Q1 Earnings Surprise Masks a Deeper Sector Rotation

Brian Gilmartin | May 05, 2025 01:00AM ET

This table shows the sharp jump in just the last week in the Q1’25 S&P 500 EPS expected growth rate (from +9.7% expected last week to +13.6% expected this week) and the subsequent lower revisions for Q2’25.

Source: LSEG Earnings Scorecard

The upside surprise per the LSEG data is +7% for Q1’25 S&P 500 EPS, while it’s just +0.9% for Q1’25 revenue, showing some margin control within the S&P 500 companies that have reported earnings. In Q3 ’24 and then early ’24 we saw +7.5% – 8% upside surprises in S&P 500 EPS, but that’s rarified air typically.

Looking at the sector level changes to expected 2025 sector growth rates, the communications services sector jumped sharply this week, likely due to Meta Platforms (NASDAQ:META), to +14.8% from last week’s +10.4%, while technology also increased slightly to +16.8% from +16.5%. Every other sector was lower except financials, which increased slightly.

The Fishhook Pattern

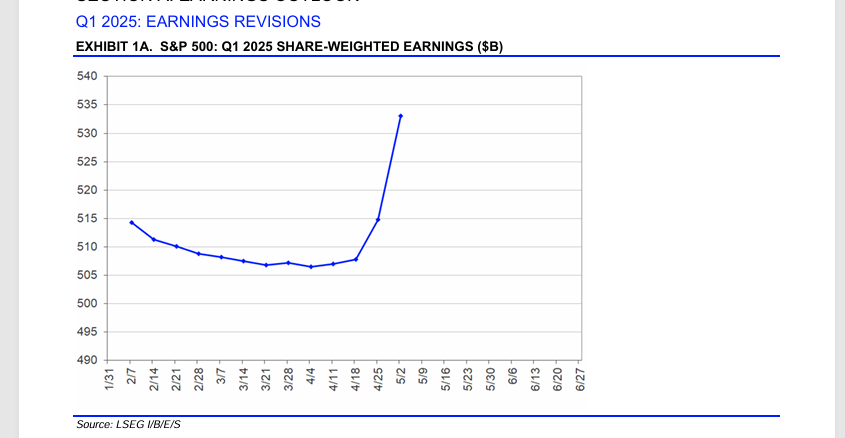

If you have ever heard Ed Yardeni refer to the fishhook pattern, here it is, but it’s actually a reverse fishhook pattern if you look at earnings chronologically.

This pattern repeats itself almost every quarter, where sell-side analysts and strategists grow conservative in front of a quarterly earnings season (in this case Q1 ’25) and lower estimates, only to see the actual results, thanks to the upside surprise patterns, be greater than what was estimated.

What’s interesting for me is that LSEG gives readers “net income” levels, which you can see from the chart started around $515 billion in early February ’25, sank until early April ’25 where expected net income bottomed around $507 billion, and then since Q1 ’25 earnings season began, are now well over $530 billion, and again this is net income, not EPS so EPS would be boosted further from share buybacks.

Conclusion

Don’t try to time the market tracking S&P 500 earnings estimates as this article in late November ’24 discussed. Estimates can be helpful in tracking sector growth rates. Upward revisions to sector EPS growth rates are more telling to an investor than the downward revisions, since the typical pattern in a normal quarter is to see downward revisions for the last two to three months before a quarter is reported.

With the Presidential tweets, headlines, and possibly Fed rate cuts coming this year, it seems harder to predict what Q2 and Q3 ’25 might look like from an S&P 500 earnings perspective. Fed funds rate cuts are usually an unambiguous positive, but there’s the tax bill, etc.

Despite the headlines, there are still a lot of positives that could happen this year, and I’m not a raging bull.

What impressed me most was the changing market leadership year. Non-US, like Europe, is +10% through April 30, and the emerging markets saw a little pop today (i.e. EMXC, EEM, VWO) after China signaled last night they are ready to engage with the US on tariffs. As of April 30, 2025, the typical “balanced” portfolio (60% equity / 40% bonds) was down -1.79% YTD.

High yield credit spreads peaked in early April ’25 and have steadily come down. Not so ironically, high-yield spreads were at their tightest when the S&P 500 was near its all-time high in mid-February.

The tax bill, while it won’t be what was passed in 2017, would help if the corporate tax rate is reduced, but I wouldn’t expect it to be lowered much more than 2% – 3%, from the current 21%. (This is probably not in the strategist EPS estimates for ’25, it’s still a little early yet.)

Disclaimer: None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results.

Thanks for reading.

More to come this weekend.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.