Confidence In The U.S., Confidence In The USD

Jeremy Cook | May 29, 2013 05:59AM ET

Everything seems to be turning up roses for the US economy at the moment, as another session was dominated by better than expected US data and a stronger US dollar. Home prices and consumer confidence, which rose to a 5yr high, both beat expectations and, coupled with the news that S&P had upgraded their rating of the US banking sector, the market was only going to travel one way.

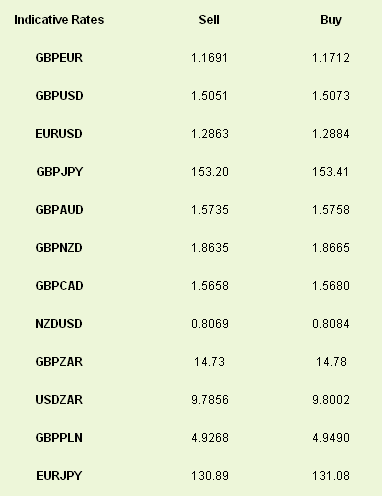

That exuberance has carried over into the Asian session overnight, with the USD continuing from where it left off. It seems almost obvious now that GBPUSD should test the years lows of around 1.48 with EURUSD under similar pressure towards its year-to-date low of 1.2750.

The commodity currencies continued to get hurt yesterday as fears over growth came to the fore. The main mover yesterday was South African which came in for a beating following further strikes by miners in recent months leading to a 7.1% fall in industrial production and a hit to growth that led to a below expectation GDP print of 1.9%. ZAR has lost 1.7% vs the pound in the past 36hrs as a result.

We forecast at the beginning of the year that the Aussie dollar was likely to be one of the ‘Dogs of 2012’ and overnight the currency has become a lot more canine. Poor construction data has caused local banks to revise GDP estimates lower while PIMCO, the world’s largest bond investor, called for another RBA rate cut sooner rather than later in a research note which came out this morning. AUDUSD is currently close to a 19 month high while GBPAUD is at an 8 month high.

Focus on Europe will likely dominate today with the European Commission delivering its evaluation of the budget plans of the EU-27 this morning. Today’s FT is leading on a story that France, Spain and the Netherlands are to be given a ‘waiver’ on the need to hit their 3% annual deficit limit. This could be a sea-change in the move away from austerity in the Eurozone, although the switch to growth is by no means as easy as limiting the discipline.

The shift away from austerity is designed to promote employment and we shall see this morning whether German divergence from the rest of Europe has continued as we get unemployment details for the month of May. The market is looking for unemployment to rise by 5k.

UK data is due in the form of CBI reported sales which, somewhat strangely, the market is expecting to increase. Labour market indicators have remained onerous of late and we would be very surprised if this has led to an increase in sales. A disappointment here could easily be the release that puts GBPUSD through 1.50.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.