Speculation Rises, Sentiment Rebounds: Is the Cycle Getting Extended?

Callum Thomas | Jul 14, 2025 01:17AM ET

This week: late-cycle resets, speculative mood, sentiment and positioning, buy the dip, small caps, Fed rate cuts vs stocks, Space X, IPO market trends.

Learnings and conclusions from this week’s charts:

-

We appear to be going through a “late-cycle reset”.

-

Institutional sentiment is healing, risk appetite resurgent.

-

Private investors are running very high equity allocations.

-

A return to rate cuts might *not* be a good thing.

-

The IPO market is booming again.

Overall, there seems to be mounting evidence for the “late-cycle reset” hypothesis —where much like the late-90’s you see a frothy market with pressures building up getting an extension via a healthy correction (one which shakes out sentiment, but does little fundamental or enduring damage, and hence allows the cycle to continue on a little further; melting up into a potential later larger blow-off top).

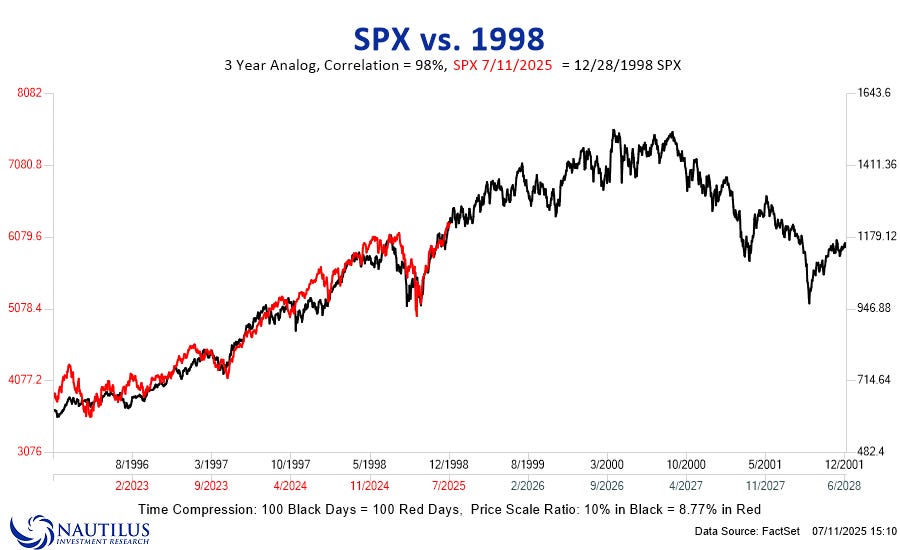

1. The Late-Cycle Reset Hypothesis: This is something I’ve examined in the last few editions of the S&P 500 Weekly ChartStorm, and here’s another angle on it — using the 1998 late-cycle reset as a direct analog.

I think there is some merit in this comparison (remember, for analog charts there ideally needs to be some rhyme/reason for using the analog, otherwise it’s just fun with chart scales), because there is the similar type of high valuations, frothy sentiment, and big scary reset going on now as then.

If we take this one literally we probably do go higher, and probably in a more ranging volatile fashion from here, and probably with some surprises yet to be known.

Source: @NautilusCap

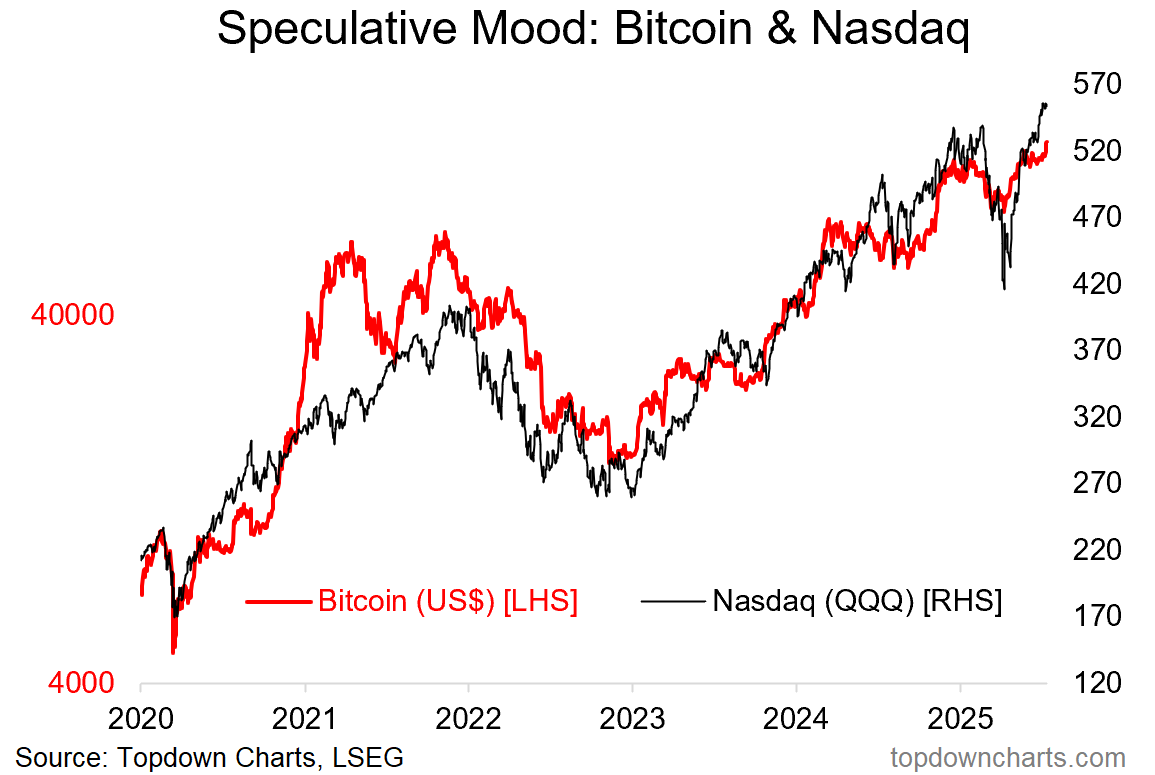

2. New Highs, Renewed Sentiment: This one also captures an element of the late-cycle reset theme because these two relatively high-speculation markets have broken out to new highs following the tariff tantrum shakeout. This tells us that speculative risk appetite is alive and well, no major damage was done during the corrections, and fear of downside is likely set to give way to FOMO with the advent of new highs and eventual chasing.

Source: Topdown Charts

3. Sentiment Reset: This dynamic is also illustrated in the investment manager surveys — after a big crash in risk appetite, folk are getting back in the pool given the absence of new bad news and a set of less bad than expected news (+desensitization) eroding the wall of worry.

Source: Investment Manager Index

4. Late-Cycle Partial-Reset: And another one for the late-cycle reset, we can see my Euphoriameter taking a material move lower (from record highs, might I add) — but refusing to rollover into a down cycle as I thought could happen. But all of this is to say that it looks like the events of H1 were a late-cycle reset, and while there are still pressures and risks building up in the system, it looks like we still squeeze a few drops of juice out of this orange yet.

Source: Topdown Charts Professional

5. Allocation Heights: Another sign of being well-progressed in the market cycle is how BofA private clients are still running very high allocations to stocks (and a very low 10.7% to cash; the lowest since 2021). This maps to multiple other datapoints revealing similar e.g. the Fed flow of funds dataset showing record high allocations to stocks by US households in aggregate.

Original Post

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.