China To Enact Policy Easing Due To Fears Of A Sharper Slowdown

Qatar National Bank | Dec 26, 2021 12:50AM ET

Despite the recent concerns about the COVID-19 Omicron variant, the global economic recovery remains strong and activity indicators in most advanced economies are comfortably within expansion territory.

In fact, a strong recovery, along with inflationary pressures, is already leading to a U-turn in the policy guidance of several central banks. Policymakers are moving from accommodation to “normalization” or even tightening. This even led to a more “hawkish” stance of the US Federal Reserve and the European Central Bank.

In contrast, China is experiencing a different macroeconomic, and therefore policy, dynamic. After a sudden collapse in demand and activity in Q1 2020, when China’s GDP contracted by 6.8% year-on-year, the country performed an impressive recovery that lasted from mid-2020 to mid-2021. China was the first and only large economy to present positive GDP growth last year, being ahead of other countries in the economic cycle by several quarters.

But the strong performance led to an early withdrawal of policy stimulus in China several months ago. On the fiscal side, policy tightened as tax relief measures expired, extraordinary social transfers moderated, and support for public investments dwindled.

On the monetary side, liquidity injection moderated significantly since Q4 2020. Money supply (M2) growth dropped to a lower rate than nominal GDP growth, which consequently implied a more restrictive monetary policy stance in the beginning of this year. Moreover, the government also started a comprehensive campaign to tighten regulation on the real estate and corporate sectors, dampening business sentiment and containing a more significant rebound in private investments since then.

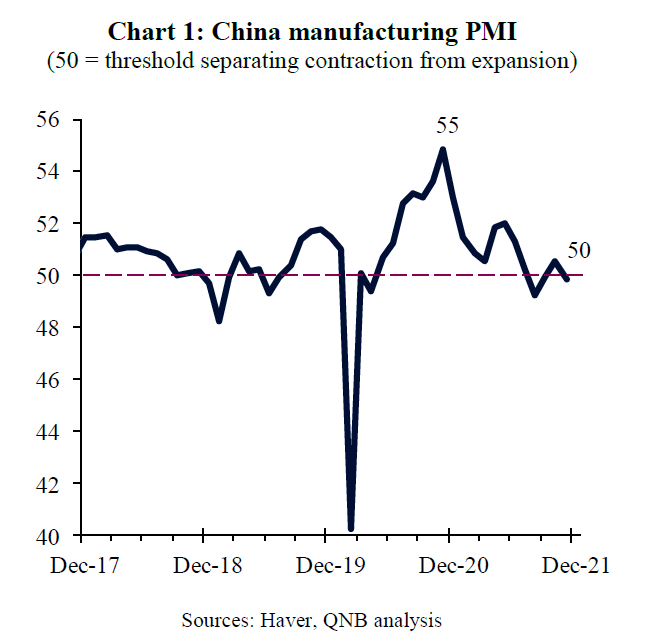

As a result, the recovery in China has been losing momentum more rapidly than in other major economies since Q2 2021. The manufacturing Purchasing Managers’ Index (PMI) of China, a survey-based indicator that measures whether several components of activity improved or deteriorated versus the previous month, peaked at 55 in November 2020, before a gradual slide towards 50 in November 2021 (Chart 1).

Traditionally, an index reading of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) changes in business conditions. In other words, higher frequency data is indicating that China activity is closing-in to contraction territory.

Sources: Haver,QNB analysis

In light of that, Chinese policymakers have already started to revert from policy tightening to policy easing. In recent weeks, the People’s Bank of China (PBOC) decided to cut the required reserve ratio (RRR) to a broader set of financial institutions by 50 basis points. The measure aims to increase support to the real economy, releasing RMB 1.2 trillion (about USD 190 Bn) to the banking system. This was only the first act of a more comprehensive cycle of easing measures e.g., more recently, the PBOC reduced its one-year loan prime rate by 5bp.

In our view, three factors support the “dovish” (supportive, accommodating) pivot of policymakers in China.

First, leading indicators are pointing to a sharper deceleration of growth in China over the coming months, in a movement that can make GDP growth drop below the expected policy target of “around 5%” for 2022. China’s credit impulse, an indicator that measures the relative thrust from social financing for real activity, leading other activity indicators by about 6-months, is pointing to a sharp deceleration of growth in China over the next semester (Chart 2). Stimulus measures are necessary to turn the credit story around towards a more supportive stance.

Sources: Haver, QNB analysis

Second, local COVID-19 outbreaks are becoming more frequent in China, which leads to the imposition of tighter social distancing measures and localized lockdowns. This is also starting to weigh on growth as outbreaks spur a drop in activity around the location where cases concentrate. The Chinese government maintains a “zero COVID-19” policy and is expected to continue to do so over the medium-term, deploying robust restriction measures against local outbreaks. The arrival of the Omicron variant in China adds another layer of complexity to this story, as localized outbreaks could become even more pervasive.

Third, COVID-19 related global supply constraints in several industries continue to have spill over effects in Chinese manufacturing, placing an additional cap on overall growth in the country. Supply constraints include low inventory levels as well as bottlenecks and other disruptions in manufacturing output and transportation infrastructure, such as ports, containers, and logistic networks.

We expect that supply constraints will only ease meaningfully by mid- to late-2022, the time when key industries are expected to be operating at normalized capacity. This will put a cap on China’s manufacturing growth for next year.

All in all, the PBOC decision to cut the RRR and lending rates, thus starting a new easing cycle, is justified by China’s significant slowdown as well as the challenges posed by COVID-19 outbreaks and supply constraints.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.