Rates Spark: All About Inflation

ING Economic and Financial Analysis | Nov 30, 2023 07:38AM ET

By Benjamin Schroeder & Padhraic Garvey

The rates rally found its confirmation in German and Spanish inflation data ahead of today's eurozone release, but finally seemed to pause after more hawkish Fed comments. A reassessment of inflation has been the main driver of the EUR rally since rates peaked in October, but the real component still played a larger role in the US

Bull Steepening On Inflation Data, But Finally Running Into Some Resistance

The bond rally in EUR rates found confirmation in the softer German and Spanish inflation estimates for November. They point to a larger-than-expected drop in today’s eurozone flash estimate. For the European Central Bank that means 2024 could bring a first rate cut. Whether this will be as early as the market currently prices remains questionable though. A first rate cut is close to being fully discounted now for April. Overall some 110bp in cuts are discounted for the year as a whole.

The ECB’s Stournaras of Greece, one of the more dovish ECB members, told Politico yesterday that he thought markets betting on April were too optimistic in his view. But he did see a cut in mid-2024 as possible. Early rate cut hopes for now ignore the ECB’s more cautious approach to inflation having vastly underestimated price pressures in the past.

US rates stabilized with 10Y UST yields failing to move past the 4.26% mark, but the front end continued to slide lower with the 2Y yield coming close to touching 4.6%. It was only after hawkish comments from the Fed’s Barkin that rates moved higher when he argued it was premature to be talking about rate cuts. The market still begs to disagree and already discounts a 50% probability for a cut in March and more than fully prices a cut in May. US markets discount 117bp in cuts over 2024.

Dissecting The Past Month’s Rally In Rates

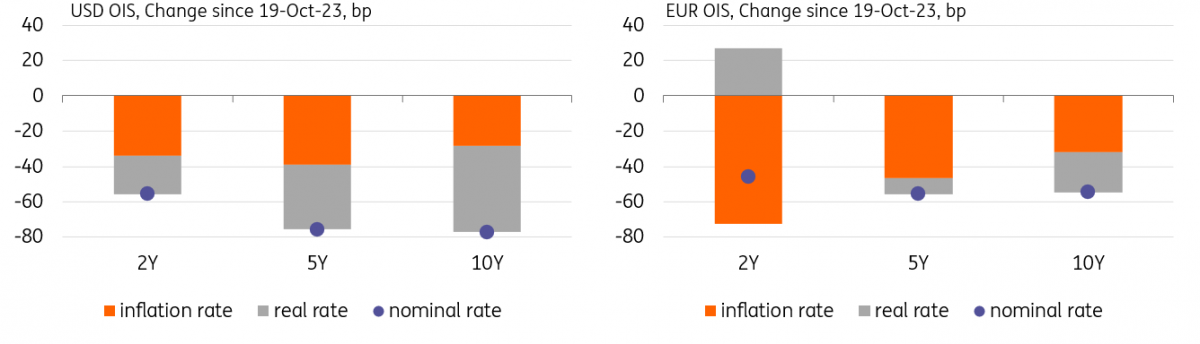

When decomposing the rally of nominal OIS rates since their peak on 19 October into their real and inflation components we find confirmation that the reassessment of inflation has been the main driver of the EUR market, especially at the front end. That should give ECB officials some comfort as the market is rallying for the right reasons, even if the central bank is more cautious on inflation.

In the US inflation expectations have come down notably as well, but the real interest rate component has played a larger role in driving nominal rates lower, especially at the long end where the market had previously been more concerned about the high US deficits.

The Inflation Reassessment Has Played A Bigger Role In EUR Markets Than In The US

Source: Refinitiv, ING

Today’s Events and Market View

Today’s session will still be all about inflation. In the eurozone, markets are eyeing the flash CPI for November. The consensus is for a 2.7% year-on-year reading for the headline after 2.9% in October. But following the German and Spanish inflation data yesterday, the actual figure could come in lower. Core is expected at 3.9% after 4.2% last month.

We will also be watching ECB commentary. The usually very dovish Panetta speaks for the first time in his role as the head of the Bank of Italy today. Bundesbank’s Nagel is scheduled to speak early in the evening, but we have heard from him already earlier this week.

In the US the focus is on the PCE data, the Fed’s favored inflation measure. Here the market is looking for a 3.0% year-on-year figure for the headline and 3.5% for the core. We will also get initial jobless claims data, which markets have been relying to a greater degree on lately to gauge the temperature in the jobs market.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.