Market Taking Stock Of Dollar Direction

Dean Popplewell | Oct 07, 2013 07:52AM ET

Capital markets are still waiting for common sense to prevail. It’s the most basic of ingredient that is required by Washington to resolve the federal budget impasse and to tackle the federal debt ceiling debate whose deadline for many is becoming too close for comfort (October 17th). Some members of Washington are playing ‘high stakes poker’ apparently blind. This is somewhat similar to many investors who have been left with less economic news and guidance due to the partial shutdown of the federal government. The market continues to hold a view that the US situation will find a resolution.

Friday’s no-show US jobs report – the granddaddy of economic indicators – is technically the beginning of a slew of economic releases that is expected to be shelved until after the US government shutdown is broken. When all agencies are back to work the market can expect a cascading of mostly irrelevant data points to be battered about until “lost time has caught up with the present.” Based on the original schedules pre-shutdown, the main focus for traders this week will be the Feds minutes of the September 17-18 FOMC meeting mid-week – current federal budget issues do not affect this release.

The market will be expecting this mid-week release to provide some extra clarity on when the Fed’s monthly $85b bond buying program may begin to taper. Next up will be the US retail sales release this coming Friday – it remains a key reading on the domestic consumer sector. However, do not be surprised to find that various Federal government indicators release dates may continue to change due to a fiscal budget impact on both the Commerce and US Labor Department work schedules. Any indicators produced by the Fed’s and any private companies remain not affected. Investors should remain alert that indicators not released this past week might be released this week on an “unscheduled” basis if Washington politicking and federal budget issues are resolved.

If anything, the situation in Washington is probably a tad worse off as we enter the second week of the US partial government shutdown. Mr. Boehner, Speaker of the House of Representatives, said his Republican majority would not pass bills to fund the government or increase the debt ceiling unless the Obama administration was willing to make concessions on health care – there is nothing new in this, however, this is more than domestic high stakes politics.

Any threat to the tentative US growth schedule that capital markets have become accustomed to of late will only have a negative knock-on global impact. Up to this point, the various asset classes have been trading with a quick resolution in mind – markets have grown used to a Washington shenanigan showdown as least every three months since Obama’s first term of office. However, this time around, Boehner insists, “there are not the votes in the House to pass a clean ‘continuing resolution’ (short-term funding measure with no strings attached that would allow the government to reopen). The debt ceiling would not be increased unless the White House addressed long-term spending and budget issues. Financial markets have so far reacted relatively calmly to the impending debt deadline – investors have somewhat brought into the idea that lawmakers would be able to lift the debt ceiling. However, the stellar comments by the House speaker over the weekend could add further unease to a market who probably half believed we would not have gone so deep with the political brinkmanship.

The sooner the US can eliminate its fiscal policy uncertainties the sooner global markets can go on about their own business. The might dollar trades in relative “no-mans land,” a touch softer as the partial US shutdown enters its second-week. With October 17th fast approaching, the more apprehensive capital markets will become in respect to the US debt ceiling deadline. Overall, the market continues to hold a view that the US situation will find a resolution, albeit maybe at the last minute.

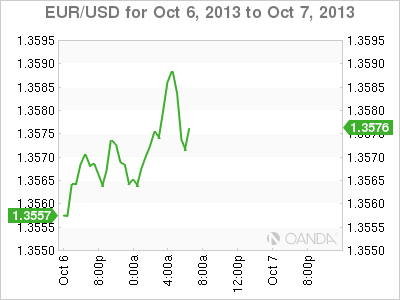

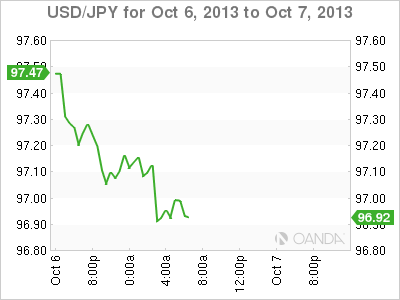

The 17-member single currency currently remains entrenched in a three-cent scope, 1.34-1.37 consolidation range, with some dealers believing its upside could run out of steam and while a re-test of the 1.3645 and 1.3710 peaks cannot be ruled out in the near term. Against sterling, the GBP has rebounded from last week’s late sell-off (1.6059), with dealers noting that the gains have mostly been driven by the plethora of positive economic UK data surprises. The BoE meet this week – governor Carney’s “lower rates for longer” will surely be challenged, again. The current yen direction is mostly been swayed by the direction of its domestic equity indexes. In the overnight session USD/JPY was able to print a fresh one-month low below 96.90 after the Nikkei225 again slumped by -1.2% to close below +14k. So far, the mighty dollars decline remains gradual as traders remain reluctant to bet heavily against it while not knowing when lawmakers may make a compromise. Any heighten concerns of US debt default will only push US Treasury yields higher and have global bourses trading further into the ‘red.’ Investors will try and remain tight with their “wait and see” approach.

Original post

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.