Monetary Policy Is Not Expansionary

Lance Roberts | Jul 16, 2021 05:38AM ET

Monetary policy is not expansionary despite widespread belief otherwise.

The general assumption by the Federal Reserve is that by providing excess reserves to the banking system, the banks would then lend to businesses and individuals to expand economic activity. Furthermore, as discussed previously, the Federal Reserve’s entire premise of inflating asset prices was the subsequent boost to economic activity from an increased “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” – Ben Bernanke

However, after more than a decade of “monetary policy,” there is little evidence that supports those claims. Instead, there is sufficient evidence that “monetary policy” leads to greater wealth inequality and slower economic growth.

Prima Facie Evidence

The only reason Central Bank liquidity “seems” to be a success is when viewed through the lens of the stock market. Through the end of Q2-2021, using quarterly data, the stock market has returned almost 198% from the 2007 peak. Such is more than 8x the GDP growth and 3.9x the increase in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not AS subject to manipulation.)

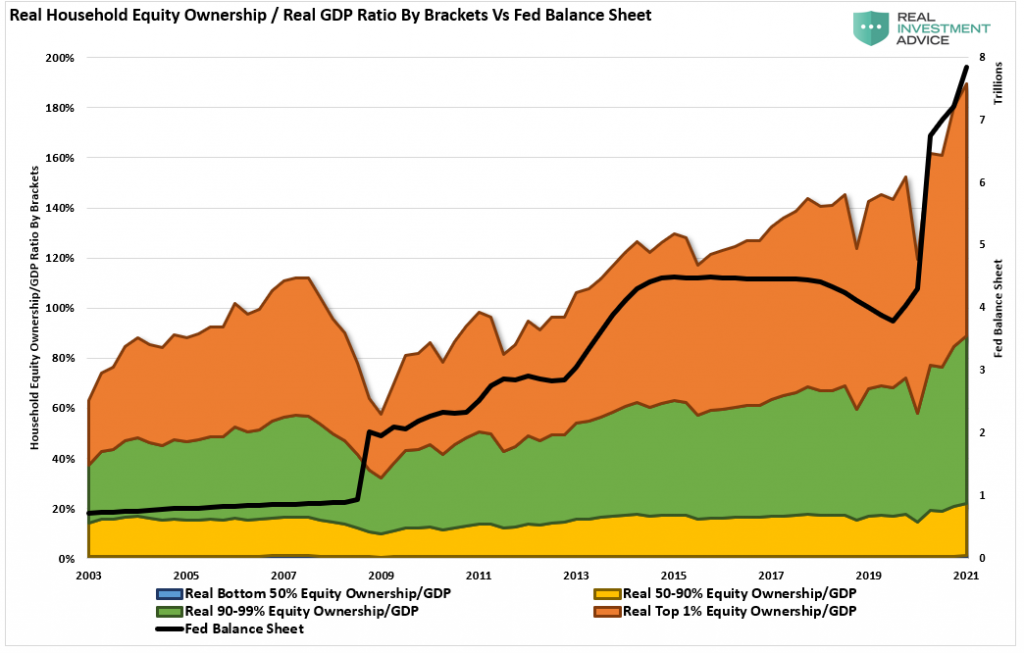

Unfortunately, the “wealth effect” impact has only benefited a relatively small percentage of the overall economy. Currently, the top 10% of income earners own nearly 90% of the stock market. The rest are just struggling to make ends meet. Thus, the impact of the Fed’s monetary interventions on the equity value of the top 1% is evident.

While short-term ongoing monetary interventions may appear to be expansionary, it creates negative incentives to economic activity and monetary velocity.

QE Has A Negative Incentive

As noted above, the Fed suggests that by providing excess reserves to the banking system, the banks will then “lend” those reserves. In turn, as businesses borrow money to expand production or consumption, the economy gets a lift.

However, in reality, it is precisely the opposite. Each time the Fed has engaged in QE programs, the banks “hoard” those reserves as the “risk/reward” of loaning money into the economy is not justified. For example, in early 2020, as the economy was “shut down” due to the COVID pandemic, companies tapped credit lines at their banks to ensure sufficient capitalization. After that initial surge in lending activity, banks reversed back into a more “protectionary” mode.

I say “afloat” rather than “growing” because, since 2008, the total cumulative growth of the economy is just $3.5 trillion. In other words, for each dollar of economic growth since 2008, it required $12 of monetary stimulus. Such sounds okay until you realize it came solely from debt issuance.

Government Spending Has A Negative Multipler

Here is the problem. Excess “debt” has a zero to a negative multiplier effect. Such was shown in a study by the Mercatus Center at George Mason University by economists Jones and De Rugy.

“The multiplier looks at the return in economic output when the government spends a dollar. If the multiplier is above one, it means that government spending draws in the private sector and generates more private consumer spending, private investment, and exports to foreign countries. If the multiplier is below one, the government spending crowds out the private sector, hence reducing it all.

The evidence suggests that government purchases probably reduce the size of the private sector as they increase the size of the government sector. On net, incomes grow, but privately produced incomes shrink.”

Notably, politicians spend money based on political ideologies rather than sound economic policy. Therefore, the findings should not surprise you. However, the conclusion of the study is most telling.

“If you think that the Federal Reserve’s current monetary policy is reasonably competent, then you actually shouldn’t expect the fiscal boost from all that spending to be large. In fact, it could be close to zero.

This is, of course, all before taking future taxes into account. When economists like Robert Barro and Charles Redlick studied the multiplier, they found once you account for future taxes required to pay for the spending, the multiplier could be negative.”

Monetary policy, in its current form, is not helping the economy. As a result, the Federal Reserve has lost the ability to influence economic growth.

Conclusion

The Federal Reserve has no real options unless they are willing to allow the system to reset painfully.

Unfortunately, we now have a decade of experience of watching monetary experiments only succeed in creating a massive “wealth gap.”

Most telling is the current economists’ inability to realize the problem is trying to “cure a debt problem with more debt.”

In conclusion, the Keynesian view that “more money in people’s pockets” will drive up consumer spending, with a boost to GDP being the result, has been wrong. It hasn’t happened in 40 years.

The reality is that monetary policy is not expansionary but rather contractionary. Unfortunately, deflation remains the most significant threat as permanent growth doesn’t come from an artificial stimulus or debt.

But such is a lesson that has yet to get learned.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.