cyclical Sectors

Chris Yates | Mar 27, 2024 02:57AM ET

- The major stock market indices in the S&P 500 and Nasdaq are pricing in a significant rebound in growth throughout 2024.

- This has been completely justified given the long leading indicators of the business cycle have been suggesting a growth rebound is coming for some time now.

- However, the areas of the market that are most forward-looking (think tech, Mag-7, etc.) are looking increasingly priced to perfection.

- In contrast, the more pro-cyclical and growth-sensitive areas of the market (materials sector, commodities, etc.) are yet to price in any material rebound in growth throughout 2024.

- As such, commodities and other pro-cyclical areas of the market could be poised to outperform mega-cap tech moving forward.

- Meanwhile, from a pricing standpoint, neither long-duration fixed interest nor credit appears particularly appealing at present.

Time for a Rotation

While we are clearly amidst a bull market in stocks, it is becoming increasingly difficult to argue the major indices in the S&P 500 and Nasdaq 100 aren’t becoming increasingly priced to perfection. This notion does not imply a rollover of these indices is imminent, but perhaps, for those looking to allocate capital to equity markets, allocating to sectors and asset classes that are not the Mag-7 or growth darlings dominating headline today may be prudent.

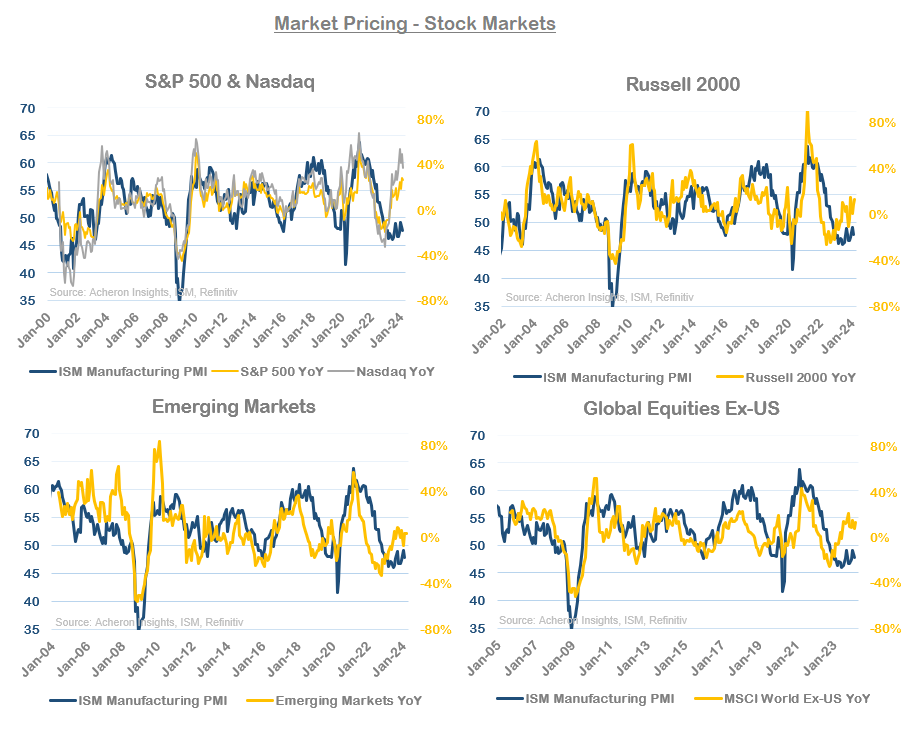

Attempting to understand what is priced into markets is a valuable exercise, particularly from a business cycle perspective. I have always found the ISM Manufacturing PMI to be an excellent (and timely) barometer for the business cycle, and comparing how various asset markets and equity indices are performing relative to the PMI provides a valuable reality check of how markets are performing relative to economic reality.

As we can see below, the S&P 500 and Nasdaq are currently pricing in a PMI of around 60, which is equal to previous cycle peaks over the past 20 years and is representative of a booming economy. On the other hand, the Russell 2000, emerging markets and global equities are all pricing a PMI of around 50-55, which is indicative of expansionary growth (but not booming economic growth), whilst also being materially lower than the more liquidity sensitive peers in the S&P and Nasdaq.

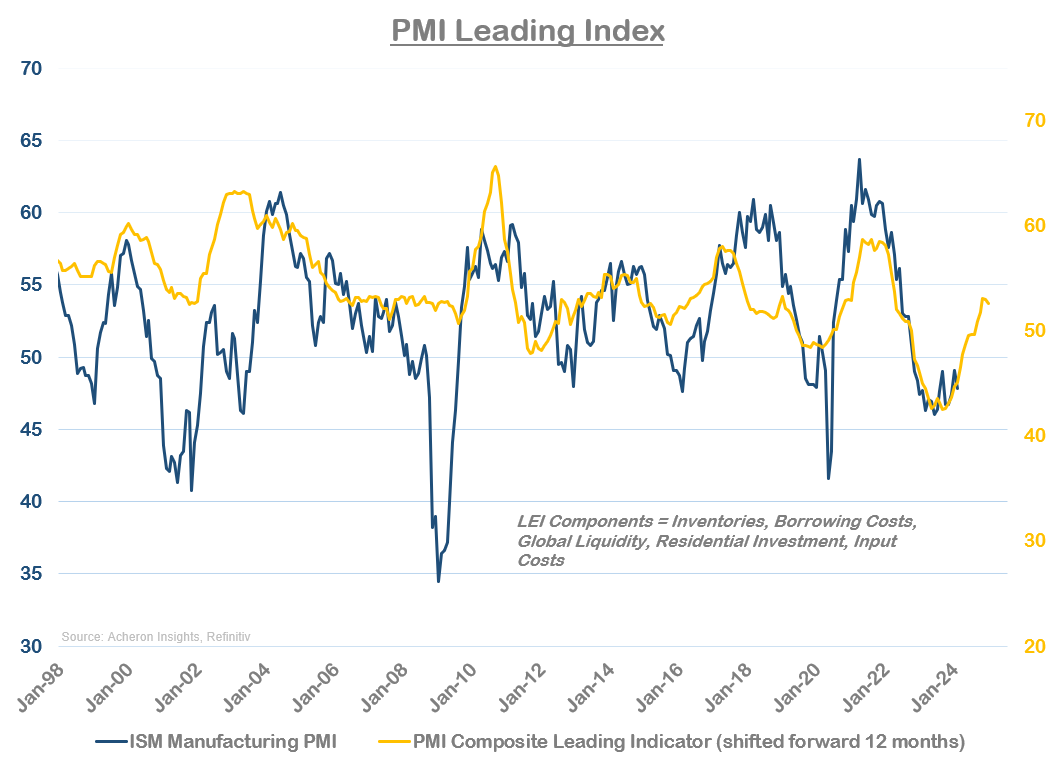

But of course, we must remember equities are forward-looking, at least to a certain degree. Thus, the S&P 500 pricing in a 55-60 PMI may well be justified should the outlook for the economy support it. As it stands, this is very much the case. My PMI Leading Index and Macro Leading Index - both of which tend to lead the PMI by around 12-15 months - suggest the PMI should rebound to 55-60 by the end of 2024. This is very much in line with what the growth areas of the market are pricing.

As such, there is no question that current growth and forward-looking growth has been largely supportive of equities. When thinking in these terms, the rally in the Mag-7 (the “growthiest” of all growth stocks) over the past year makes perfect sense.

Extending this analysis to the growth in corporate earnings, we can see my various composite leading indicators of EPS growth have both been trending higher for much of the past year. The outlook for EPS growth has thus been wholly supportive of the S&P 500 pricing in what it has done in recent times.

Nowhere is this more evident than in the liquidity-sensitive and long-duration areas of the market in technology, as well as the high-beta/low-beta ratio, all of which are pricing in a 55-60 PMI.

On the contrary, when we delve deeper into the stock market, this level of bullish forward pricing is much different for the pro-cyclical and business cycle-sensitive sectors within the market. These sectors are generally much more sensitive to current economic trends and are thus less forward looking in their ability to price in future growth.

As we can see below, although consumer discretionary stocks are pricing a PMI at a similar level to the S&P 500, the industrials and materials sectors are seemingly of value from a business cycle perspective, particularly if growth actually picks up through 2024 as the leading indicators suggest it will.

When we extend this analysis further to what is perhaps the least forward-looking asset class in commodities, we can see none of copper, crude oil, nor commodities as a whole are priced as if a 2024 rebound in growth is forthcoming. Commodities are one of the shortest-duration asset classes after all.

As such, should the leading indicators of the business cycle prove true and we do see the PMI continue to expand to the high-50s over the coming 12 months, then asset classes such as commodities (be they industrial or energy), their equity counterparts in the materials sectors or other pro-cyclical sectors in the form of industrials who are dependent on actual growth to drive earnings seem likely to outperform in this part of the cycle.

Indeed, when we look at how investors are positioning towards commodities, we can see commercial hedgers (i.e. smart money) are positioned as bullishly as they have been at any point over the past decade.

Of course, betting on sectors that require a cyclical upturn in economic growth is subject to a caveat: growth improving. And while the long-term leading indicators suggests this is forthcoming, my Short Leading Indicator of the business cycle is yet to pick-up meaningfully (though does look to have bottomed). As such, there may be further short-term risk in cyclical assets and commodities, particularly if we see a pick-up in unemployment in the coming quarter.

Time to Buy Bonds?

On the fixed interest front, I remain skeptical toward the notion we are currently being presented with any form of attractive mis-pricing when it comes to credit or long-duration bonds.

In terms of credit, junk bonds and high-yield spreads are pricing a PMI of around 55, in-line with what the leading indicators are suggesting but not as aggressive as the tech/growth sectors of the market. While I view the outlook for the corporate credit cycle to be a significant risk for markets later in 2024 and into 2025 as the refinancing cycle accelerates, credit spreads have been right to contract in recent times, particularly over the last quarter (in-line with my credit spreads model moving materially lower). Liquidity conditions have also been supportive of risk assets during this period.

Credit spreads and junk bonds will continue to trade largely in-line with equities. However, from a pricing perspective and fundamental outlook, junk bonds as a whole may not be the best risk-reward investment over the next 12 to 18 months.

On the duration front, while the case can be made bond yields should be lower given the move lower in the PMI seen over the past 18 months when this is considered in context with the stubbornness of inflation, resilient economy overall as well as the unfavorable supply and demand mismatch of treasuries, I remain bearish toward duration on a cyclical and secular level.

In fact, when we consider what my medium-to-long-term leading indicators of the business cycle are suggesting is ahead for growth, in addition to my inflation leading indicator below (which continues to signal inflation is bottoming around the 3-4% level), then from a growth and inflation standpoint, interest rates should be heading higher from here, not lower.

This is something the market is yet to price in. One-year/one-year inflation swaps are still pricing CPI of around 2.5%.

And finally, one cannot talk about market pricing without commenting on the Fed and the outlook for the Fed funds rate relative to what market participants are pricing in. Last week Powell reaffirmed the notion the Fed intends to cut rates three times in 2024, and as it stands that is exactly what the market has priced in.

While I do believe monetary policy is somewhat tight at present, I do not believe it is restrictive. Hence this dovish pivot by the Fed was a surprise to me, particularly given the recent inflation stickiness. Alas, if we do see a growth and inflation pick-up (or for the latter, continue to remain sticky around the 3-4% area), it is going to be increasingly difficult for the Fed to justify three rate cuts in 2024.

I have no doubt we will get at least one by May/June, and maybe even a second come August, but beyond that I would be surprised if the data allowed a third. A third cut would likely need to come at the expense of either the equity market or the jobs market, with a material jump in unemployment probably meaning recession. As such, a hawkish repricing at some point this year should be something investors be cautious of as we progress through 2024. If not, having an allocation in one’s portfolio to precious metals ought to serve investors well.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.