Rates Spark: The ECB Pushes Back

ING Economic and Financial Analysis | Jan 16, 2024 04:25AM ET

By Benjamin Schroeder

EUR curves bear flattened at the start of the week with the European Central Bank leaning against aggressive market pricing. The message remains consistent – much of the wage data will only be available by the June meeting. At the same time, the ECB knowingly limits the reach of any pushback by sticking to overall data dependency

The ECB Counters Aggressive Cut Expectations With Consistency

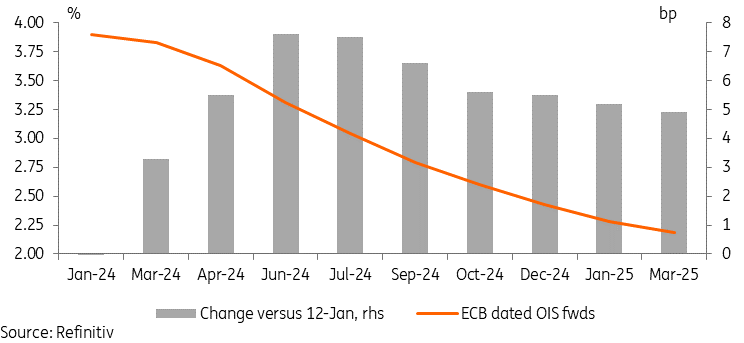

The market’s pricing of ECB rate cuts going into this week was elevated, prompting expectations that we would start to see more pushback from officials. And observers were not disappointed.

Chief Economist Philip Lane initiated the renewed pushback already over the weekend when he cautioned against recalibrating policy too early. And specifically with regards to the development of wages, he pointed out that the Council would only have the most complete data set available by the end of April, so only in time for the June policy meeting.

Yesterday then saw two of the most hawkish ECB members Robert Holzmann and Joachim Nagel add their takes. Holzmann highlighted that early wage data pointed to relatively high increases. The Austrian central banker also warned that one should not bank on rate cuts this year given the potential price implication of supply chain and energy disruptions from developments in the Middle East. The Bundesbank’s head concurred that it is much too early to talk about rate cuts with wages being the “great unknown”.

Market rates nudged higher on the back of yesterday’s remarks, even defying a negative GDP figure out of Germany. But they are still more than fully pricing in a first ECB rate cut by April and overall remain close to discounting 150bp in policy easing over 2024.

The ECB probably knows that it is difficult to really move markets away from pricing that is seemingly inconsistent with its communication. But market pricing has to include pricing for tail risks, not just the baseline scenario. Even Lane highlighted downside risks to the outlook and possibly even disinflationary effects of geopolitical tensions – wages are not everything.

To a degree, there is some justification to the market dynamic of anticipating a turning cycle. After all, the remarks by Lane and (most) others including Nagel yesterday seem to indicate that there is a consensus building within the Council that summer could be a possible turning point. And once the ECB starts to move, Lane made clear to not expect this to be a one-off but signaled a sequence of cuts.

Despite ECB Pushback, Summer Still Can't Come Soon Enough for Markets

Today’s Events and Market Views

While US markets will return from a long weekend, the focus today should initially remain on EUR rates and central bank communication. The ECB’s François Villeroy, one of the more influential centrists, is scheduled to speak today in a panel at the Davos World Economic Forum.

In eurozone data, we will get the German ZEW survey and the ECB’s consumer survey on inflation expectations. The fragility of expectations is a particular worry to officials, which is likely only exacerbated by geopolitical tensions. The US calendar is light, with only the Empire Index of note, but we will have the Fed’s Christopher Waller speaking on the economy and policy.

Today’s highlight in primary markets is the launch of a new 25Y green bond by France via syndication. Germany will auction a new 5Y bond.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.