How Resource Limits Lead To Financial Collapse

Gail Tverberg | Mar 31, 2013 03:04AM ET

Resource limits are invisible, so most people don’t realize that we could possibility be approaching them. In fact, my analysis indicates resource limits are really financial limits, and in fact, we seem to be approaching those limits right now.

Many analysts discussing resource limits are talking about a very different concern than I am talking about. Many from the “peak oil” community say that what we should worry about is a decline in world oil supply. In my view, the danger is quite different: The real danger is financial collapse, coming much earlier than a decline in oil supply. This collapse is related to high oil price, and also to higher costs for other resources as we approach limits (for example, desalination of water where water supply is a problem, and higher natural gas prices in much of the world).

The financial collapse is related to Energy Return on Energy Invested (EROEI) that is already too low. I don’t see any particular EROEI target as being a threshold–the calculations for individual energy sources are not on a system-wide basis, so are not always helpful. The issue is not precisely low EROEI. Instead, the issue is the loss of cheapfossil fuel energy to subsidize the rest of society.

If an energy source, such as oil back when the cost was $20 or $30 barrel, can produce a large amount of energy in the form it is needed with low inputs, it is likely to be a very profitable endeavor. Governments can tax it heavily (with severance taxes, royalties, rental for drilling rights, and other fees that are not necessarily called taxes). In many oil exporting countries, these oil-based revenues provide a large share of government revenues. The availability of cheap energy also allows inexpensive roads, bridges, pipelines, and schools to be built.

As we move to energy that requires more expensive inputs for extraction (such as the current $90+ barrel oil), these benefits are lost. The cost of roads, bridges, and pipelines escalates. It is this loss of a subsidy from cheap fossil fuels that is significant part of what moves us toward financial collapse.

Renewable energy generally does not solve this problem. In fact, it can exacerbate the problem, because the cost of its inputs tend to be high and very “front-ended,” leading to a need for subsidies. What is really needed is a way to replace lost tax revenue, and a way to bring down the high cost of new bridges and roads–that is a way to get back to the cost structure we had when oil (and other fossil fuels) could be extracted cheaply.

The Way Resource Extraction Reaches Financial Limits

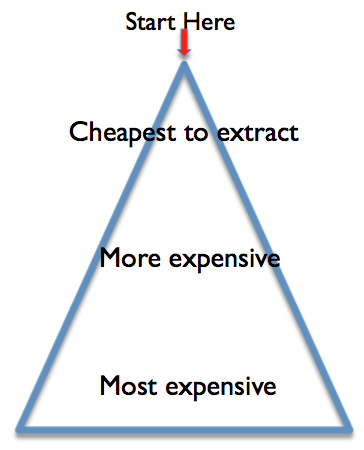

When a company decides to extract a resource such as oil, gold, or fresh water, it looks for the least expensive source available. After many years of extraction, the least expensive sources become depleted, and the company must move on to more expensive resources. It always looks like there are plenty of resources left; they are just increasingly expensive to extract. Eventually an extraction limit is reached; this limit is a price limit.

As easy to extract resources become more depleted, it becomes necessary to invest more resources of every type in extraction (for example, manpower, oil, natural gas, fresh water), in order to extract a similar amount of the resource. I have called this the Investment Sinkhole problem.

The need to use greater resources in the process of resource extraction leaves fewer resources available for other purposes. Prices adjust to reflect this out of balance. If there is no substitute available for the resource that is reaching limits, the economy adjusts by contracting to match the amount of resource that is available at an affordable price. Some economists might call the situation “reduced demand at high price”. What the situation looks like, in terms most of us are used to using, is recession or depression.

Part of the confusion is that many people completely miss the fact that there is a close connection between cheap energy supply of the exact type needed (for example, gasoline for cars, diesel for trucks, electricity for many factory applications) and the ability of the world economy to make goods and services.

If the price of energy of the type a particular manufacturer or service provider uses increases (say gasoline or diesel or natural gas or electricity), that manufacturer or service provider in the short term has no choice but to pay the increased price, because there is no substitute for energy of the right type. If the manufacturer or service provider tries to pass these higher costs on to its customers, there is likely to be a cutback in demand, leading to a need for layoffs. Alternatively, with longer lead time, the company may be able to find a way around the problem of increased costs, by using more automation, or by outsourcing production to a country where costs are cheaper. Any of these responses leads to reduced US employment and recessionary impacts.

What History Says about Prior Collapses

Until fossil fuels came into widespread use, civilizations regularly grew until they reached limits of some sort, and then collapsed. There are many books looking at this issue. David Montgomery, in Investors pile into housing, this time as landlords .” Of course, when something goes wrong (like mis-estimating returns, or oil prices rising higher, leading to more pressure on renters’ ability to pay), the same investors are likely to pile right back out, puncturing the new bubble. Commercial investors rushing out will pull down property values, leading to yet more mortgage defaults as homeowners again find their loans “underwater”.

A fourth possibility is that oil prices will ratchet upward again. Alternatively, natural gas may rise from its current artificially low price level in the US, to more like European or Japanese levels. Either of these would lead to more financial pressures on citizens, and more debt defaults. Banks would likely again be in difficulty, needing bail outs.

A fifth possibility is that the Euro ceases to be a currency. Alternatively, some of the debtor nations could drop out of the Euro, allowing the Euro to rise for remaining nations, thus putting the remaining nations in a worse position for selling their exports. In either of these scenarios, the European crisis could be exported to the US, partly as reduced demand for our goods, and partly through exposure of banks to European defaults.

A sixth possibility is the effects of ObamaCare will destabilize an already weak economy, as businesses attempt to circumvent its effects by substituting more part-time workers for full-time workers.

A seventh possibility is that pensions start running into real financial difficulty, because of artificially low interest rates. The US government may be called in to bail out pension funds, or the Pension Benefit Guaranty Corporation, at high cost.

An eighth possibility is that states start leaving the United States, because they feel that they would be better off on their own, as taxes and mandatory programs (such as ObamaCare) become increasingly difficult to deal with.

What does the shape of the decline look like?

Many people who base their views on geological depletion of oil expect that the decline will be somewhat slow, matching geological decline. I don’t think geological decline rates will have much to do with the shape of the decline, except for perhaps setting an upper bound as to how well things might, in theory, work out.

The big question in my mind is how well the international financial system will hold together. There is a close corollary question: How successful will be at replacing it on a timely basis if it does fall apart? My concern is that if banks are suddenly closed, businesses of all types will fail. This could include companies extracting oil as well as companies selling electric power and companies providing fresh water.

If there are long-term problems with the financial system, international trade is likely to be greatly reduced. Businesses making trades are likely to want greater assurances that they will actually be paid than is the case today. This could take the form of bilateral trade with trusted partners, or “I’ll ship you Product A if you will ship me Product B,” as a form of barter.

A slowdown in world trade could have dramatic repercussions quickly with respect to our ability to keep basic services in good repair, because we are now dependent on international trade for replacement parts of products we use every day (such as cars and trucks). Nearly everything that is manufactured today incorporates raw materials from around the world, and uses machines that depend on parts from around the world.

Another question is whether there will be huge political disruptions. If banks are closed, someone usually is blamed. We have seen many ways these political disruptions can take place. Some examples might include Syria, Egypt, the Former Soviet Union, and Greece.

One scenario I can imagine is that some parts of a country are subject to more disruption than others. In one part of the country, banks may be closed, while in another part, states may be able to reopen closed banks. Or electricity outages may occur following a storm, and never be repaired, while other locations nearby are doing fairly well. There may be political riots, but these are often located in areas where politicians are located, not in other areas.

Perhaps it is just as well that we don’t know exactly what the decline will look like. Not knowing gives us some chance for optimism.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.