Spear Alpha (SPRX) 1Q24 Quarterly Letter

Ivana Delevska | Jul 01, 2024 01:50AM ET

This is the 1Q24 quarterly update for our flagship fund, Spear Alpha ETF (NASDAQ:SPRX). In these quarterly letters we share our performance highlights and trends that are shaping our investment approach.

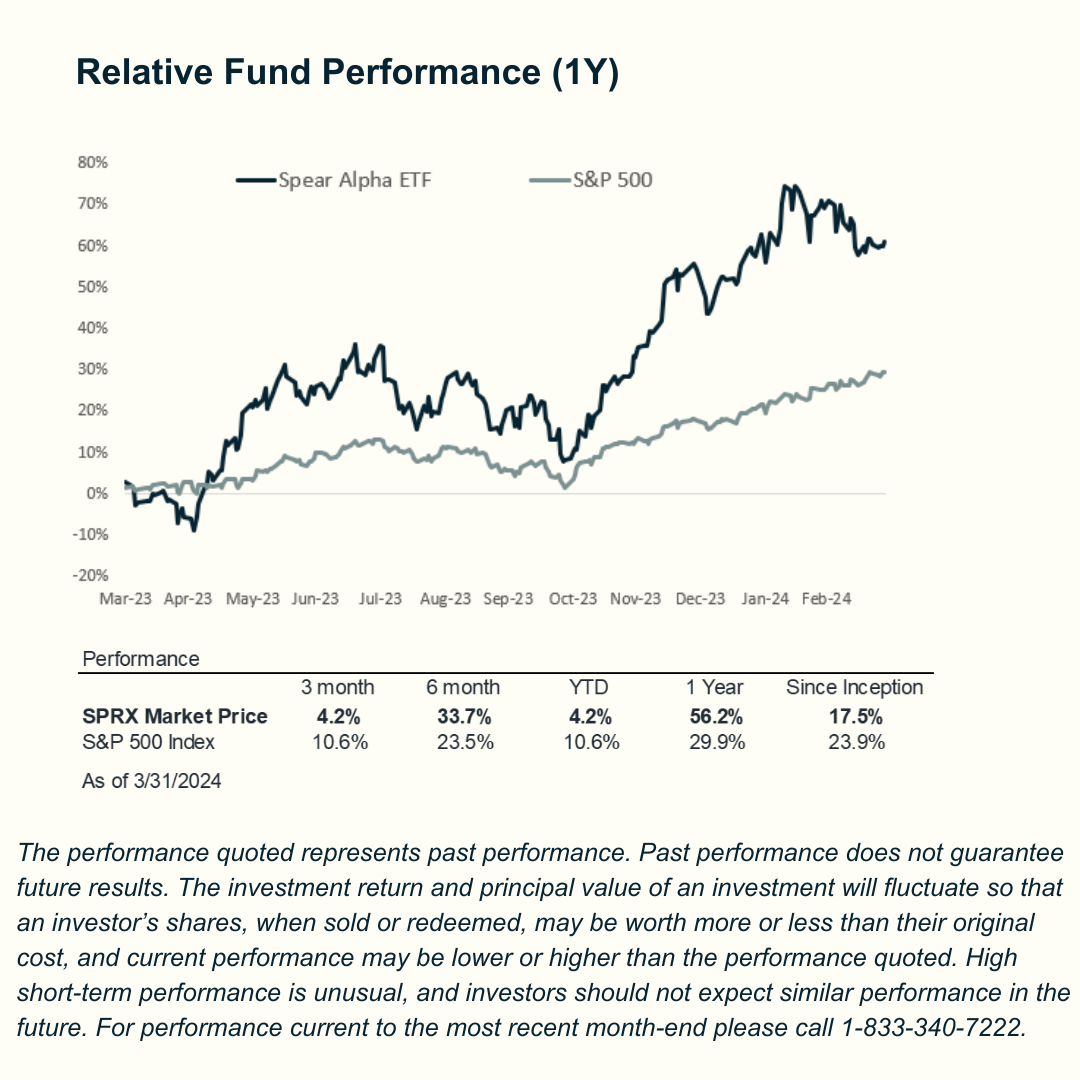

Spear Alpha ETF (NASDAQ:SPRX) was up 4.22% in 1Q24 compared to the S&P 500, up 10.56%, and the Nasdaq Composite, up 9.31%. Over the past year, SPRX was up 56.2% vs. the S&P500 29.9% and the Nasdaq Composite up 35.08%.

Summary:

As interest rates rose in 1Q24, investors shifted to playing defense, increasing their exposure to mega caps and defensive sectors like utilities. We responded to this by focusing on risk management, limiting our underperformers, and positioning ourselves to capture the next wave of opportunities. These periods of consolidation create the best entry points (both for investing in our fund and for us to find opportunities).

After a strong finish to 2023 with excitement over interest rate cuts, 2024 started on a defensive note, with interest rates trickling up and expectations for rate cuts lowered from seven rate cuts to potentially none. As a result, the market outperformance has been driven by mega-cap technology and sectors like utilities, which indicate that investors are playing defense.

The average member within the Nasdaq has had a >35% drawdown from peak this year while, the Nasdaq Index has had no more than a 7% drawdown, demonstrating how bifurcated this year's performance has been between mega-caps and the rest of the space.

During these periods of consolidation (risk-off), like in 1Q24, we shift our focus to risk management. But unlike most funds, where risk management means reducing risk, for us, it means managing risk and selectively increasing it, especially after periods like May, when we saw panic selling, particularly in software. These drawdowns allow us to add to our high-conviction ideas at attractive prices.

There is no question that we are in the early innings of the next technology cycle amplified by AI. What has been unusual about this recovery is that instead of the Federal Reserve stimulating the economy, it is providing a headwind. In the short run investor sentiment is very much tied to interest rates, which we expect to remain range-bound. As rates increase towards 5%, investors turn to risk-off, and the economy weakens (jobs, consumer sentiment, inflation down); conversely, as rate cuts take the front seat and the 10Y Treasury declines, investors turn to risk-on.

These periods of consolidation create the best entry points (both for investing in our fund and for us to find opportunities).

How Do We Manage Risk?

We have two main tools for risk management:

- 1. We increase our idea velocity: during periods of consolidation, we increase the pace of generating new ideas (e.g., in the past 3-4 months, we have increased our exposure further down the data center value chain, specifically expanding to areas "outside of the rack" including materials, components, and electricity generation).

- 2. We take profits on outperformers and cut/reduce losers. The most important aspect of this is that we try to maintain the same level of risk so that when the market turns to risk-on, we are positioned to capture the benefit.

Fundamental active strategies, in general, perform better in a risk-on environment as investors are looking to allocate to ideas that capture alpha and broaden their exposure beyond just tracking broader market.

What Gives Us Confidence for the Rest of the Year:

- Capex spending cycle just kicked in. Coming out of the 1Q24 earnings season, a constant theme was increased capex. Expectations for hyperscaler capex growth are now +40% yoy vs. ~20% as we entered the year with the five largest hyperscalers investing >$200B. Estimates for '25 are >$250B which could prove to be conservative as Nvidia (NASDAQ:NVDA)'s Blackwell (B100) chip is entering production and offers significantly lower TCO (total cost of ownership).

-

Data Center investment cycle is broadening-out. AI spending last year was mostly focused on processors/GPUs and Nvidia was the only company that got a meaningful boost from AI. This year we are starting to note the impact of the AI spending wave both inside the rack (processors, networking, memory) and outside of the rack (electrical and thermal management, power generation etc.).

- Attractive valuations. Valuations for mega-cap technology have expanded over the past 6 months but are still within historical ranges. Valuations for mid-caps (

Performance contributors and commentary

The most significant change to our portfolio in '24 vs. '23 was that we expanded our Data Center hardware investments beyond processors (GPUs) and created a new focus area, "Materials & Power Generation," which we expect will benefit from a broader data center build-out.

The types of companies included in this area are 1) materials such as copper, 2) components such as electrical equipment, connectors, and thermal management, and 3) power generation, including independent power generators. As many of these companies are cyclical, the turnover of this basket is higher than some of our other focus areas, where we often maintain our holdings through the cycle (in varying sizes).

For 1Q24 our out-performers were:

- Data Center Hardware. Nvidia (NVDA) stood out and was our best-performing idea in the quarter and ytd. AMD (NASDAQ:AMD) and Marvell (NASDAQ:MRVL) also outperformed the rest of our portfolio but underperformed our expectations. The underperformance is because while AI is a positive contributor for these companies, it is not material enough to offset weakness in the rest of their businesses. We are being patient with these companies as we expect that it may take 1+ years to scale their new products.

- Materials and Power Generation. Freeport McMoran (NYSE:FCX) and Teck Resources (NYSE:TECK) outperformed the rest of our portfolio. Since the end of the quarter, we took some profit in copper and redeployed it to other areas in power generation and connectors.

Our underperformers were Cybersecurity and Data Infrastructure companies, which was the reverse of 4Q23. While it may not be obvious from looking at the broad indices, the software sector got destroyed in 1Q24 and continued to face significant pressure, specifically in May. What started as a pull-back turned into carnage, with many companies down 40%+ since the end of 23.

- Cybersecurity. Despite ransomware hitting all-time highs and now affecting over 10% of organizations, cybersecurity got caught up in the software sell-off. For cybersecurity specifically, interest rates were the main negative driver, while fundamentals have remained strong. Crowdstrike (CRWD) was the relative outperformer in the quarter vs. Zscaler (NASDAQ:ZS) (S) and Sentinel One (S), which meaningfully underperformed.

-

Data Infrastructure. In addition to interest rates, data infrastructure software did not deliver the expected fundamental improvement in 1Q23. There are two main reasons behind this that we have identified:

1. The initial investment wave in AI has been securing hardware and "renting" this hardware as a service. Revenue from selling software services and applications is still in the early days. This is why companies like Datadog (NASDAQ:DDOG), while still growing, are tracking below the historical 2x the rate of AWS growth (Amazon (NASDAQ:AMZN)).

2. Companies cut spending during the downturn and were more focused on reaching profitability at the expense of growth, which is now coming back to bite them. A common theme that we are noting is that companies that were supposed to be growing 30-40% are now growing only 20%. Snowflake (NYSE:SNOW) is a prime example. Some of this is a function of weak macro/enterprise spending, but some of it may be related to dropping the ball. We have largely maintained our exposures but are looking to selectively add to the ones that are able to play offense rather than defense.

While we are not concerned about the first point as we are confident that as companies start building on top of the hardware, they will need the software services (especially critical ones like cybersecurity, observability, and data streaming), we are laser-focused on the second to make sure we don't get stuck with the losers.

We are maintaining our balanced positioning between software and hardware, but we have started adding to software on a selective basis, expecting to benefit if interest rates stabilize.

We continue to manage risk actively and asses the potential risk/reward of each individual holding, incorporating the trajectory of earnings and valuation. We aspire to perform in line with diversified indices on the downside, and generate differentiated performance on the upside, given our concentrated portfolio of investments.

DISCLOSURES:

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance current to the most recent month-end please call 1-833-340-7222. The total expense ratio is 0.75%.

For a prospectus or summary prospectus with this and other information about the Fund, please call (888) 123-4589 or visit our website at www.spear-funds.com. Read the prospectus or summary prospectus carefully before investing.

- “Alpha” strategy seeks to identify investment opportunities in which the performance of a company’s stock will exceed that of the market over time.

- B2B stands for business-to-business.

- Free Cash Flow (FCF) is the cash a company generates after taking into considerations the cash outflows that support its operations and its capital expenditures.

- CAPEX stands for capital expenditures or funds used by a company to acquire, upgrade, and maintain physical assets.

- EV/EBITDA is a commonly used valuation metric and is the ratio between the value of the enterprise to earnings that the company generates. EBITDA stands for earnings before interest, tax, depreciation and amortization.

- S&P 500 is a stock index that tracks the share prices of the 500 largest companies in the United States by market capitalization.

- Nasdaq Composite is a market capitalization-weighted index of more than 2,500 stocks that are listed on the Nasdaq stock exchange.

Investing involves risk, including possible loss of principal. The fund is subject to both growth and value equity risk. Investing in growth companies that are based on an issuer’s future earnings may be more volatile if revenues fall short of expectations. Investing in value companies that remain unfavored or are undervalued for long periods of time could have a negative on the fund’s performance. Companies in the industrials sector may be adversely affected by changes in government regulation, world events, economic conditions, environmental damages, product liability claims and exchange rates.

Technology, Space, Robotics and Automation companies are particularly vulnerable to rapid changes in product cycles, obsolescence, government regulation and competition, both domestically and internationally, which may have an adverse effect on growth and profit margins. Market or economic factors impacting these companies that rely heavily on technological advances could have a major effect on the value of the Fund’s investments. SPRX is non-diversified and may invest in a greater percentage of its assets in securities of an issuer in the industrial or technology sectors. An adverse event to an issuer in the industry may negatively impact the fund’s performance.

Applying ESG (Environmental, Social, Governance) sustainability criteria to the investment process may exclude securities of certain issuers for non-investment reasons, and therefore, the Fund may forgo available market opportunities.

Foreside Fund Services, LLC, distributor.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.