Rates Spark: System Stresses Are Key

ING Economic and Financial Analysis | Mar 14, 2023 08:49AM ET

SVB reverberations continue. In the US, the FRA/OIS spread is at a tipping point and needs to calm to help generate wider calm. US financial conditions have tightened considerably as a consequence of all of this. This does a job for the Fed, but the Fed would no doubt prefer the system to look and feel safer. US CPI is less relevant - the system is key for now

The FRA/OIS Spread Is at a Point of Vulnerability; Spelling Trouble if it Does not Calm

The US 3mth FRA/OIS spread spiked out to 60bp yesterday, it's widest since the pandemic. But it is nowhere near as wide as it got to during the Great Financial Crisis a decade and a half ago, and so far there is no major panic here. The FRA/OIS spread has been in the 40-50bp area on many occasions over the past decade in fact. Still it's a market deviation versus the very tight FRA/OIS spread seen in recent seeks. We remarked at the time that such a tight spread meant that the Fed could indeed deliver a 50bp hike at the March meeting, as the system was taking it quite calmly. That's clearly changed in the wake of the Silicon Valley Bank collapse.

Now the FRA/OIS spread is in territory where the system is under some stress, or at least under perceived stress

Now the FRA/OIS spread is in territory where the system is under some stress, or at least under perceived stress. It remains to be seen whether there is a material wider contagion in the small and regional banking sector in the US. Certainly there was a strongly correlated tumble in the performance of stocks in that sector yesterday, including some outsized moves in certain names. So far there has not been another actual collapse, nor material evidence there's one coming. But its early days. Re-scrutiny of quarterly results is ongoing now, especially given the clear hindsight evidence from the SVB results that there were potential issues there.

Meanwhile, the Federal Home Loan Bank System is set to raise over US$80bn in short-term debt, typically employed as a means to help shore up deposit shortfalls for US banks. The fear is that the genesis of this is deposit outflow pressure on the part of some banks; the smaller ones in particular. Over the weekend, the Fed, Treasury and regulators managed to stem this risk by protecting depositors, at least in SVB and Signature Bank, and there is an implication that all deposits are in fact safe, especially given the blanket comments made by President Biden.

Part of the market panic is counterintuitive

Part of the market panic is counterintuitive, and likely reflects an implied concern coming from the very swift and significant action coming from the Treasury and Fed. The thinking here is they must have been worried enough to warrant action taken. If we go through the rest of this week and there is nothing else to see, then this whole thing will likely calm down. Watch the FRA/OIS spread as an ongoing gauge of system risk. Alternatively, should the FRA/OIS spread remain elevated it suggests that the system remains fragile and vulnerable, even if still functional.

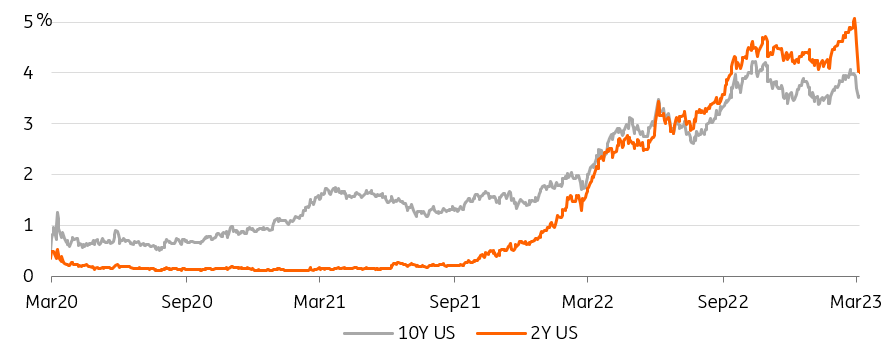

The Collapse in 2Y Treasury Yields Highlights the Dramatic Shift in Fed Hike Expectations

Source: Refinitiv, ING

Financial Conditions Have Tightened Considerably; Less Immediate Pressure to Hike

Importantly, the biggest impact so far has been a material tightening in financial conditions. Even though market rates have fallen significantly, which loosens financial conditions, the widening in credit spreads and the likes of the FRA/OIS spread has the opposite effect, and that has dominated. US financial conditions are now as tight as they have been during the rate hiking cycle so far. In a way this is far more impactful than the delivery of a large interest rate hike.

No need for a hike right now if the weak system is showing vulnerability

The market has undiscounted hikes in the coming months. A 25bp hike in March is discounted with a 60% probability, but in reality not fully discounted till the May meeting. From there, the market is discounting cuts, starting with at least a 25bp cut from the July meeting. The US 2yr yield is back below 4% in tandem. Remarkably this had broken above 5% only a week ago. It's now at it's lowest since September last year, yet the fed funds rate is higher by 150bp since then. Less dramatic is the 10yr, which is back in the 3.5% area we were at only a month ago.

The silver lining is that the dramatic dis-inversion of the 2/10yr curve (now -40bp, was over -100bp) can imply less future pain for the economy. The logic here is that fewer hikes can mean less pain, and earlier cuts help cushion the economy.

This may be the case, but we need to get through the system stresses first.

Away From the Banking Sector, Signs of Contagion Have So Far Been Limited

Source: Refinitiv, ING

EUR Rates See a Sharp (OTC:SHCAY) Repricing of ECB Policy Outlook…

The risk-off move in the US paired with an extraordinary shift in policy expectations has also gripped European markets. This comes just a few days ahead the European Central Bank meeting where the bank plans to brandish its inflation-fighting credentials. The ECB had managed to firmly anchor expectations for a 50bp hike this week, and just last Thursday markets were seeing a good chance that the ECB could take the deposit rate from 2.5% currently to above 4% this year.

Now, markets are on the edge between 25bp or 50bp this Thursday, seeing the overall tightening to be delivered this year at just below 90bp – the ECB might just reach 3.5% after summer. The magnitude of the interest rate moves are mind-boggling, with 2Y Bund yields dropping 40bp and the 10Y still 25bp just yesterday. In outright terms, we are back to where we were just a few days after the last ECB meeting at the start of February.

... Although Stress Indicators Themselves Look More Contained

The question the ECB will ask itself is how bad is it? The ECB of course will always have an eye on sovereign spreads. The key spread of 10Y Italian government bonds over Bunds widened by 11bp to just over 191bp – we have seen wider spreads in February.

One will be more inclined to look at market measures related to systemic stress in the banking system and short-term funding markets. The European stress measures are still well below peaks seen in the latter half of 2022. The Itraxx senior financials CDS spread is 26bp wider from last Thursday. At 112bp, it is the widest since November, but still below the c.150bp peak of last September. In money markets the forward 3m Euribor/OIS for June widened to 18bp yesterday, up from just below zero at the start of last week. But it is also just 5bp over the average where the market saw the spread one quarter out over the course of 2022.

News stories citing ECB sources suggest that it will stick to its plan with regards to the 50bp hike

News stories citing ECB sources over the course of yesterday suggest that the ECB will stick to its plan with regards to the 50bp hike this week. But the outlook beyond March has become increasingly uncertain, considering financial stability fears. Our economists have stuck to the view that the ECB will only get to 3.50% in the depo rate, citing the lagged impact of monetary policy. A tightening of financial conditions via systemic stress might just be that, but it also still implies more tightening and likely higher market rates again.

***

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.

Original Post

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.