Softer Dollar Seen Amid Potential Strong Euro Data

Fullerton Markets | May 15, 2017 04:43AM ET

Softer U.S. data may prompt USD/JPY to drop below 113, good time to short?

U.S. dollar downside risks seen increasing after soft inflation

Dollar index fell below its 200-day moving average during Friday’s overnight session and U.S. 10-Year Treasury yields edged lower after slower U.S. inflation and disappointing retail sales growth weighted on pace of Fed’s rate hikes expectations this year. Together with softer China PPI data released last week, we think the global inflation growth faces the risk of slowing down.

Inflation in world largest economy slowed in April at an annual pace of 1.9%. This is the lowest rate in almost two years and below the key 2% threshold. Meanwhile, the retail sales rose by just 0.2% MoM in April, below consensus 0.4%. Though the Fed is widely expected to raise interest rates at it’s meeting next month, the pace of rates normalisation in second half is expected to slow down if the trend confirmed slower inflation growth.

Market has widely forecasted two more hikes this year after 25bp increase two months ago, any slower pace of hiking is set to undermine the strength of U.S. dollar. The chart below shows that Fed fund rates have been consistent with the trend of U.S. inflation rate over a long period of time.

China ‘Belt & Road’ initiatives help to boost sentiment on yuan and rest of EM currencies, not a postive news on U.S. dollar

Chinese President Xi Jinping pledged $124 billion over the weekend for his new Silk Road plan to forge a path of peace, inclusiveness and free trade, and called for the abandonment of old models based on rivalry and diplomatic power games. The strategy of belt and road plan comes with the plan on further yuan internationalisation, as a major funding boost denominated in yuan currency to the new Silk Road is pledged.

The funding includes an extra 100 billion yuan into the existing Silk Road Fund, 380 billion yuan in loans from two policy banks and 60 billion yuan in aid to developing countries and international bodies in countries along the new trade routes. Such environment requires yuan to be more internationised than its current status. If China needs to pursue that, the nation is likely to anchor on currency stability, otherwise capital outflows will increase along with a more liberal capital market. USD/CNY has been moving below 6.9 again these days, which could be an effort of Chinese authorities to stabilise its currency. A stable yuan will also influence other currencies in the region, such as TWD, MYR, KRW etc., appreciation in these currencies may also contribute to the weakness of the U.S. dollar.

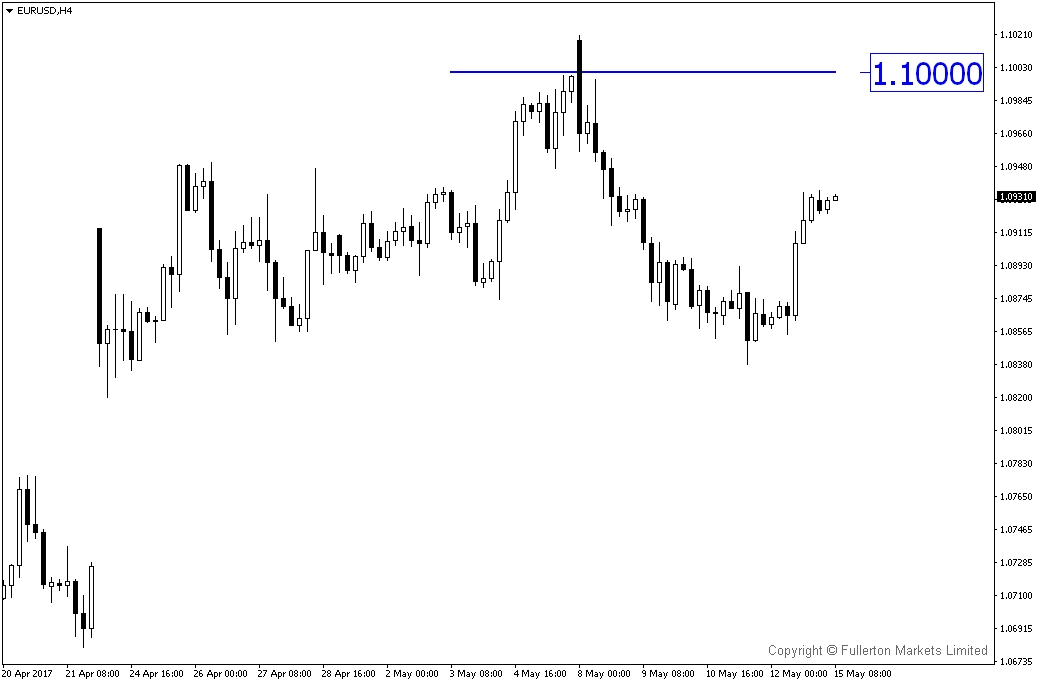

Euro Zone economic data could further support the single currency

EUR/USD can sustain a move above 1.1000 this week supported by encouraging Eurozone economic activities. Rising PMIs in both manufacturing and service sectors call for the GDP growth in first quarter to be in a good shape. The ZEW economic sentiment survey released on Tuesday is likely to improve due to lower political risk. The implication is ECB may start to reduce monetary policy accommodation sooner rather than later which bodes well for EUR. Interestingly, Der Spiegel reported on Friday that ECB will likely signal a shift away from its super-accommodative monetary policy stance as early as July.

Our Picks

EUR/USD – Slightly bullish. We expect this pair to move towards 1.10 in coming days if the economic data beats earlier forecast.

USD/JPY – Slightly bearish. We expect the soft sentiment on dollar may drag this pair towards 113.

Top News This Week (GMT+8 time zone)

Euro Zone: GDP. Tuesday, 16 May, 5pm.

We expect figures to come in at 0.6% (previous figure was 0.5%).

UK: CPI. Tuesday, 16 May, 4.30pm.

We expect figures to come in at 2.5% (previous figure was 2.3%).

Japan: GDP. Thursday, 18 May, 7.50am.

We expect figures to come in at 0.3% (previous figure was 0.3%).

Fullerton Markets Research Team

Your Committed Trading Partner

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.