Canada Slides Into Recession

Wall Street Daily | Jul 22, 2015 07:32AM ET

My critics said I wasn’t educated. They said I didn’t understand the Canadian banking system. Some asserted that I had an agenda.

Indeed, my article from January 2015 about the tough times that lie ahead for Canada struck a nerve.

No one likes to be told that their home is overvalued or that the stocks they own are likely to fall.

To be clear, I have no hidden agenda and I’m not allowed to trade the securities I write about. I’m just trying to identify risks and, to some extent, predict the future.

At this point, we know that the Canadian economy has effectively entered a recession. Last week, the Bank of Canada (BoC) “unexpectedly” cut the benchmark lending rate to 0.5% and slashed its economic growth estimates for 2015. The BoC noted, “Real GDP is now projected to have contracted modestly in the first half of the year.”

Clearly, the decline in commodities prices is having a bigger impact than many expected. It boggles my mind when Canadians downplay the importance of natural resources for the Canadian economy. Yet even the Bank of Canada appears guilty, given its rosy economic projections at the beginning of the year.

The foreign exchange market has it right, in my opinion. The Canadian dollar hit its lowest level against the U.S. dollar since March 2009. Of course, the equity markets will be slow to grasp the enormity of the situation, as usual. However, the cracks are already starting to show.

Home Capital Group Inc. (TO:HCG), a large Canadian subprime lender, fell 19% on July 13 after the company reported that residential mortgage originations fell more than expected in the second quarter. The stock has declined over 30% year to date and is the worst performer of all Canadian financials this year.

As I’ve said in the past, the Canadian banking system will come under more stress, though I never said that Canadian bank stocks are going to zero. When I label something as “dangerous yield,” I mean that the relatively high dividend yield is insufficient to compensate you for the risk of holding the shares. A 4% dividend yield is a small consolation if the share price declines by 20%. You just lost the equivalent of five years of dividends.

If we’re looking for high yields, they’d better be safe. For this reason, Canadian financials are a “Sell.”

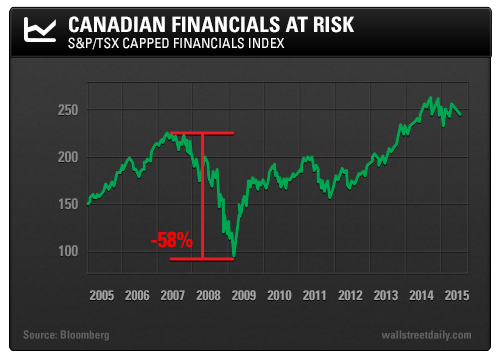

The S&P/TSX REIT Capped Financials Index, which is dominated by the large Canadian banks, fell 58% from 2007 to 2009. The Canadian banking system proved more sound than its U.S. counterpart, but investors in the Canadian financials still experienced an unacceptable drawdown.

There’s no telling how big the decline will be this time around. But based on the pushback we’ve seen from readers, it’s likely to be far larger than most investors want to believe. Also, hidden leverage and speculation will undoubtedly be uncovered, as usually occurs during recessions.

Furthermore, many investors harbor a naïve view that any and all lending is insured against losses by the Canadian government. If this were actually true, then the Canadian banks wouldn’t have provisions for credit losses (which will need to be increased).

The credit cycle has peaked in Canada, and credit availability will contract. In other words, it will become harder to obtain a loan – secured or unsecured, corporate or individual borrower. This will lead to more defaults and exacerbate the downturn. This deleveraging is ultimately a healthy, yet painful, process.

The situation in Canada will likely get painful enough that the Bank of Canada will be compelled to implement quantitative easing (QE). This will serve to dull the pain and prop up financial asset prices, but it’ll also halt the necessary deleveraging.

Perhaps every central bank in the world will be conducting QE stimulus before the global debt supercycle peaks.

Safe (and high-yield) investing,

Original post

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.