Deep-Value ETF Report: Commodities/Energy Remain Out Of Favor

James Picerno | Jan 10, 2020 07:41AM ET

Ben Graham famously described Mr. Market’s psychological state from day to day as vulnerable to erratic swings of optimism and pessimism. But recent history shows that the crowd’s exhibited a mostly stable view on commodities and energy by consistently discounting these assets by relatively aggressive standards, based on a set of exchange-traded products. That was true in our last update (Aug. 22, 2019) and remains so today.

As outlined below, sentiment has been tepid at best when it comes to raw materials and the companies engaged in processing oil, gas and other basic commodities. There are a handful of notable exceptions – gold, for instance, has been trending up in recent years. But across the broad sweep of commodities and energy, investors have cooled to the idea that assets in this corner deserve relatively high valuations.

Before we get into the details, a quick refresher on the ranking system used below. The metric of choice for “deep value” in this column is the 5-year return, which is based on an idea outlined in a paper by AQR Capital Management’s Cliff Asness and two co-authors: “Value and Momentum Everywhere,” published in a 2013 issue of the Journal of Finance. There are many value metrics and so no one should confuse the 5-year-performance benchmark as the definitive measure of bargain-priced assets. But as a starting point on the journey of identifying where the market’s outlook has fallen sharply, the 5-year change is a practical measure.

One advantage of us a 5-year performance measure: It can be applied over a broad set of assets, thereby dispensing a level playing field for evaluating value. Another plus: this metric is simple and therefore immune to estimation risk, which can complicate accounting-based value gauges, such as price-to-book and price-to-earnings measures. In short, the 5-year return is a handy tool as a first approximation for identifying ETFs that may be deeply discounted by the crowd — and thereby offer (possibly) relatively high expected returns via the value proposition for investing.

The standard caveat applies, of course, namely: there are no guarantees that value, no matter the definition, will lead to superior performance anytime soon, if ever. Recent history certainly shows that to be true. All the more so when it comes to commodities, fossil-based energy investments in particular. As the world grapples with the risk of climate change, there are predictions that the glory days for oil companies and the like have passed. In other words, energy stocks are arguably deeply discounted for a reason and so investors should go in with eyes wide open.

The ranking below covers 135 exchange-traded products that run the gamut: US and foreign stocks, bonds, real estate, commodities and currencies. You can find the full list here, sorted in ascending order by annualized 5-year return — 1260 trading days — through yesterday’s close, Jan. 9, 2020.

Keep in mind that the list is quite granular. In equities, for instance, the ETFs range from broad regional definitions (Asia, Latin America, etc,) to country funds, down to US sectors (energy, financials, for instance) and industries (e.g., oil & gas equipment & services). The only limitation is what’s available for US exchange-listed funds. Note, too, that just one representative ETF for each market niche is selected, albeit subjectively. For instance, there’s only one fund on the list for US real estate investment trusts. Otherwise, the search is broad and deep, or as broad and deep as allowed given the current availability of US-listed ETFs.

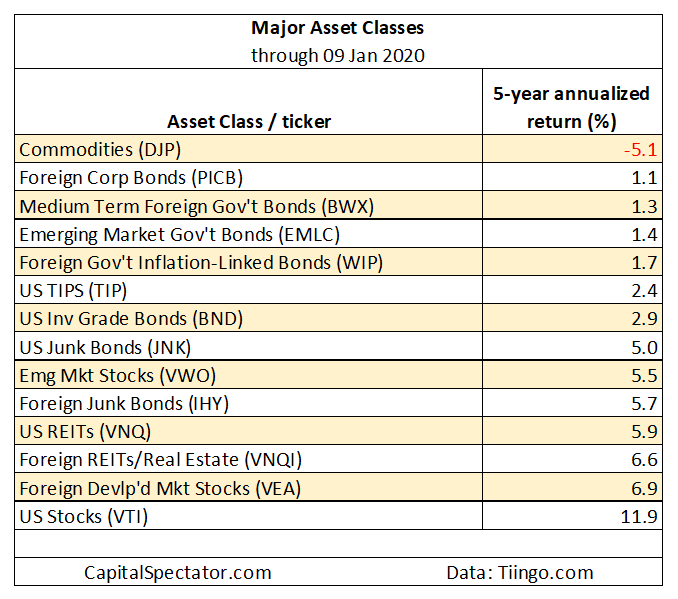

Let’s begin with the major asset classes for a big-picture profile. Echoing recent history, a broad definition of commodities continues to post the deepest shade of red for 5-year results. The iPath Bloomberg Commodity (DJP) – an exchange-trade note – has lost an annualized 5.1%. Otherwise, all the proxies for the major asset classes are posting varying degrees of gain for the trailing 5-year window.

Now let’s focus on the full list of funds, starting with the deepest 20 losses for all 135 ETFs. The biggest decline at the moment is in natural gas via United States Natural Gas Fund (UNG), which is down 22.2% on an annualized basis. The second deepest 5-year loss: shares in the oil and gas industry via SPDR S&P Oil & Gas Equipment & Services (XES), which has tumbled 19.9% annualized.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.