Forget Fed Action, Markets Explaining Inflationary Fear

Satendra Singh | Jul 19, 2021 09:54PM ET

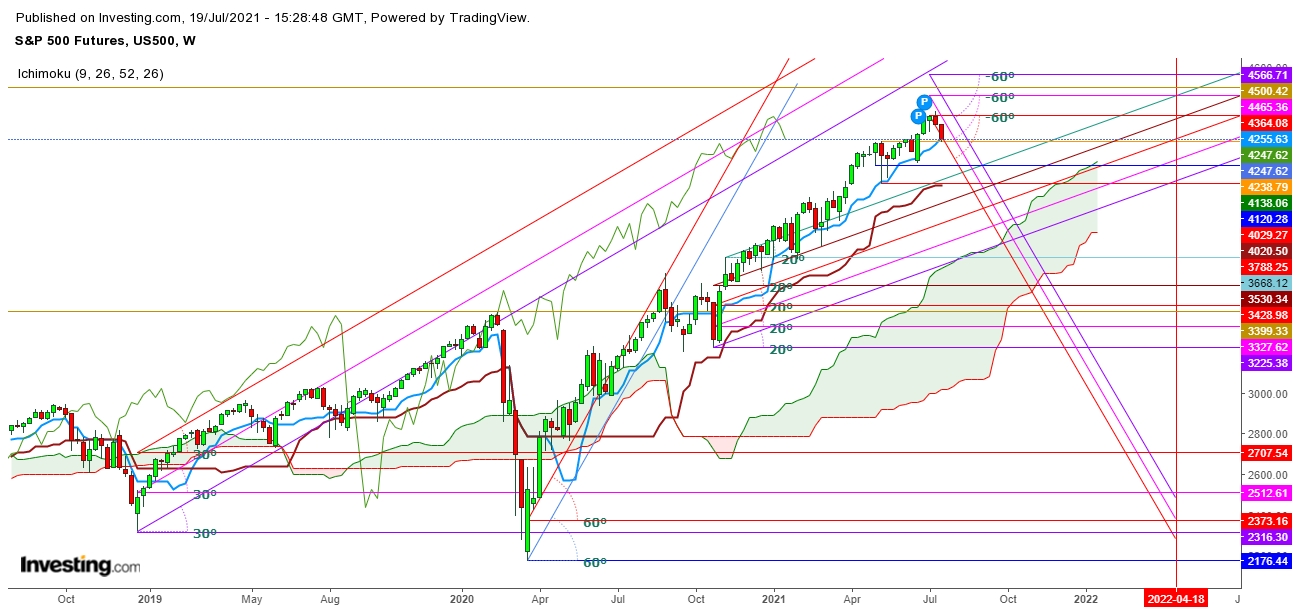

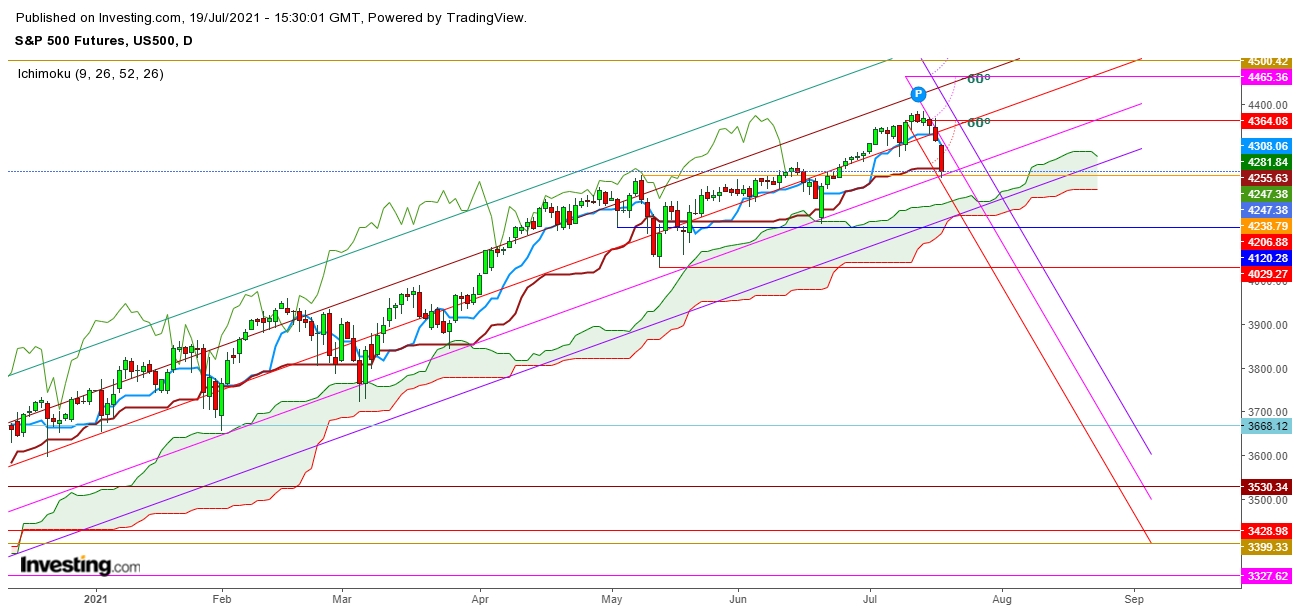

Undoubtedly, the S&P 500 Futures had signaled an advent of a steep fall on July 16, 2021 that was accompanied by a sharp surge in the S&P Volatility Index.

On Monday, this first signal was confirmed by a steep fall in US equity markets. At 4:30 pm (GMT), the Dow was trading 781 points lower, the S&P 500 had lost more than 78 points and NASDAQ was below 165 points. This type of steep fall could create big jolts in global markets, until the Fed’s next meeting on July 28, 2021. Undoubtedly, based on the reactionary moves of the US equity indices, we hardly need to wait for the Fed’s next meeting.

Globally, Central Banks are having difficulty adjusting their monetary policies amid the sudden surge in the COVID-19 cases, particularly at when most countries were planning to push forward reopening, following completion of vaccinations. But the abrupt upswing in COVID-19 cases has left the hopes of earlier re-openings on hold.

The current steep fall of US equity indices seems to be the impact of ill-tempered exchanges between the Biden administration and social media giants, which illustrated the mounting concern in Washington about the spread of the Delta variant of COVID-19, which is more than twice as contagious as earlier strains of the virus.

Infection rates are rising particularly strongly in the South and Midwest, where skepticism toward vaccines—and to most policies advanced by the Democratic administration—is highest.

The Federal Reserve seems to follow the conventional methods to tackle growing inflation by keeping interest rates below zero or even in the negative territory. In short, this indicates that Fed Chair Jerome Powell’s insistence that inflation is transitory is becoming less defensible. Even if these high readings abate as the base effect of depressing prices a year ago fades, to call a mismatch between supply and demand that could last many months transitory begs the question.

Central bank policymakers in other countries are less hesitant. The Bank of Canada cut its bond purchases by C$1 billion a week in April, to C$3 billion (USD$2.4 billion), and last week said it will cut a further C$1 billion (USD$784 million) a week.

Finally, global equity markets could hardly wait for the Fed's next meeting on July 28, which is expected to hardly come with a decisive move to control inflation. And, with the absence of a solid monetary policy, big bears could be attracted to remain in control of global equity markets.

Disclaimer:

1. This content is for information and educational purposes only and should not be considered as investment advice or an investment recommendation. Past performance is not an indication of future results. All trading carries risk. Only risk capital should be involved which you are prepared to lose.

2. Remember, YOU push the buy button and the sell button. Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from an investment and/or tax professional before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.