Looks Like A Correction Is Brewing

Cam Hui | Feb 02, 2015 12:07AM ET

Trend Model signal summary

Trend Model signal: Risk-off

Trading model: Bearish (downgrade)

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. In essence, it seeks to answer the question, "Is the trend in the global economy expansion (bullish) or contraction (bearish)?"

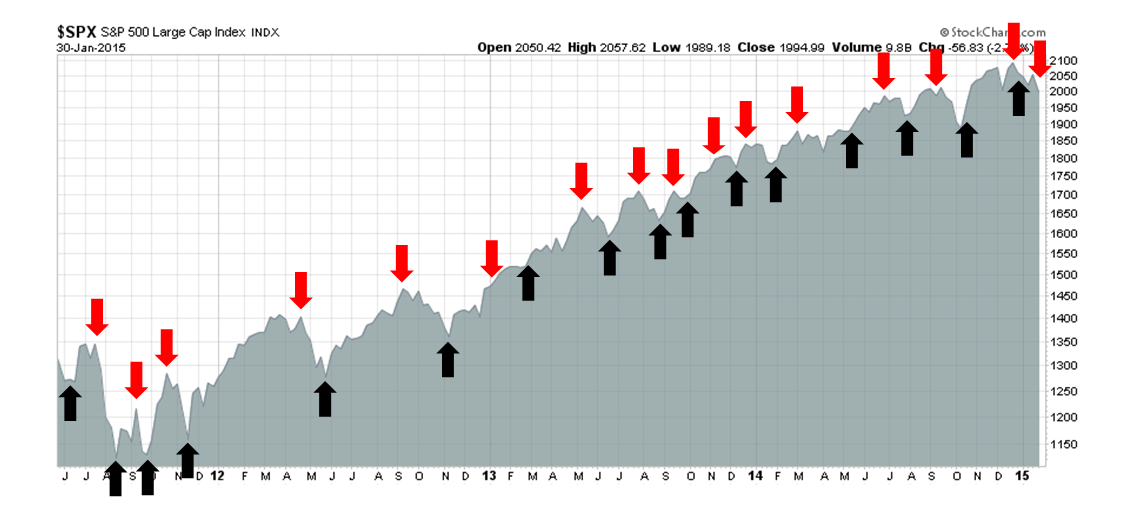

My inner trader uses the trading model component of the Trend Model seeks to answer the question, "Is the trend getting better (bullish) or worse (bearish)?" The history of actual (not backtested) signals of the trading model are shown by the arrows in the chart below. In addition, I have a trading account which uses the signals of the Trend Model. The last report card of that account can be found here.

Update schedule: I generally update Trend Model readings on weekends and tweet any changes during the week at @humblestudent.

Outlook is turning bearish

In the past week, the outlook has turned decidedly negative for the following reasons:

- Commodities are signaling a lack of demand.

- US EPS estimates continue to deteriorate.

- Uncertainty is rising in Europe.

Let's go through these factors, one by one.

Commodities signaling weak global economy

Commodity prices have been falling for quite some time and they represent a key input to my Trend Model. Historically, falling commodity prices have signaled weakness in the global growth outlook. In my last post (see Good news, bad news on the commodity downturn), I struggled to find reasons—such as USD strength and the de-financialization of commodities as an investment—to explain the downtrend. Perhaps this time is different?

Alas, this time is NOT different. Even if we to filter out the effects of the strong USD, the picture isn't pretty. The chart below shows the CRB Indexdenominated in euros. Even in euro-terms, the CRB remains in a downtrend.

The chart of industrial metals in euros is a bit more constructive as it appears to have rallied through a downtrend and seems to be trying to stabilize.

Overall, I would rate the message from the commodity market as neutral to negative at best. Mr. Market is telling a story of a lack of global demand, which is not helpful for the growth outlook and risk appetite.

The failing grade from US Earnings Season

In the US, the equity outlook is deteriorating. The latest analysis from John Butters of Factset shows that forward EPS continues to fall. As the chart shows, falling consensus EPS has historically been associated to either corrections or bear markets (annotations in red are mine).

In the past few weeks, I had been cautiously bullish as I waited for EPS estimates to turn up as the benefits of lower oil prices became more clear. It`s time to throw in the towel on that thesis.

Earnings Season is in full swing with 227 of the companies in the S&P 500 having reported their Q4 results and there is no sign of an upturn in estimates. The earnings beat rate is 80%, which is well above the historical average, and the sales beat rate is 58%, which is roughly in line with past history. The more disturbing result is the negative guidance rate, which is a whopping 80% and has consequently pushed down estimate revisions.

While Energy stocks have born the brunt of the earnings downgrades, Bespoke showed that negative guidance was not restricted to just energy:

The gloom is spreading, according to Bloomberg (emphasis added):

U.S. chief executive officers are more pessimistic about corporate earnings than any time since the financial crisis, according to research from Bespoke Investment Group LLC.The percentage of companies cutting profit forecasts during this earnings season has outpaced those with upward revisions by 8.6 percentage points, the widest margin in six years, according to data compiled by Bespoke. Consumer companies and drugmakers are the most bearish among 10 major industries, with at least 18 percent of each group providing lower guidance, the data show.

The Street is now projecting negative EPS growth in Q1 and Q2:

Analysts now expect per-share earnings from SP 500 companies to decline 2.1 percent in the first quarter and fall 1.1 percent over the following period, estimates compiled by Bloomberg show. Should the forecasts come true, it would be the first back-to-back profit contractions since 2009.

Fundamentally, there are two basic ways that stock prices can advance. Either the P/E multiple expands, the E in the P/E ratio rises, or both. Now consider that (for more details see (Sort of) debunking the bear case for stocks):

- Valuations are elevated;

- The Fed is starting a tightening cycle, which will put downward pressure on P/E multiples; and

- EPS estimates are falling.

The combination of these factors is a recipe for either a bear market or correction. In a more typical mid expansion phase of an economic cycle (especially when energy input prices are falling), the positive effects of rising earnings growth offsets the negative effects of Fed tightening. This time, EPS estimates are falling down on the job.

A WTF Greek moment

Across the Atlantic, the macro picture looks dire on a short-term basis. Late in the European trading day, we saw the news from Greece that they would decline the next round of €7 billion aid without a deal on the conditions surrounding the funds, according to Bloomberg report (emphasis added):

Prime Minister Alexis Tsipras sought to repair relations with Greece’s creditors ahead of a diplomatic push to win support for his economic program, as euro area officials said they’re looking for concessions from the new government.Greece will repay its debts to the European Central Bank and the International Monetary Fund and reach a deal “soon” with the euro-area nations that funded most of the country’s financial rescue, Tsipras said in a statement e-mailed to Bloomberg News on Saturday.

“The deliberation with our European partners has just begun,” Tsipras said. “Despite the fact that there are differences in perspective, I am absolutely confident that we will soon manage to reach a mutually beneficial agreement, both for Greece and for Europe as a whole.”

Yes. WTF would be an apt description of the negotiations.

In the meantime, Greek stocks continue to tank relative to eurozone equities. While the Athens market is oversold on a relative basis, it's still very early in the negotiation process and anything can happen. No doubt there will be much more drama and tantrums in the days and weeks to come. The bottom may not be in yet - and any more posturing by either side is likely to spook the markets.

Stay tuned for more drama and volatility as the markets react to the latest headlines. The stakes are high, not just in Greece, but because of the heightened risk of political contagion as the Guardian reported that 100,000 flocked to Madrid for a Podemos rally .

China the one bright spot

Ironically, the one bright spot that could contribute positively to the global growth outlook is China. Despite the headlines about slowing Chinese growth, analysis of the Shanghai market and the stock market of China's major Asian trading partners (Hong Kong, Taiwan, South Korea and Australia) indicates that they are either in uptrends or in the process of turning up. Such a development must be regarded as a positive development for the bulls and investors may want to look at exposure to "Greater China" for the equity component of their portfolios.

While the Chinese economic trajectory is weakening as the latest official PMI figures missed expectations , the market is in a "bad news is good news" phase as the perception is that weakness is setting the stage for more easing.

A correction, or more choppiness?

The combination of these factors indicate that the path of least resistance for US equity prices is down. Cornelius Luca at Thomson Reuters is seeing signs of declining risk appetite from the credit markets.

On the other hand, the stock market has been volatile and range-bound for the last few weeks and we have to allow for the possibility that, instead of declining right away, it rallies and resumes the choppy pattern. The chart below shows that the SPX has seen its recent declines arrested at the 150 day moving average and the index closed just slightly below that level on Friday. In addition, the 5-day RSI, which is a useful short-term swing trading indicator, is showing a slight positive divergence so the rally scenario remains a possibility.

In response to these changes in market conditions, my inner investor is looking to lighten up his equity positions on strength. A correction is brewing and he wants to be prepared.

My inner trader short position on Wednesday after the FOMC statement, but before the sell-off cascade that occurred in the last hour of trading. He is leaning bearish, but he has been burned too many times in the past few weeks by the market choppiness (see All washed up!). He is therefore keeping his short exposure lower than normal for risk control reasons.

Disclosure: Long SQQQ

Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. ("Qwest"). This article is prepared by Mr. Hui as an outside business activity. As such, Qwest does not review or approve materials presented herein. The opinions and any recommendations expressed in this blog are those of the author and do not reflect the opinions or recommendations of Qwest.

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this article constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or Mr. Hui may hold or control long or short positions in the securities or instruments mentioned.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.