Bond Market Noise Masks a Golden Buying Opportunity

Michael Lebowitz | Oct 18, 2023 06:28AM ET

Treasury yield levels are overwhelmingly a function of inflation. However, in the short run, a plethora of influences can explain deviations between yields and inflation. These factors, which we call noise, are significant for short-term traders but can hide tremendous opportunities for long-term investors.

As we witness, bond market noise can be deafening. The horror-ridden narratives explaining the sudden rise in yields are compelling. They can steer even the best traders away from a golden opportunity.

For those bullish on bonds, separating the noise from the signal is difficult. But, doing so allows you to alleviate short-term stress when bond prices move adversely. Additionally, it helps maintain confidence in long-term fundamental prognostications.

This article discusses one of our favored bond fair value models to show you the true bond yield signal.

The signal is the meaningful information that you’re actually trying to detect. The noise is the random, unwanted variation or fluctuation that interferes with the signal. – Conceptually

What Is Noise?

Market noise is the primary determinant of hour-to-hour and day-to-day price changes. While it is very important for short-term direction, its influence often wanes quickly.

Today, there are a plethora of concerning narratives explaining why bond yields are rising. At first glance, they make a lot of sense and should be worrying. However, if you take the time to research them, you will find many recent bond market narratives are insignificant temporary noise.

Noise can be separated into real noise and false narratives.

Real Noise

Real noise are influences that changes the demand and or supply of bonds.

For instance, risk premium describes investors’ preferences for longer-maturity bonds versus rolling over a series of short-term bonds. These preferences matter, but trends in the risk premium are well correlated with inflation and inflation expectations. As such, our signal, inflation, catches this noise.

Another example is the Fed. Through managing the Fed Funds rate and doing QE or QT, they affect the supply of and/or demand for bonds. However, monetary policy effects will also show up in our inflation signal.

A recent illustration is the flight to quality trade to U.S. Treasury bonds due to the Israeli-Hamas war. The demand spurt will likely be short-lived as investors begin to acclimate to the situation.

However, oil-driven inflationary concerns may arise if the war proliferates to Iran or other oil-producing countries. Again, this will show up in our inflation signal.

False Narratives

False narratives are meaningless noise. These are stories market pundits tell to justify market actions. False narratives can certainly move the bond market in the short term, but their shelf life is often minimal.

We expose a current false narrative in our recent Daily Commentary. To wit:

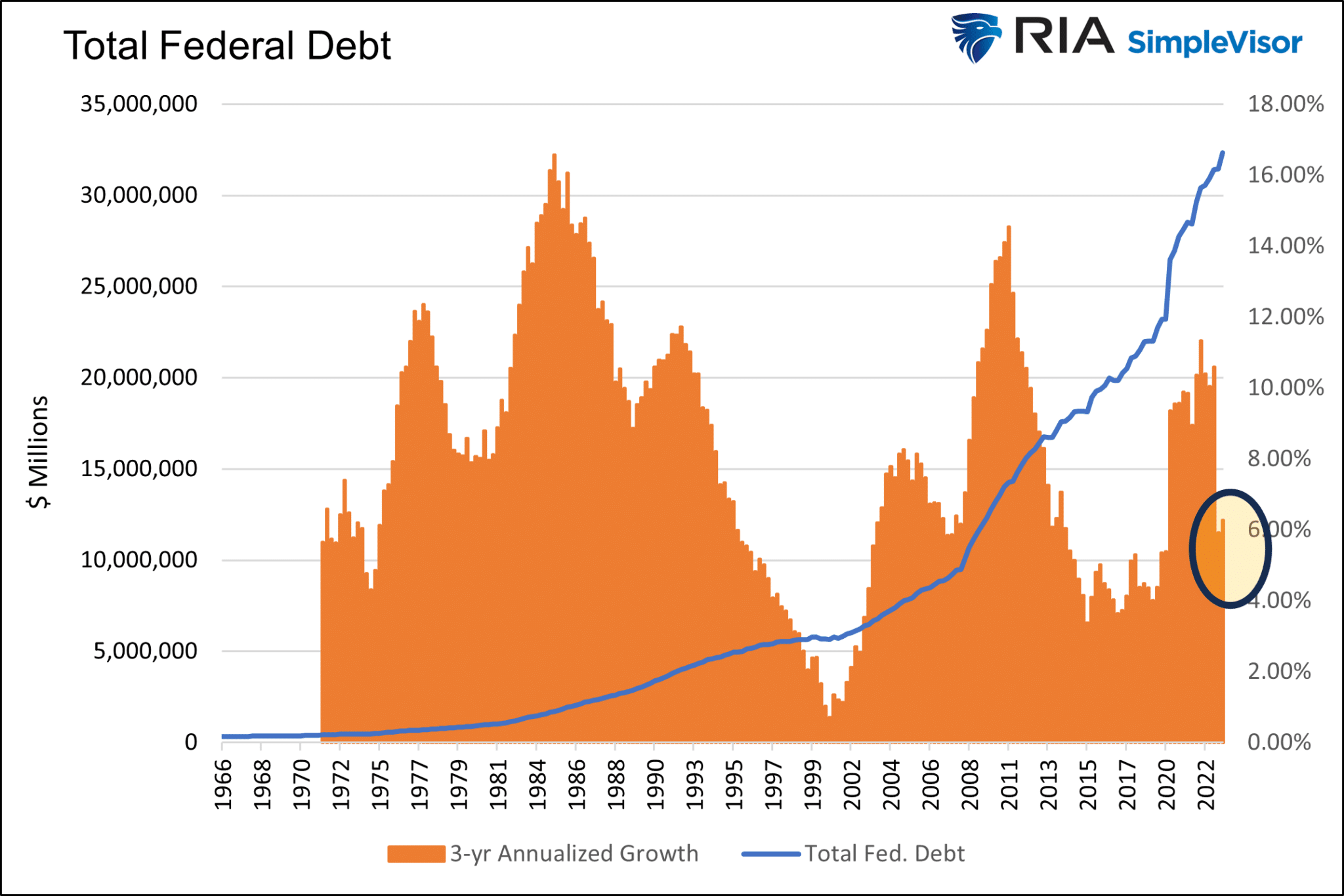

Listening to the media or Twitter, one might think Treasury debt issuance over the last six months is off the charts. Such stories are far from the truth when looked at from the right perspective. Consider the graphs below. The top left graph shows federal debt is growing slightly faster than the pre-pandemic years but well below prior surges.

The right chart puts debt growth on a log scale to show the current growth rate is actually slightly below the trend of the last fifty years. Lastly, the bottom graph shows the sharp increase in debt to GDP during the pandemic. However, it has declined since. A high debt-to-GDP ratio, as we have, is very problematic. But false narratives claiming recent issuance is well above average are flat-out wrong.

The recent sell-off in bond prices and increasing yields is not due to “massive” Treasury debt issuance. Nor is it due to China, Japan, or other nations selling our bonds. The reason is noise.

The Signal: Inflation Drives Yields

The true signal guiding bond yields is inflation. When combined with current yield levels, we have found that a combination of actual inflation data, market-implied breakeven inflation rates, and surveys of inflation expectations are extremely well correlated with yields.

After comparing economic and inflation data with bond yields, we have observed that the Cleveland Fed’s Inflation Expectation Index is far and away the best predictor of yields. Per the Cleveland Fed:

How we get our estimates: Our estimates are calculated with a model that uses Treasury yields, inflation data, inflation swaps, and survey-based measures of inflation expectations.

Our Fair Value Model

The monthly scatter plot below shows that since 1990, ten-year yields and the Cleveland Fed Inflation Expectations Index, which is also ten years, have an R-squared of .966. Simply, 97% of Treasury bond yields are explainable by the Index. As you can see, the current yield (green) lies about 1% above the trend line. Ergo, current yields are about 1% above fair value.

The following graph uses a line graph to compare our regression model (dotted line above) to actual yields. As it shows, they track each with precision. However, the green and red differential bars show bond yields can deviate from the model’s fair value calculation. As we highlight, the increase in the difference, or noise, has grown since 2008. It is likely due to the Fed’s bond-buying activities.

The current deviation is the largest since at least 1990!

Fair Value Model Predictions

Our fair value model not only tells us how much noise the bond market is pricing in but also allows us to forecast future fair value yields based on our own inflation expectations projections.

The regression trend line in the scatter plot (black dotted line) is defined by the circled formula. It calculates where yields should be based on the Cleveland Fed Index.

The slope of the regression line is 2.77x. Each 1% change in inflation expectations should result in a yield change of 2.77% in the same direction.

The current inflation expectation is 2.21%. If you think expectations will eventually return to average pre-pandemic levels (1.65% – 2017-2019), the fair value ten-year yield falls to 2.09%.

With current yields around 4.60%, a turnaround to fair value would generate a 20%+ return on a ten-year note plus nearly 5% a year in coupon payments.

What If Inflation Expectations Rise

Thus far, we have made a bullish case for bonds, assuming the Cleveland Fed Inflation Expectations Index remains at the current level or declines.

We would be remiss if we did not discuss what happens if inflation expectations increase.

Current yields will be at fair value if inflation expectations rise by about half a percent. For every one percent that expectations rise after that, we should expect yields to increase by 2.77%.

Let’s put some context around that. Inflation expectations at the recent peak were 2.45% or about .25% above current levels.

Therefore, a full one percent increase is highly unlikely, especially given that many supply and demand imbalances that led to higher inflation have largely dissipated.

Further, if inflation expectations start rising consistently, the Fed will increase interest rates and all but assure a recession and disinflation or deflation.

It’s also worth noting that elevated rental and house prices (aka shelter) keep CPI well above where it should be. We say “should be” because real-time market shelter prices are falling.

As the arrows in the graph below highlight, shelter should continue to decline, catching up with actual prices. With it, about 40% of CPI will be dragged lower.

Summary

The noise in the bond market is thunderous these days as inflation is still well above norms, deficits remain high, and the Fed continues to promise higher rates for longer. Noise creates differences between the yield on bonds and their true fair value.

Noise is hard to ignore, but it can create tremendous opportunities!

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.