It Not All Bad News For Advanced Micro Devices Stock

MarketBeat.com | Nov 07, 2022 05:12AM ET

- AMD saw double digit sales growth across three of its four business segments

- Client segment fell due to slowdown in PC and notebook sales as normalization kicks in

- Gaming segment revenues rose thanks to robust demand for next-gen consoles PlayStation 5 and Microsoft Xboxes

- Data Center segment revenues roseand Embedded segment grew due to the Xilinx acquisition

- AMD shares are trading at 17.7X forward earnings cheaper than NVDA at 42X forward earnings

Semiconductor company Advanced Micro Devices (NASDAQ:AMD) stock is down (-52.5%) on the year underperforming both the Nasdaq Composite down (-36%) and the VanEck Semiconductor ETF (NASDAQ:SMH) down (-39%) for the year. Investors fear that rising interest rates, global recession, a strong U.S. dollar, high inflation, and waning consumer discretionary spending are headwinds that continue to erode AMD’s business.

While its latest earnings report missed analyst estimates as it shows declining growth, the Company continues to make profits and sustain double-digit growth rates. It begs the question that if analyst expectations were lower, would the narrative be more positive? Has AMD’s earlier success placed expectations too high?

Valuations have fallen dramatically as shares now trade at just 17.7X forward earnings compared to GPU competitor NVIDIA (NASDAQ:NVDA) trading at 42X forward earnings. AMD reset the narrative by lowering its Q4 2022 top-line guidance and shares have been rallying as a result.

Next-Gen Video Game Consoles Drives Gaming Growth

While NVIDIA warned about the abrupt slowdown in its video gaming business as evidenced by the (-33%) drop in YoY segment revenues in its Q2 2022, it’s worth noting that AMD saw 14% YoY growth. AMD has literally cornered the market for console gaming, which is more mainstream than desktop PC gaming. AMD supplies the chips for the most popular next-gen video gaming consoles.

These revenues are posted under the “Semi-Custom” segment which includes next-gen consoles like the Sony (NYSE:SONY) PlayStation 5, which has sold over 25 million units and still nearly impossible to find one on the open market, the Valve Steam Deck, and the Microsoft (NASDAQ:MSFT) Xboxes.

It doesn’t supply chips for the Nintendo (OTC:NTDOY) Switch or Meta Platforms (NASDAQ:META) Oculus VR Headset, but there’s always the potential. While its GPU video card revenues fell like NVIDA, its “Semi-Custom” segment powered by next-gen video game console sales was able to offset the shortfall to drive up AMD's Gaming segment revenues by 14% YoY.

Not So Bad, Right?

On Nov. 1, 2022, AMD released its fiscal third-quarter 2022 results for September 2022. The Company reported an earnings-per-share (EPS) profit of $0.67 excluding non-recurring items versus consensus analyst estimates for a profit of $0.70, a (-$0.03) miss. Revenues grew 29% year-over-year (YoY) to $5.57 billion, beating analyst estimates for $5.65 billion.

Non-GAAP operating margins were 50%. The Data Center segment revenues rose 45% YoY to $1.6 billion driver by robust sales of its EPYC server processors. The Client segment fell (-40%) YoY from reduced processor ships stemming from a weak PC market. Gaming segment revenues climbed 14% YoY to $1.6 billion thanks to higher semi-custom product sales which offset the lower graphics revenues.

Embedded Segment revenues rose 1,549% to $1.3 billion YoY because they included Xilinx (NASDAQ:XLNX) embedded product revenues. AMD CEO Lisa Su commented on the conference call, “In summary, we are well-positioned to navigate the current market dynamics based on our leadership product portfolio, strong balance sheet and growth in our Data Center and Embedded segments.

We have three clear priorities guiding us. First and foremost, we are focused on executing our road maps and delivering our next generation of leadership products. Second, we are building even deeper relationships with our customers as we make AMD a fundamental enabler of their success. And lastly, we remain very disciplined in how we manage the business.”

Controlling the Narrative and Lowering the Bar

The Company lowered its Q4 2022 revenue guidance to grow 14% YoY coming in between $5.20 billion to $5.80 billion and falling short of the $5.94 billion consensus analyst estimates. The Company expects YoY and sequential growth for its Embedded and Data Center business and non-GAAP operating margins of 51%.

Full-year 2022 revenues are expected to grow around 43% to $23.2 billion to $23.8 billion and non-GAAP gross margins around 52%. Except Client aka desktop and notebook PC sales experiencing normalization after the pandemic spawned demand shock, AMD is delivering double-digit growth across the rest of its segments including Data Center, Gaming, and Embedded.

It continues to beat out Intel (NASDAQ:INTC) by keeping prices low thanks to its asset-light strategy of outsourcing their chips to Taiwan Semiconductor Manufacturing (NYSE:TSM). Sony has also announced it will be bulking up shipments of its hard-to-find PlayStation 5 for the upcoming holiday shopping season and rumors of a PlayStation 5 Pro launch in 2023.

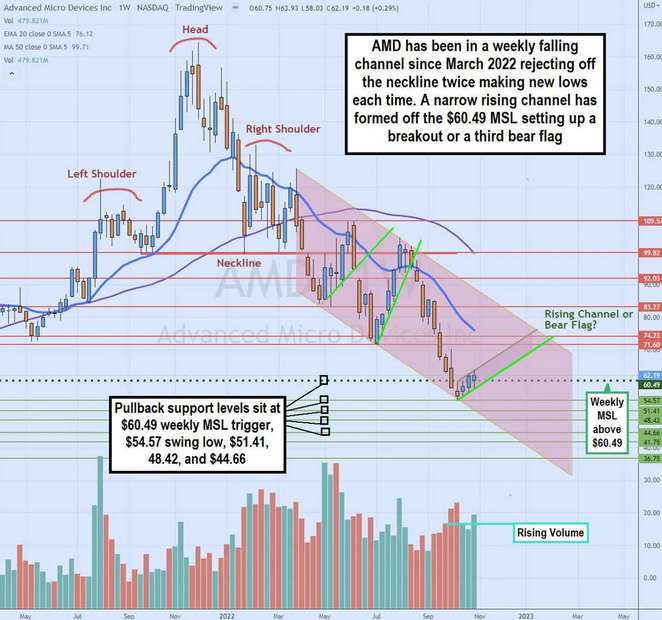

Breakout or Bear Flag on the Menu?

The AMD weekly chart illustrates its falling downtrend channel that commenced from March of 2022 after the head and shoulders (HS) breakdown through its $99.82 neckline. AMD was able to bounce through the neckline on two occasions only to peak at the top of the falling channel trendline and collapse right back under to make new lows.

The weekly 20-period exponential moving average (EMA) resistance continues to fall at $76.12 followed by the weekly 50-period MA overlapping the neckline near $99.82. Shares bottomed out at $54.57 to form a weekly market structure low (MSL) trigger above $60.49. The trigger was activated on Oct. 24 as a narrow rising channel formed heading into the Q3 2022 earnings report on Nov. 1.

While the earnings report missed analyst estimates, its initial gap down was absorbed as buyers pushed shares right back up into the rising channel as volume picked up. The question now is if the narrow rising channel, within in the larger falling channel will continue to rise until a breakout can occur above $75 or a third bear flag forms on a rug pull dropping shares back below the lower trendline of the narrow rising channel and proceed to new swing lows is $54.57 breaks down.

Original Post

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.