Infinite Fed Easing, Finite Market Bounce

Ivan Delgado | Mar 24, 2020 04:53AM ET

No matter how big the guns the Fed pulls out QE infinity this time - the market is still in a state of 'glass half empty' when it comes to buying into the old mantra of 'the Fed Put', which gained widespread popularity on the belief that the Fed can always rescue the economy and equities. The market told us on Monday, again, that these paradigms are shifting...

Quick Take

The Fed has gone all in with QE infinity and yet stocks, despite a short-term spell of strength, are largely unfazed, with the S&P 500 closing down near the 3% mark. In a world where demand and supply have been decimated amid the fastest descent into a bear market in history, week after week, we have further evidence that the Fed’s old tricks are no longer working. Still, they are necessary to provide a backstop in the avalanche of bankruptcies that would eventuate otherwise in a global economy that is imploding for desperate measures. It’s precisely this state of despair that is forcing Germany to break its own long-held rules of a balanced budget by signing off a €750 billion economic package to combat the virus fallout, the US soon to approve the release of $2 trillion in fiscal stimulus, RBA/RBNZ testing the waters of QE, etc.

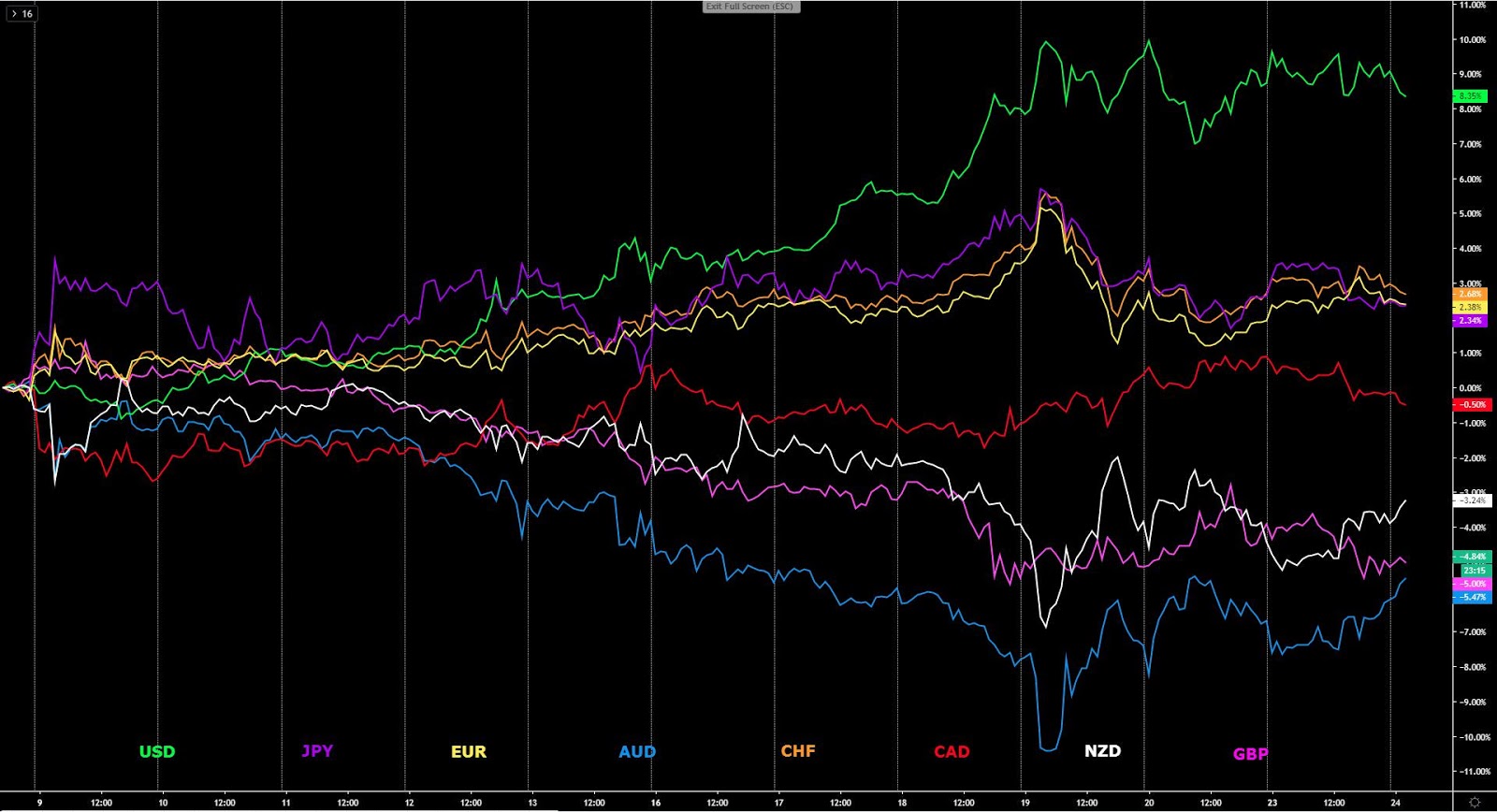

The last country to cave in and go into lockdown is the UK, which only reinforces the notion that since the countries where the main financial centers exist (NY, London) are just getting started to toughen the rules, we should be expecting worsening virus stats before they turn the corner. In the currency market, even if QE infinity has done little to lift the equity valuations, the US Dollar has seen a temporary pause in its macro bull phase after recently breaking into all-time highs at an index level. The Oceanic currencies benefited from the Fed announcement, as did the Euro and the Swiss Franc. The worst performers included the GBP, CAD, and JPY.

Narratives In Financial Markets

* The Information is gathered after scanning top publications including the FT, WSJ, Reuters, Bloomberg, ForexLive, Twitter, Institutional Bank Research reports. pass soon as millions of lives are at stake. The delay in the bill is adding sell-side pressure in equities. The Financial Times notes that “the negotiations hit an impasse after Democrats on Capitol Hill said that the proposed deal offered big business an overly generous bailout with limited conditions and scant oversight. They also argued it would not release enough new funds to hospitals.”

Equities shrug off Fed QE-infinity: The latest measures by the Fed proved to be a short-lived stimulant for equities, and after a brief run higher, most of the QE unlimited-induced gains were given back, with gold the major beneficiary of a world that is about to be flooded with further USDs. Government bonds were bought in a follow-through move after the ferocious demand from last Friday.

USD strength caps risk markets: In the USD domain, the action by the Fed was largely ignored. It’s looking increasingly likely that for risk markets to go on a sustainable jubilee run, a weaker USD and tighter corporate credit spreads is a combination that must materialize. Traders should not rule out, should the bullish run continue into fresh record highs, that the Fed will step in, coordinated with other Central Banks, to intervene in the currency, even if there are not yet any early noises or suggestions by politicians that this is imminent. The NY Fed put out a paper explaining in detail the circumstances and guidelines to act in the exchange rate.

COVID-19 makes Fed Put obsolete: The fact that equities in the US succumbed to the historical measures by the Fed is a reminder that the market is unwilling to justify clinging on to the old mantra that the endless liquidity by a Fed Put will always work. This old paradigm has shifted as the market appears to still be excessively anxious about the complete destruction of wealth in a world that is rapidly descending into a new phase. This includes very limited economic activity for a protracted period of time, which leads to companies’ revenue projections decimated, corporate debt defaults, major scale bailouts around the world, and essentially a reset of global economies.

Trump doubles down on line drawn at some point: US President Trump said “we cannot let the cure be worse than the problem itself”, in reference to coronavirus containment measures. His tweet read: “We cannot let the cure be worse than the problem itself. At the end of the 15 day period, we will make a decision as to which way we want to go!" The administration appears to be weighing all possibilities, realizing that the measures to put off endless fires via a tsunami of liquidity runs counterproductive to the ballooning economic costs, which may lead to even more lives taken should a depression settle in. Trump has started to imply a choice they will face is to be willing to go into lockdown for a long time or go back to relative normality and minimize deaths.

Germany signs off huge fiscal stimulus package: In Europe, Germany is finally recognizing that it must abandon the old stance of a balanced budget to instead go all-in with a very generous fiscal and monetary support program to stem the economic blow that COVID-19 is inflicting not only home but across Europe, especially in the countries most punished such as Italy or Spain. The German government, therefore, agreed earlier today to a €750 billion economic package to combat the virus fallout.

‘Flash’ PMIs to paint a new reality: Coming up today, ‘Flash’ Markit PMIs from Germany, the wide European Union, France, UK and the US will provide the first real taste of the magnitude at which these sectors are sinking. Projections are pointing at around 40 in Germany from 48 the previous month, the Eurozone at 41 from 49 last month, a slide to 49 from 51.7 in the UK and 45 from 50.7 in the US. While the data may be shockingly low, the market continues to trade on pure sentiment and I doubt these numbers will be a primary driver to set the market mood. The risk is that it will just feed the negative narrative around COVID-19 as the new reality sinks in.

MAS hints at further easing sooner rather than later: The Singaporean Central Bank has announced that it will bring forward its monetary policy statement to March 30th. The market’s reaction was to weaken the SGD as it interprets that such a move implies they are looking to take earlier measures to deal with the economic crisis. As the Strait Times notes, “economists expect the MAS to ease monetary policy significantly as recession risks rise owing to the impact of the coronavirus pandemic on the economy.”

UK latest to enforce lockdown: The fluid COVID-19 situation has finally led UK PM Johnson to cave in by announcing that “everyone in the U.K. must stay at home. Residents can only leave home to shop for basic necessities, for one form of exercise per day, for medical needs, and to travel to and from work when necessary, according to ABC, a site that live blogging the latest. On a more positive note, even if that may sound quite a stretch given the context, the new virus cases in Italy, while rising by nearly 5,000, is the first time that in percentage terms it has gone below 10%.

Insights Into Forex Flows

The weekly aggregation of forex flows reveals some great insights on the potential directional biases each G8 currency may follow in weeks to come. The technical observation when stepping back and staring at these macro outlook tells me that the USD run is just ⅓ mature in the full scale of its potential magnitude. It also suggests the EUR faces some major stumbling block overhead backed up by 10 years worth of price action data. The Pound remains a fragile currency as drawing parallels with GFC tells us more weakness should be expected. However, no currency offers more technical value than short CAD. On the complete opposite side of the spectrum is the Yen, with the aggregation of flows finally providing sufficient validation to make me think that the next cyclical bull run is now underway (15%+ potential). The AUD has rebounded from its most relevant support in a decade, so those following my daily deconstruction of flows won’t be too surprised to see AUD appreciation. The NZD has transitioned into a cyclical bear trend with a very ambitious downside target from current levels. Lastly, the CHF is looking like it may soon validate a huge technical breakout.

Let’s now get started with a look at every index…

- The EUR index weekly chart pulled back from its decade-long resistance - 50% retrac from the post GFC sell-off -. This level is huge and EUR shorts were initiated from here.

- Volatility in the Euro remains exceptionally high, and based on the last GFC, it suggests that we are set for a protracted bumpy ride of high vol in months to come as COVID-19 plays out.

- Only a weekly close of the EUR index above the red rectangle (50% decade-long resistance) would suggest the EUR is heading into a more macro cyclical change in dynamics.

- It is on this black swan event that this technical milestone may occur, but we are still far from it, and with conditions overstretched, a deeper pullback is my base case.

- The GBP weekly chart does not bode well for the currency, as technicals are pointing towards further room to fall based to the historic low.

- If the GBP weakness accelerates further from there, a final bearish projection target would result in an additional 8-10% downside potential in the currency.

- This bear rally resumption would, therefore, complete a 20% move from peak to trough, which would be matching in percentage terms the collapse seen in the last GFC of 2008.

- GBP tends to underperform G8 FX indices in a global crisis, but caution is warranted that we only make it to the first support as GBP selling originates from much lower than pre-GFC.

- Fundamentally, the aggressive actions by the BOE alongside the mandatory lockdown of Britain announced by UK PM Johnson anchors the bearish sentiment in the currency.

- We are still in the early stages of a new cyclical USD bull run, with the currency having appreciated strongly but only ⅓ of the expected upside movement.

- The fact that the Fed has gone all in with QE infinity yet the USD still trades near record highs is the ultimate clue that the outlook for the currency is unambiguously bullish.

- I will reiterate that at this point, the only effective way to ‘impose’ weakness in the USD is via coordinated, mass intervention in the USD by the Fed.

- Even if intervention were to occur, history has taught us that while it may lead to a temporary reversal in the currency, it’s hard to fight the market (BOJ, SNB as examples).

- The levels of vol the currency hit last week surpassed the peaks in vol during the GFC, validating a ‘liquidity event’ but may warrant ‘excuse’ to intervene down the road if vol prevails.

- The world has greater needs to get USDs as USD-denominated debt has doubled since the last GFC, implying that the scramble to get hold of USD to serve debt is here to stay.

- The CAD index has seen an acceleration in the building of short inventory off a very attractive level in the form of its range mid-point.

- CAD is my preferred short on the basis that the Canadian economy will go through a double-whammy of services/energy plunge alongside further room to ease by the BOC.

- The existing range parameters have been at play for the last 4 years but with the perfect bearish storm hitting the currency, I can’t help but to see big technical value here.

- If an eventual bearish resolution of the long-held range occurs, it paves the way for an additional 8% fall this year. This is the time to exploit this discounted value.

- The JPY index finally broke and closed above its weekly price structure, suggesting a major technical milestone that implies the next bull phase is underway.

- The next bull projection target is found over 15% higher, which means that some great opportunities to engage in JPY longs in the ng weeks may arise.

- In the worst case that the JPY only appreciates half in magnitude relative to the moves seen in the GFC (this crisis in many ways is worse), the final target I point at would still be met.

- The target selected (around 15% higher) that may mark a potential top in the JPY aligns perfectly with the highest JPY valuations in 2008 + 100% projected target.

- The AUD, after reaching a massive level of support dating back to the last GFC (all-time low as far as the chart goes + 100% bear projection), has found aggressive buyers.

- Since the level of support reached was such a major confluence as it includes the 100% projected target from the last decade’s + support line, I can envision a short-term recovery.

- If the bounce proves to be a ‘dead-cat’ type with its shallowness leading to further sell-side pressure, I’ve come up with scenario #2 as an alternative playbook.

- If the bear rally extends this year, the Aussie would be exposed to severe losses until the next 100% bear projection target is met (see projection target below).

- The NZD index confirmed last week a breakout of a decade-long structure, which sets the ball for a new cyclical bearish trend in the NZD this year.

- This breakout of structure validates an ultimate target 18% lower from the breakout point, which makes the prospects to short the currency on strength this year my base case.

- If the NZD bearish playbook materializes during the months to come (in 2020), the low that would be put in comes in stark alignment with the bottom found during the GFC in 2008.

- The CHF weekly chart is yet to validate the acceptance of the currency above its last all-time high, therefore, one must horse its horses to expect the bull cyclical phase as confirmed.

- Stepping back, the index recently broke through its previous GFC/record-high, and upon a weekly close above, it allows us to draw a new bull projected target.

- Should this new bull run eventuate, the magic of market symmetries tells me that the run towards the ultimate target is 12% above the breakout point.

- As in the case of the JPY, the vol realized so far in CHF has been tepid relative to the GFC, therefore, I wouldn’t be surprised that we see a pick up in vol moving forwa

Important Footnotes

- Market structure: Markets evolve in cycles followed by a period of distribution and/or accumulation.

- Horizontal Support/Resistance: Unlike levels of dynamic support or resistance or more subjective measurements such as Fibonacci retracements, pivot points, trendlines, or other forms of reactive areas, the horizontal lines of support and resistance are universal concepts used by the majority of market participants. It, therefore, makes the areas the most widely followed and relevant to monitor.

- Fundamentals: It’s important to highlight that the daily market outlook provided in this report is subject to the impact of the fundamental news. Any unexpected news may cause the price to behave erratically in the short term.

- Projection Targets: The usefulness of the 100% projection resides in the symmetry and harmonic relationships of market cycles. By drawing a 100% projection, you can anticipate the area in the chart where some type of pause and potential reversals in price is likely to occur, due to 1. The side in control of the cycle takes profits 2. Counter-trend positions are added by contrarian players 3. These are price points where limit orders are set by market-makers.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.