Capers Is a Ticking Time Bomb: Leverage Plus Loading Up on Nvidia

David I. Kranzler | Feb 20, 2024 12:03AM ET

Calpers – the California Public Employee Retirement System pension fund has borrowed 8% of its assets in order to load up on risky stocks. From the Financial Times: “Calpers, the largest pension plan in the US with $452bn in assets, had total fund leverage of 8 percent as of June 2023, which included what the fund described as “active” and “strategic” leverage.” “Strategic leverage?” Leverage is leverage and pension funds, with large, monthly fixed obligations, should not be using leverage to load up on risky equities. It may be borrowing even more money so to avoid having to sell part of its massive private equity holdings, some of which have no bid right now.

Sure, leverage works great as long as the stock bubble continues to inflate. But it’s a double-edged sword that has tendency to decapitate entities that abuse the leverage. I’ll confidently assert that Calpers’ use of leverage to load up on stocks like $NVDA is abusive, particularly since Calpers has monthly pension beneficiary cash outflows. Its private equity holdings, with a recklessly large allocation as a percentage of assets, are already worth far less than the amount Calpers invested. Calpers added 1.5 million shares of Nvidia (NASDAQ:NVDA) in Q4, giving it 7.5 million shares ($5.4 billion). This is an insane 1.2% of Calper’s assets. By the way, most public pension fund managers I’ve met are idiots.

Below is the latest update on NVDA excerpted from my latest bear newsletter. I also updated $SMCI after doing a deep dive the previous week.

Nvidia update (NVDA – $726) – Cisco (NASDAQ:CSCO) reported its FY 2024 Q2 numbers last week. Revenues declined 6% YoY and EPS was down 3%. The Company also cut full year and announced that it was cutting 5% of its workforce. I bring this up because, outside of corporate capex that has been spent on upgrading to AI hardware, there’s a general slowdown in the tech sector in both corporate capex spending and consumer electronics sales.

It’s also starting to look like AI chips will not be immune to a pullback in corporate spending. UBS published a report in which is said that lead times for NVDA’s H100 GPU for the 2H of 2024 are coming down: “Customer discussions confirm Nvidia’s lead times have come in substantially over the past few months, meaning shipment slots are still available in the 2H of 2024. This is interesting because, up until now, there’s been a supposed shortage of NVDA’s H100, which gave the Company some pricing power and fat profit margins. Companies like META (NASDAQ:META) and MSFT – plus the Chinese – likely bought what they needed for upgrade programs and are now busy deploying the hardware. Based on the UBS report, it would appear as if the initial rush to load up these chips has subsided.

40% of H100 GPU’s shipped are not yet in service as there is a lag to install the hardware and power up. Based on the number of AI chips already shipped, there is a lot of AI capacity. MSFT, META and AMZN account for 34.2% of NVDA’s revenues. All three are developing their own AI chips. In addition, AMD’s competing chip-set, the Mi300X, is going to start shipping in the 1H 2024. Finally, I would suggest that a material percentage of NVDA’s GPUs are going to the small, private companies that NVDA funds to enable them to buy chips from NVDA. It’s likely that many of these GPUs will never be deployed and show at big discounts on the resale market.

It thus would appear that supply and demand are coming back into balance. This will limit NVDA’s ability to dictate pricing and when competitive chips hit the market and the price wars will begin. A contact of mine who follows this stuff more closely than me explained that there is “an insane amount of [AI] capacity” for many applications that have yet to demonstrate profitability. As an example, I started toying with ChatGPT and Microsoft’s Copilot (which was forced on Windows users). While they make internet-based research faster and easier, I would not spend a dime to use them.

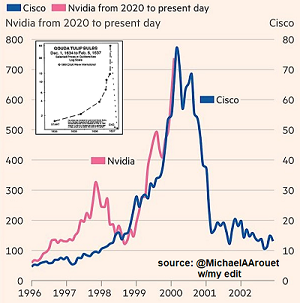

In the context of the chart path taken by bubble stocks (or tulips), a path that is consistent throughout history, I thought this analog chart comparing CSCO during the tech bubble and NVDA currently is interesting:

I don’t know that we can expect NVDA necessarily to crash the way CSCO did when the tech bubble popped, but I wouldn’t rule it out. For those who were not active in the market during the tech bubble, CSCO was billed as the backbone of internet build-out similar to the way now that NVDA is promoted as the king of AI chips. The dreamers and snake-oil salesmen conveniently overlook the fact that competition and obsolescence prevent a monopolistic tech product from achieving much more than a brief period of dominance. Between its all-time high in March 2000 and October 2002, CSCO lost 82% of its value. The stock price is still 41% below its all-time high. I would suggest that there’s a strong probability that NVDA will experience the same fate.

In that regard, the Financial Times published an article last week titled “Nvidia is nuts, when’s the crash?”. The article has a discounted cash flow analysis by an analyst from Chameleon Capital, a UK-based money management and investment banking firm. He noted that “to get to a $740 share price requires that the company maintain monopolist-like operating profit margin of 55% over the next decade, while growing sales ten-fold, from $60 billion/yr to more than $600 billion.” The entire semiconductor industry sold $527 billion worth of chips last year.

A big factor in the stock’s resilience is the $25 billion share buyback program it announced in August 2023. It has been aggressively buying shares in an effort to support the stock price. Instead of investing in future growth, and fending off competition, by deploying free cash flow into R&D, NVDA chooses to buy back shares and fertilize its ponzi-like scheme of “investing” in many unprofitable companies – many are supposedly data-center providers but have no customers – who turnaround and use the NVDA capital to buy H100 GPU’s from NVDA.

It feels like NVDA is finally starting to lose upside momentum. Last week I sat on my hands to prevent me from chasing NVDA higher with puts. But I think I’m going to start testing the waters again, likely with longer-date, deep OTM puts. As an example, I may start to accumulate July $550’s or September $500’s.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.