Hedge Fund Analyst Makes Bearish Call On Oracle’s Earnings Report

Estimize | Sep 18, 2013 02:01AM ET

Oracle (ORCL ) is expected to report FQ1 2014 earnings on September 18th after the close. The information below is derived from data submitted to the Estimize platform by a set of Buy Side and Independent analyst contributors.

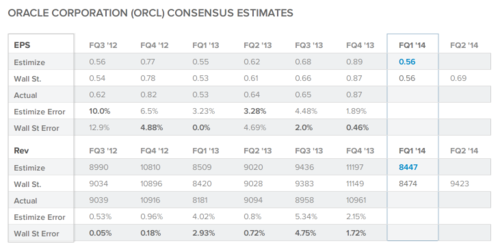

The current Wall Street consensus expectation is for Oracle Corporation (ORCL), to report 56c EPS and $8.475B Revenue while the current Estimize consensus from 14 Buy Side and Independent contributing analysts is 56c EPS and $8.448B Revenue. The magnitude of the difference between the Wall Street and Estimize consensus numbers often identifies opportunities to take advantage of expectations that may not have been priced into the market.

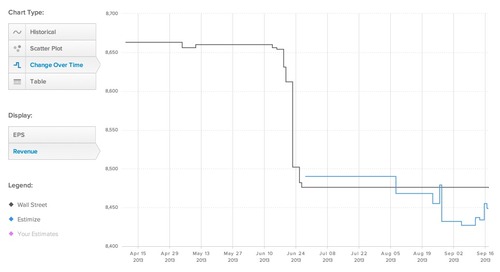

Over the past 4 months the Wall Street consensus trend for EPS has been negative, moving from 58c to 56c while the the Wall Street consensus trend for Revenue has been negative moving from $8.660B to $8.475B. There have not been any recent revisions from Wall Street, but the Estimize revenue consensus has dipped significantly towards the end of the quarter. The directionality of revisions at the end of the quarter is often a good predictor of beats and misses.

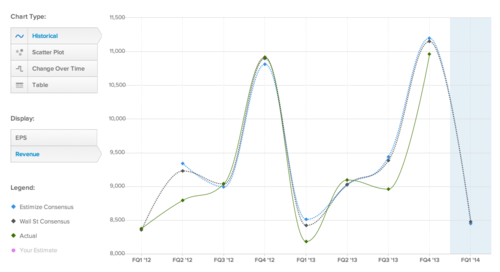

Over the previous 8 quarters, ORCL has beaten the Wall Street consensus for EPS 4 times while missing the Wall Street Revenue consensus 4 times. Over the same time period ORCL has missed the Estimize consensus for EPS 5 times while missing the Estimize Revenue consensus 3 times. Disappointing reports the last two quarters have significantly impacted ORCL post earnings as the stock has seen significant selling each time.

The distribution of estimates published by analysts on Estimize range from 62c to 54c EPS and $8.150B to $8.750B Revenues. The range of estimates for both EPS and Revenue this quarter is larger than it has been during the past two earnings releases signaling that there is wide disagreement amongst analysts. The size of the distribution of estimates relative to previous quarters often signals whether or not the market is confident that it has priced in the expected earnings already. A wider distribution signals the potential for greater volatility post earnings, a smaller vice versa.

The analyst with the highest estimate confidence rating this quarter is hedge fund analyst JC215 who projects 56c EPS and $8.425B Revenue.

Given ORCL’s recent history of disappointing earnings results, the trend in the Estimize Revenue Consensus, and a bearish estimate by one of the most accurate hedge fund analysts on the platform, ORCL may be in for a tough report. As well, given the size of the distribution, the stock should see significant volatility post earnings.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.