It’s Time To Catch Palantir Stock

MarketBeat.com | Jan 26, 2022 04:34AM ET

Enterprise and government data analytics services provider Palantir Technologies (NYSE:PLTR) stock has fallen nearly (-20%) in 2022. The growth stock has fallen more than (-60%) from its peak price of $45 at the beginning of 2021. While shares are much cheaper, they aren’t exactly at bargain levels yet.

The Company has no debt and a fortress balance sheet. The enigmatic company is a pioneer in big data analytics and the utilization of artificial intelligence (AI) to create solutions and bolster effectivity and outcomes for enterprises.

Top line continues to grow at 35% despite being an 18-year old company. Prudent investors with a longer-term horizon seeking exposure in cutting edge data applications can watch for opportunistic pullbacks in shares of Palantir.

Q3 Fiscal 2021 Earnings Release

On Nov. 9, 2021, Palantir reported its fiscal Q3 2021 results for the quarter ending September 2021. The Company reported an earnings-per-share (EPS) profit of $0.04 matching consensus analyst estimates for a profit of $0.04. Revenues grew 35.5% YoY to $392.2 million, beating analyst estimates for $386.46 million.

The Company added 34 net new customers and grew commercial customer count 46% quarter-over-quarter (QoQ). Palantir closed 54 deals of $1 million or more with 18 of those deals worth over $10 million. Total remaining deal value rose 50% YoY to $3.6 billion. Cash flow from operations was $101 million representing a 26% margin.

Upside Guidance

The Company also expects Q4 2021 revenues around $418 million versus $401.87 million consensus analyst estimates. Palantir expects annual revenue growth of 30% or greater between 2021 and 2025.

Conference Call Takeaways

Palantir Chief Operations Officer Shyam Sankar set the tone,

“It was a fantastic quarter across the board. In Q3, total revenue grew 36%. Commercial revenue growth has accelerated in every quarter over the last year, from 4% in Q4 2020 to 19% in Q1 to 28% in Q2. Now, 37% in Q3. At this scale, acceleration like this, it's gravity defying. U.S. commercial revenue growth accelerated once again to 103% year-over-year.

"We added 34 net new customers in Q3. To put this in perspective, our commercial customer count grew by 46%, sequentially. We have more than doubled our commercial customer count since the beginning of the year. We closed 54 deals of $1 million or more, 33 of which were $5 million or more, and 18 of which were $10 million or more.”

He continued,

“There are so many wins this quarter. Instead of going through them customer by customers as I usually do, I wanted to highlight 3 themes. (1) We are seeing more traction selling into the defense industrial base as a customer. Foundry has shown that it can help in the production of the A-320 of Ram pickup trucks, auto parts, PPE and tractors. It can do it better, faster, and cheaper. And the defense industrial base is seeing that it can have the same impact on the production of fighter jets, naval ships, and land vehicles. We are excited to do more here with L3Harris, Huntington Ingalls (NYSE:HII), and other large primes.

Get The News You Want

Read market moving news with a personalized feed of stocks you care about.Get The App"Secondly, our work in automotive, and more generally, mobility is growing. We are adding more customers across the mobility value chain, from OEMs and their suppliers all the way to EV charging companies and insurers. And lastly, our work in healthcare is exploding. The NHS, MD Anderson, 70 academic medical centers through the NIH’s N3C, the Department of Veteran Affairs, and even more regional U.S. providers means that Foundry is helping to manage over 300 million patient lives and growing.

"We have a very unique opportunity and a diverse footprint that we believe continues to uniquely position us deliver on the necessary transformation in healthcare delivery from operational excellence to complex clinical care. Cutting-edge product and continued innovation and distribution drove these exceptional results in Q3.

"And you can really see that in the consistently accelerating commercial business. We are seeing a profound pull on foundry in the market as organizations digest and synthesize lessons from the shocks of COVID and subsequent events, there is a canonical spot for foundry in the enterprise architecture that the market has synthesized. Foundry is the nervous system and the cardiovascular system of the enterprise. It is the connective tissue that connect your analytics to your operational systems.

"Such an architecture marries a digital twin of the enterprise with action APIs that allow you to first model and simulate and second orchestrate and execute complex, cross-functional transactions. As the COVID-19 crisis pulled the tide out, that's exactly what was revealed as missing. Companies needed to move beyond visibility, beyond analytical insights to having the technical infrastructure to translate that into coordinated, orchestrated actions in the operations of their business.

"And one of the coolest places to see this working is with our day zero companies. These companies have enormous ambition and deeply value the step change in speed and the reduction of expenses foundry delivers when consumed as infrastructure as a service. Wejo (NASDAQ:WEJO) was able to develop market ready applications in as little as 6 weeks on Foundry; Sarcos (NASDAQ:STRC) is integrating 0.5 trillion data points per month to accelerate design, maintenance and commercialization of their iron man suits. Lilium (NASDAQ:LILM) is flying through ground and flight testing using the vast data generated by every sensor streaming from the aircraft.”

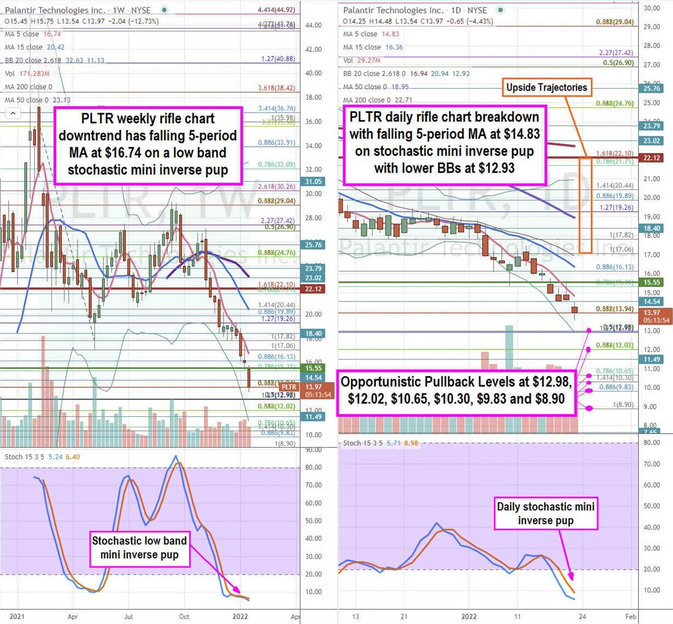

PLTR Opportunistic Pullback Levels

Using the rifle charts on the weekly and daily time frames provide a precision view of the landscape for PLTR stock. The weekly rifle chart has a nasty downtrend that triggered on the market structure high (MSH) sell trigger breakdown under the $22.10 Fibonacci (fib) level. The weekly 5-period moving average (MA) resistance is falling at $16.74 followed by the 15-period MA at $20.42. The weekly stochastic is forming a low band mini inverse pup through the 5-band. The weekly lower Bollinger® Bands (BBs) sit at $11.13.

The daily rifle chart has an inverse pup breakdown with a falling 5-period MA resistance at $14.83 followed by the 15-period MA at $16.36. The daily stochastic is also forming a low band mini inverse pup under the 10-band. The daily lower BBs overlap with the $12.98 fib level. The daily market structure low (MSL) buy triggers on a breakout through $15.55.

Prudent investors can watch for opportunistic pullback levels at the $12.98 fib, $12.02 fib, $10.65 fib, $10.30 fib, $9.83 fib, and the $8.90 fib level. Upside trajectories range from the $17.06 fib up towards the daily 200-period MA at $22.71.

Original Post

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.