Retailing Is Bad And About To Get Worse

David I. Kranzler | Mar 01, 2017 12:55AM ET

Americans are filing for bankruptcy at the fastest rate in several years. In January 2017, 55,421 individuals filed bankruptcy. That’s a 5.4% increase over January 2016. In December 2016, 4.5% more individual bankruptcies were filed than in December 2015. It’s the first time in 7 years that personal bankruptcies have risen in successive months on a year over year basis.

Also notable, in 2016 the number of U.S. corporate bankruptcies jumped by 26% over 2015. U.S. corporations have issued $9.5 trillion in bonds. That’s 61% more than they borrowed in the eight years leading up to the 2008 de facto financial system collapse (aka “the great financial crisis”).

The Financial Times reported that over 1 million U.S. consumers – prime and subprime – were behind on their car loans and that the overall delinquency rate had reached its highest level since 2009. The FT also stated that:

lending to consumers with weak credit scores has been one of the fastest growing parts of the [banking] industry.

It’s starting to smell like early 2008 out there.

This is information and data that you will not hear on any of the “Bubblevision” financial “news” programs or read in the mainstream financial media. It’s also information that is not being factored at all by stock prices.

Americans are bulging from the eyeballs with mortgage, auto, credit card and student loan debt. The amount of outstanding auto debt hits a new record every month. Of the $1.2 trillion in auto loans outstanding, over 30% is considered subprime. In fact, I would bet good money that the number is closer to 40%, as the same type of non-documentation loans that infected the mortgage market in mid-2000’s has invaded the auto loan market. It was recently disclosed that the 61+ day delinquency rate on General Motors' (NYSE:GM) securitized subprime loans has soared to levels not seen since 2009.

To put the amount of subprime auto debt in context, assume 35% of total auto debt outstanding is now below prime (subprime and “not rated”). This equates to $420 billion of below prime debt. The total amount of below prime mortgage debt during the mid-2000’s housing bubble was about $600 billion. In other words, the subprime auto debt problem could easily precipitate another financial markets catastrophe.

Although the retail sales report for January earlier this month purported to show a 4.9% year/year increase in retail for January, the majority of the “gain” came from the rising price of gasoline during the month (the gasoline sales category showed a 13.9% gain over January 2016, most of which can be explained by higher prices).

In fact, the .4% “gain” from December 2016 to January 2017 reported for the overall retail sales number lagged the Government’s measure of inflation. Real, inflation-adjusted sales from December to January declined by 0.20%. (Note also that the retail sales report is derived largely from Census Bureau “guesstimates” due to the supposed unavailability of real-time data. This explains why typically previous reports are revised lower – I detail this in my weekly Short Seller’s Journal ).

Debt-squeezed Americans are spending less on discretionary items, especially clothing. This is why Walmart (NYSE:WMT) has launched a new price-war agenda aimed at the grocery industry, big-box retailers and Amazon.com (NASDAQ:AMZN). The retail spending “pie” is shrinking and Walmart intends to do fight hard to maintain the size of its piece. For all the attention focused on Amazon, Walmart’s annual revenues are nearly 4-times larger than Amazon’s. And make no mistake, Walmart has plenty of room to fight, as its operating margin is nearly double AMZN’s – and that’s before we adjust AMZN’s highly misleading accounting, which would reduce AMZN’s margins.

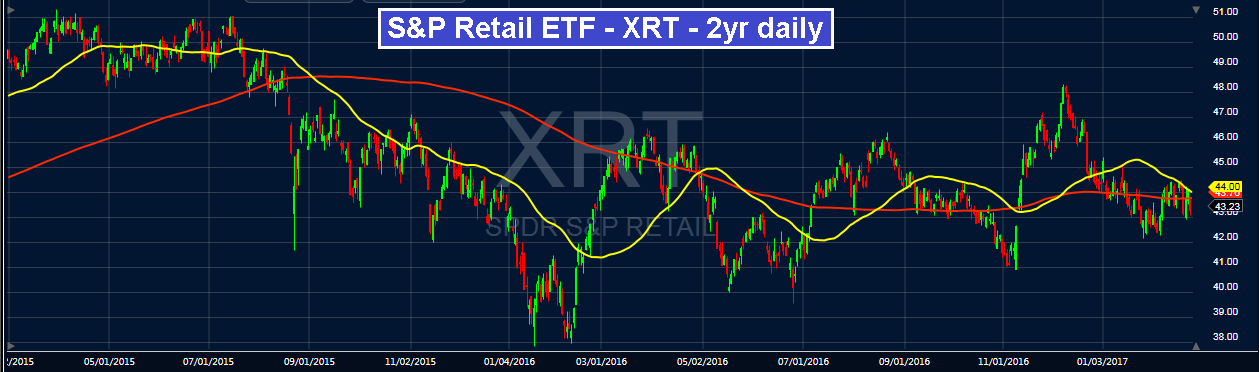

Despite the Dow hitting new all-time highs for a record number of days in a row, The S&P retail ETF, XRT (NYSE:XRT), is currently 10.4% below its 52-week high. It’s 15% below its all-time high, which it hit in mid-July 2015:

Target (NYSE:TGT) is today’s poster-child for the retail sector, as its Q4 earnings missed expectations badly and it warned for 2017. Its quarterly revenues dropped 4.3% year over year and its full-year 2016 earnings fell nearly 6% vs. 2015. Operating earnings were crushed, down 42.2% in Q4 2016 vs. Q4 2015. The stock is down over 11% right now (mid-morning trading on Tuesday).

I would also suggest that the revised GDP for Q4, reported to be 1.9%, is derived from government statisticians’ manipulation because most of the gain is attributed to consumer spending. Tell that to holders of XRT and RTH (NYSE:RTH).

The economy is sinking further into a recession despite the propaganda coming from Wall Street, financial bubblevision “meat with mouths” and the mainstream media. Real median household income continues to decline and the Fed/government intervention in the stock market is helpless to prevent this fact from being reflected in many sub-sectors of the stock market “hiding” beneath the headline-grabbing Dow and S&P 500.

![]()

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.