Rates Spark: Rates Pressure Intensifies

ING Economic and Financial Analysis | Dec 15, 2022 06:32AM ET

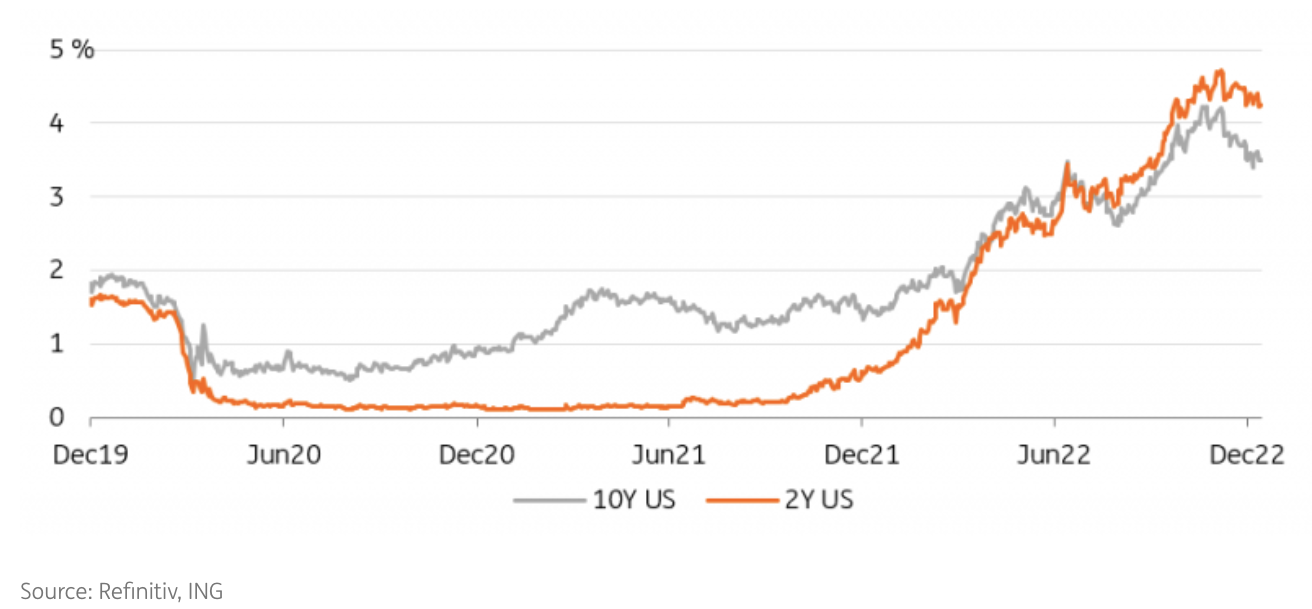

Markets need to re-think the sustainability of the bond rally seen in the past month. Nominal and real rates are seen up. But not by very much. With no sense as of yet that the Fed is done, we continue to call for market rates to move higher from here. We likely have seen the highs at 4.25%, although our models in fact call for a peak with a 5% handle, and the anomaly here is how big the discount is between the 10yr yield and the likely peak in the funds rate.

The 50bp fall in the US 2yr yield between this FOMC and the previous one correlated with a steady ratchet lower in the market discount for the terminal Fed funds rate. At the peak, the market was discounting 5-5.25%. It’s now discounting 4.5-4.75% as a terminal range.

This also ratchets lower the upward pressure on the 10yr yield, which tends to be influenced by where the funds rate peaks. It still leaves us with a conundrum where the current 10yr yield looks quite low relative to a terminal funds rate set to be a bit hit in mid-to-late-Q1 of 2023. If the 10yr stays here, the discount would be in excess of 100bp, which is quite large relative to the past few decades. We think the 10yr can narrow that discount in the coming month or so.

2Y and 10Y Treasuries yields have peaked well below the Fed's signaled terminal rate of 5%.

No Change in Balance Sheet Policy

Chair Powell had little to say of any materiality on the bond buying unwind. There had been a small probability attached to the possibility that the Fed could have considered outright bond selling (as opposed to the less impactful ongoing bond roll-off). The rationale could have been to mute, or even reverse, the significant fall in long end yields seen in the past month; done with a view to re-tightening financial conditions.

In the event, the committee is not looking into this just yet. It remains an option, however, especially should the Fed require an overall tightening in liquidity circumstances to push in the same direction as the higher rates policy does.

The Fed also remains relaxed with the ongoing volumes going back to them on their reverse repo facility. Recently this has ticked back up again towards the US$ 2.2trn area, partly as the US Treasury curbs bills issuance in an effort to smooth the rise into potentially hitting the debt ceiling by mid-2023. That aside, the bond roll-off program has done more than cause the volume of cash going back to the Fed to plateau.

The repo market would like to see this fall. From the Fed’s perspective this is a facility that’s doing its job; mopping up liquidity at 5bp above the funds rate floor. So, no change in the Fed’s tune on this. 2023 should see these volumes ultimately wind lower, albeit slowly over the course of the year.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.