Rates Spark: Primed for Pivot

ING Economic and Financial Analysis | Jan 26, 2023 06:47AM ET

Usually with US auctions this strong, we're in the midst of a bond market rally with considerable room for more. But the downside moves have been tame in fact, despite the recession talk to boot. We think that's because the curve is so inverted that it does not leave the glaring value on longer dates.

Solid US auctions show good demand, but it's heavy going on the downside test

The strong demand at auction in Treasuries has continued this week. Previous weeks saw a good test of demand for the duration as 10yr, 20yr, and 30yr auctions were snapped up. This week we’ve had the 2yr and 5yr auctions so far, and today will see the 7yr auction. The dominant theme has been solid auction results.

It’s not that the paper was well covered. It’s more that the indirect bid has been so consistently large and solid. The indirect bid will typically be bolstered by foreign demand, and in shorter-dated auctions especially, will be populated by the demand from global central banks. On top of that, the primary dealer takedown has tended to be on the low side, primarily as their support has not been needed very much, which is a good thing from the context of the quality of the auction results. And finally, the pricing at all of the auctions has been solid. None of them have tailed.

Downside to yields is supported by the growing evidence of recession and falling inflation.

Despite all of that, we still see the 10yr at or about 3.4% to 3.5%. It seems this is an area of perceived fair value right now, or at the very least a point of equilibrium. The downside to yields is supported by the growing evidence of recession and falling inflation . But there is still upside risk coming from the pronounced inversion of the curve which sees the 10yr optically rich to the front end.

This is why next week’s Federal Open Market Committee meeting is crucial. The market has convinced itself that a dovish 25bp hike is coming. If the Fed instead goes for a more hawkish hike, it stretches that 10yr valuation even more. There is a route to lower yields, but it's far from straightforward should the Fed stick to the hawkish tilt.

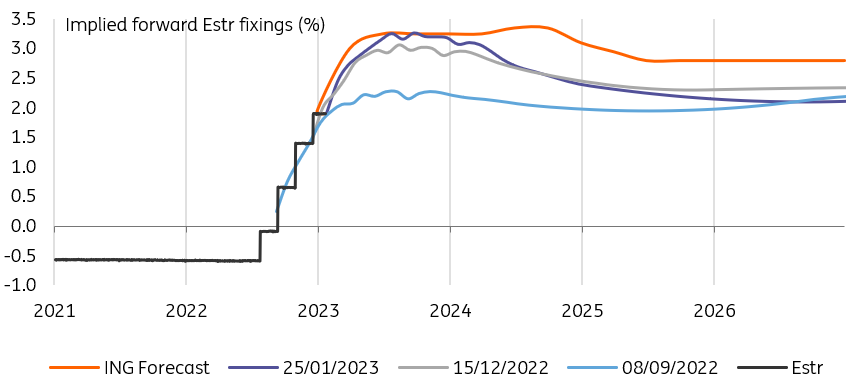

ECB struggles to push up rate expectations beyond the next few quarters

Source: Refinitiv, ING

ECB speakers' final hawkish push with fading impact out the curve

European Central Bank officials have used the final day ahead of the quiet period to reiterate their hawkish message. With the job of reining in inflation not done yet, the ECB’s Vasle argued that 50bp hikes at the next two meetings were needed. Both the Bundesbank’s Nagel and Ireland’s Makhlouf would not exclude that rates will need to rise further after March.

The longer end of the EUR curve is increasingly taking its cues from the US, not the ECB

The market discount is broadly aligning with the ECB comments regarding the next couple of meetings with the forwards pricing rates 92bp higher with the March meeting and good chances for at least one 25bp hike in the following months.

Thereafter if market pricing diverges from the ECB narrative, rates may have to be held in restrictive territory for some time before the underlying is finally tackled. The longer end of the EUR curve is increasingly taking its cues from the US where the Fed is seen close to the end of its cycle and recession angst is taking over.

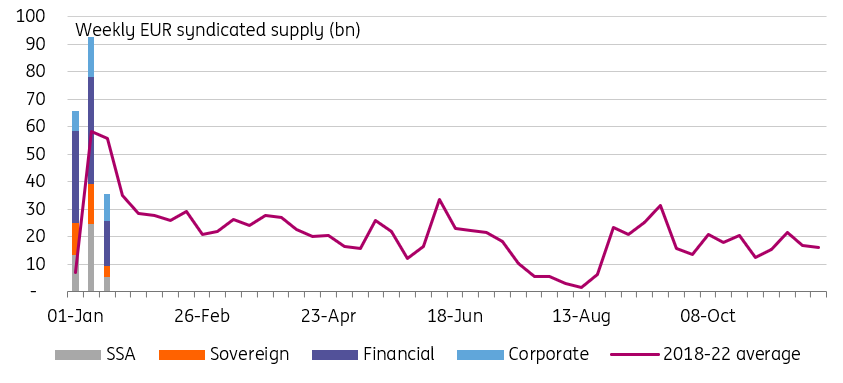

Front-loaded issuance is sending steepening impulses

Source: Refinitiv, ING

In the euro area supply proves more of a headwind

While yesterday’s last hawkish ECB comments seem to have helped turn the market during the session, halting a rally in Bunds that saw the 10Y dipping briefly below 2.10% again, we think this would overstate the ECB’s ability to influence the long end of the yield curve in current markets.

Rather we think the ECB got another assist from the long-end core government bond supply. Not only were the results of the German 15Y and 20Y bond auctions yesterday on the softer side, but later in the day Finland also mandated a 3bn 15Y bond deal which some might have had in the cards only for early February. Overall this year's supply has been much more front-loaded compared to the past years.

Today's events and market view

Central bankers have had their say ahead of the upcoming policy-setting meetings. In the meantime, markets will have to turn to data and supply for cues, though we also see a risk of profit-taking closer to next week’s meetings themselves.

For today the market will have to digest US fourth quarter GDP data, which is expected to have expanded still in excess of an annualized 2%. That should not distract from expectations that the outlook for GDP is already decisively weaker for the next few quarters. The durable goods orders released today should paint a weak underlying picture once a one-off in aircraft orders is stripped out. We will also get the weekly initial jobless claims data.

In supply, the EUR rates could see steepening pressure from the 15Y deal out of Finland, which should be today’s business. We will see shorter-dated bond auctions from Italy. In the US the focus is on the US$35bn 7Y auction, which caps off this week’s supply. It follows a streak of well-received auctions that have underpinned market strength that has also spilled into EUR rates.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.