Pre-Asia Open: Emerging From the Valley of the Bears

Stephen Innes | Mar 17, 2023 01:47AM ET

US stocks are trading definitively higher Thursday. In a true sign of confidence returning to Wall Street, Treasury yields are heading up as markets digest the news that Credit Suisse (NYSE:CS) intends to access two facilities from the Swiss National Bank.

While uncertainty around the US and Europe banks sector remains elevated. Still, with investors emerging from the “ Valley of the Bears, "markets today exhibit at least an incremental comfort level as stocks rise and bonds fall (pushing up yields).

Today's relief comes amidst a flurry of SNB backstop news, and on hope, we will get less terrible headlines around the banking sectors.

This multi-mash comes ahead of next week's FOMC meeting. Investors are still undecided about whether the Fed will prioritize financial stability or the inflation problem. Yields on 1-year T-Bills are up +23bp today to 4.51%., suggesting the pendulum is swinging to the later post-ECB rate hike.

While macro data is equally available for central banks and market participants, central banks have better visibility on micro-data, which matters most currently. Hence the good news for markets is that despite investors in stress test mode, the ECB felt comfortable sticking to guidance and hiking rates by 50 bp.

Still, the bad news for the EUR/USD is the ECB hiked 50 bp. For now, with Lagarde & Co hiking in an environment of heightened stress, it is not clear if this would be immediately helpful for the currency.

But anything short of a 50 bp hike today would have made the ECB look soft. That said, President Lagarde toned down the hawkishness to emphasize the data-dependency of their decision-making and that it will be done on a meeting-by-meeting basis. And, of course, they are "ready to respond," if needed, to ensure price and financial stability. Indeed that was about as skillfully crafted a response as a "top of the line "handmade Swiss watch. Hence at minimum, the EURO should do well on the crosses.

And with stock market investors emerging from the "Valley of the Bears," the post-ECB reaction could hint at how “The Street” may behave next week if the FED stuck to the inflation-fighting game plan and hiked 25 bp.

OIL MARKETS

With troubles in Zurich receding and energy traders coming around to the idea that this is not a 2008 reboot and where bank stress is poles apart, oil traders appear to be getting more comfortable buying dips than simply selling rallies.

Much money has been made and lost in the oil markets since the peak of China's reopening euphoria hit in mid-Feb. But looking at USD/CNH trading at 6.90 rather 6.80 suggests that cross-asset and FX traders are still circumspect about Mainland economic revival, so I suspect markets are in need of some true physical tightening before the paper market flies again.

GOLD MARKETS

On a correlation basis, gold’s “ bank run premium “looks a tad expensive, as does bullion recession premium with Treasury Yields moving higher. While my fund is 100 % price agnostic as we invest long gold same time same amount every month, we are pulling off long spec paper despite the possibility that gold could move higher as a weekend headline hedge.

TRADING

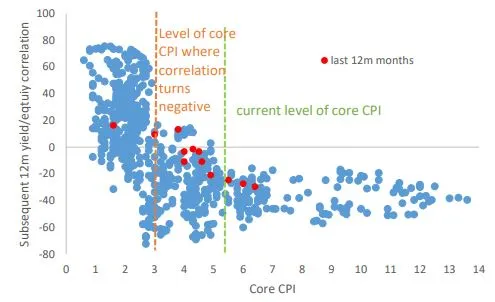

When inflation becomes an issue, a positive shock to inflation will coincide with a negative shock to growth, leading to higher bond yields and lower equities, i.e., a negative correlation between bond yields and equities. Empirically, when US core CPI is above ~3%, the subsequent 12m yield/equity correlation tends to be negative.

With core CPI at 5.5%, the yield/equity correlation should remain negative for now. In such an environment, bonds should command a higher risk premium as bonds are no longer a good hedge for equities.

From an equity perspective, the negative yield/equity correlation implies that a negative demand shock may initially be good for equities as (presumably) a lower discount rate and reduced inflation risks outweigh the impact on earnings. However, if the demand shock is large enough to bring inflation back below 3%, history suggests that the correlation will revert.

The yield/equity correlation is likely to remain negative for now.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.