Fixed Income At A Glance

Legal & General Investment Management | Jun 24, 2022 07:59AM ET

Key points from June’s credit strategy meeting

- Tighter financial conditions led us to lower our short-term for the US, UK and global market to -1. We remain slightly positive at +1 in Europe as valuations appear attractive and we see the economic backdrop as more positive.

- Our long-term scores for the US and Europe are -1 due to geopolitical pressure and our negative outlook on corporate strength. In contrast, we have increased our score for the UK to neutral as its corporate strength appears more solid.

- We increased our score on High Yield to +1 due to moderating inflation fears and our core view that there will be no material default cycle due to solid economic fundamentals.

- The EM team maintained their short-term score of +1 in the face of the significant value now offered by their market on an all-in yield basis.

Market summary

- May saw falling equity and bond markets on growing fears of a US recession and signs of slowing economic activity in other developed markets.

- Inflation remains a significant drag on the US and eurozone. Yields on US Treasuries fell and the curve steepened, while European government bond yields pushed higher but led to a flatter curve as investors priced in a more aggressive rate hiking cycle.

- Spreads widened across most major credit markets. Emerging markets saw a mixed picture, with oil-exporting countries outperforming. The Turkish lira traded cheaper thanks to an unconventional approach to combatting inflation. The Russian rouble continues to outperform due to tight domestic monetary conditions.

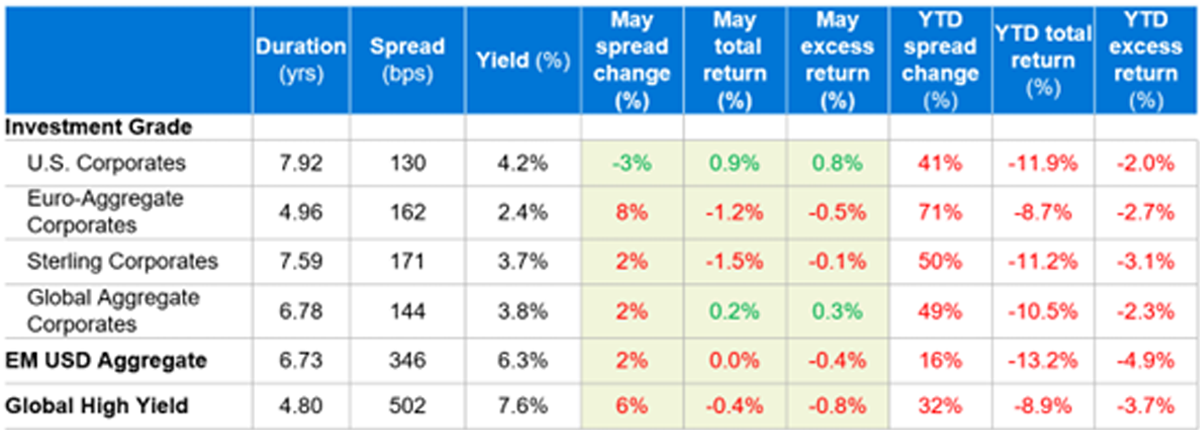

Key market moves: May and YTD

Source: Bloomberg Barclays, as of 31 May 2022. Past performance is not a guide to the future. Data: Bloomberg Barclays (LON:BARC) index returns are USD Hedged for Global indices, and in local currency for the others.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.