Fed Jawbones Mean Business

Gary Tanashian | Feb 10, 2022 05:29PM ET

The stern message is that the Fed Funds rate could be raised at any time (which is possible even before the next FOMC meeting on March 16, in my opinion).

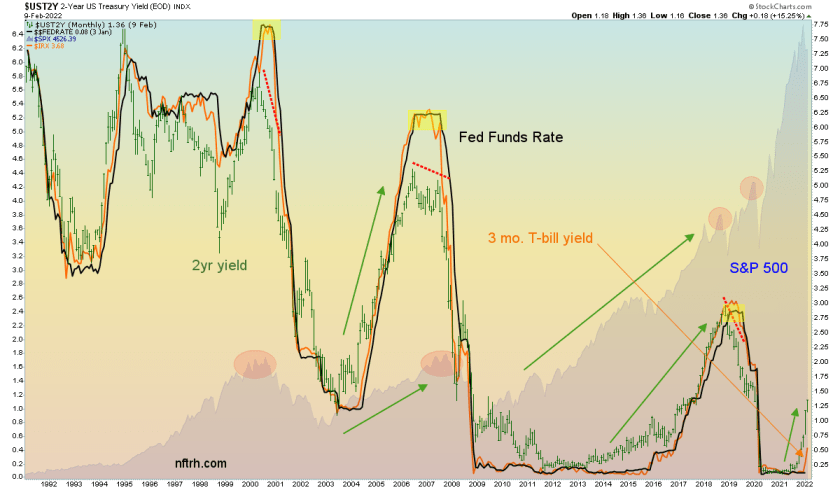

I would not advise you to listen to those who think they know what the Fed is thinking and insist that the Fed will not dare raise the Funds rate. They will dare and do it, barring any significant short-term changes to the current macro. In my experience, the Fed has done what the bond market tells it to do, almost without exception. Ben Bernanke held ZIRP for a deplorably long time, but that was because the T bill on the chart below allowed him to.

I’ve added the 3-Month Treasury bill yield (IRX, orange) to this chart, and you will notice that this short-term yield and the Fed Funds rate go pretty much in lockstep. When IRX finally rose in 2015, Bernanke’s successor, Janet Yellen, promptly got in gear out of the seven-year perma-ZIRP phase.

Take a look at the lower right corner of the chart. In that gap between the orange line and the black line, the Fed is exposed as behind the curve regarding inflation. So sure, all these about backward-looking inflation do represent the vast mountain of inflationary layers the Fed laid in 2020, and it’s sitting there like a toxic pile of monetary sludge. Now the Fed would undertake the task of cleaning it up. And it is late getting on that task.

This chart has been used previously to show that it is historically well after the Fed begins a rate hike cycle that the stock market tops out. But in this case, I want to zoom in on the orange IRX and its historically tight relationship with the funds rate.

In its long-term yields and especially short-term yields (the 2-year, green, has been demanding action since late last summer), the bond market is demanding a rate hike now, and I don’t think the Fed will find it comfortable waiting until mid-March and the next FOMC meeting. Would-be pressure relief could come from one of two sources:

- An unexpected rate hike in the interim.

- A market liquidation to send the herds into the liquidity of short-term notes and bills - which would tamp down yields.

Of course, Thing 1 could be the trigger to Thing 2. So there’s that too. It’s a complicated set of circumstances. Don’t be caught making assumptions in this market, and also don’t be caught following gurus recycling dogma. If the Fed is caught this far off guard, anything is possible, and there’s no guru alive who’s got anything but guesses at hand.

Now, as to whether or not the Fed will be able to catch up to the curve in any reasonable time frame, that’s another question altogether. It looks daunting, and I think the Jawbones know it.

![]()

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.