Rates Spark: How To Price A Recession

ING Economic and Financial Analysis | Jun 23, 2022 05:22AM ET

Have market rates peaked? We are getting close, but are not seeing a conclusive message that the top is in just yet. Inconsistent curve dynamics and the sharpest sell-off in two decades mean the bond market isn’t the obvious place to look for signs of recession.

Were this to become the market’s main focus, we look for divergence between US and European curves.

On turning point watch. But it's never easy or straightforward

So have we seen a turning point? Has the 10Yr peaked at 3.5%? Has the 2Yr peaked as it now races back down towards 3%? The answer is probably not. For two reasons. We still think that real rates have room to rise.

The 10yr is now at 60bp. Our target remains 1%. Second, the 5Yr remains cheap to the curve and consistent with a bearish market. That all being said, could there be a chink of reversion here? Answer, yes.

A notable move today has been a decompression of the cheapness attached to the 5yr. It now trades at about 11bp cheap to the curve (in net terms). That’s in from 14bp in the past couple of days.

That’s a big move, but it has not broken the range seen in the past number of months. It has been at 9bp cheap on a few occasions in the past couple of months. If it were to break down to 9bp and keep going, we’d really start to question whether we’ve seen the peak already.

"We identify 3Q as the quarter in which market rates peak"

And that’s not impossible. All the talk out there is on recession, and former NY Fed President William Dudley has given us a timely reminder that the US savings rate is fast-tracking towards 4% (having been in the 20% region during the pandemic).

That’s a signal of contemporaneous strength, but poses forward-looking risks to the ability to maintain consumption expenditure at elevated levels. This market is in a mood to look through the tight labor market and look forward to the slowdown/recession.

Should that continue, then the peak in rates is indeed in. As a central call though, we doubt we are there yet. There is too much inflation risk and not enough macro angst (just yet) to bring the bear market for bonds to a complete close.

We are getting close though. We still identify 3Q as the quarter in which market rates peak and ultimately begin a journey lower.

Bonds aren’t behaving like recession hedges

Bonds have a patchy record in pricing recession risk so far this year. In an environment where inflation has taken precedence over growth in central banks’ policy decision-making, this is understandable.

The fall in some commodity prices this week opened the door to a regime where a cooler near-term outlook for inflation allows central bankers to focus on the medium term picture.

In theory, this could translate into fixed income becoming less of an investment pariah, provided old relationships between slowing economic activity and inflation apply.

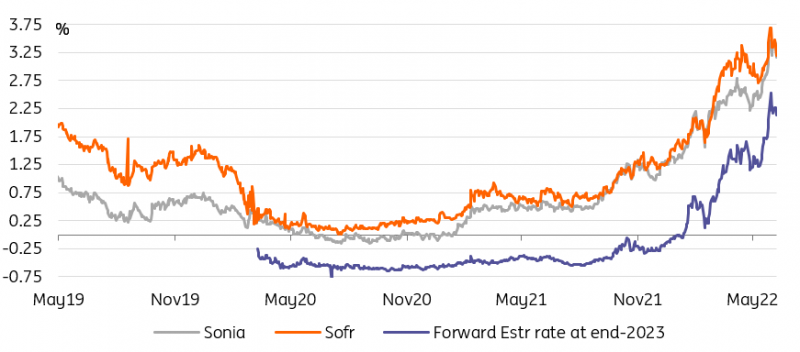

The Estr and Sonia curves are pricing too high a 2023 terminal rate

"The degree of tightening priced by some yield curves, and in particular European ones, has reached extreme levels"

It is probably too early to call for a change in market regime just yet, although a double-digit rally across developed market rates curves yesterday gives credence to this view.

The combination of Fed Chair Jerome Powell being increasingly candid about the recessionary risk brought on by aggressive policy tightening, and the fall in some key commodity prices were the key reasons behind the re-pricing.

Regardless of whether this is the beginning of a change in market regime or merely a vicious counter-trend rally, it illustrates the fact that the degree of tightening priced by some yield curves, and in particular European ones, has reached extreme levels inconsistent with a decline in inflation next year.

Recession risk in Europe could come with steeper curves

It is worth remembering at this stage that GBP and EUR OIS curves are pricing a terminal rate for the Bank of England and for the European Central Bank that are respectively 125bp and 175bp above our own economists’ estimates.

Admittedly, it is uncomfortable to be so far out of line with what the market is pricing. The reason we’re not calling for a sharp adjustment lower in rates just yet is because the part of the forwards curve we happen to agree with is the near-dated one.

In our view BoE and ECB tightening cycles will meet a much earlier end than implied by swaps, well before 2023, leaving up to six months of potential bond market sell off.

Don't listen to the yield curve, recession risk isn't lower in the eurozone

"BoE and ECB tightening cycles will meet a much earlier end than implied by swaps"

The other place where recession risk should in theory be reflected is the shape of the yield curve. Here too the market’s record is patchy. We flagged in yesterday’s Spark that the US curve inversion is both a consequence and a key input into the market’s perceived recession risk.

As it happens, the EUR curve is far from sending the same signal. Worst still, if we’re right in expecting the ECB tightening effort to fizzle out by the end of this year, it is entirely possible that the curve steepens further still, as the market reassesses the probability of 2023 hikes.

Today’s events and market view

The US calendar is no less busy with current account, jobless claims, PMIs, and Kansas City Fed manufacturing index.

Fed Chair Jerome Powell follows up yesterday’s Senate testimony with a similar intervention, this time in front of the House of Representatives.

Realistically, the scope for new information to be released in this exercise is limited since it is the second one in two days. Banque de France and Bundesbank Governors Francois Villeroy and Joachim Nagel were to speak at a Bundesbank event.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.