3 Ways to Retire on Dividends in 2023

Contrarian Outlook | Dec 28, 2022 04:10AM ET

A terrible 2022 is our income threat. There’s never been a better time to retire on dividends than right now.

Today we’re going to spotlight three diversified dividend funds that yield 8% on average. That’s right, put $500K into these tickers, and we’re looking at $40,000 per year in payouts.

Or $80,000 on a million. You get the idea. This is what I call a secure 8% “No Withdrawal” Portfolio where we get to retire on dividend income alone, without ever touching our capital. (The strategy has become so popular that Tom Jacobs and I wrote a book on it!)

No Withdrawal Fixes Wall Street’s Flawed Advice

In past decades, a big nest egg was enough to retire on. And a plain vanilla strategy like the “4% withdrawal rule” would help it last for decades.

The 4% strategy says that someone with a million-dollar portfolio can withdraw $40,000 annually. And no matter the market’s swoops and swoons, the money would last for at least 33 years.

So a 60-year-old with a million could call it a career, pull out $40,000 annually, and be good until at least 93. Not bad.

The 4% rule creator William Bengen, an MIT grad and all-around smart guy, found that a 50-50 mix (or so) of stocks and bonds was a sound approach. It made most nest eggs last. The earliest an egg would “crack” was 33 years in.

At least, this was according to the 50-year period that Bengen analyzed. Our challenge is that 2022 is a dumpster fire. Bond values are under pressure because long interest rates are up. Stock prices are falling as the Federal Reserve takes its party punch bowl away and replaces it with kale smoothies.

Bengen himself is nine years into retirement—and he concedes he’s “not comfortable.” The MIT grad admitted this to the Wall Street Journal, adding that he’s cutting back on restaurants.

Billy B.! Ditch your own rule and follow us. We, contrarians, don’t limit ourselves to a bland mix of conventional stocks and bonds. We demand secure dividend streams—like this energy toll bridge.

1. Energy Toll Bridge Pays 8.1%

Alerian MLP ETF (NYSE:AMLP) is a fund that owns infrastructure companies—middle persons that take their own tolls. They are generally less sensitive to energy prices than producers like Exxon Mobil (NYSE:XOM).

As long as energy prices merely grind sideways, these toll bridges keep collecting. Which means the dividends continue.

AMLP just boosted its dividend. It now pays $0.75 per share, good for an elite 8.1% yield.

Some of the individual stocks that AMLP owns pay even more. But be careful! Most will send you a complicated K-1 tax form—if you own them outside the fund.

My accountant nearly broke up with me years ago when I handed him two K-1s from these toll bridges. I thought I was just buying a couple of stocks. To him, I had joined two partnerships. Messy.

Never again, I promised him. Which is why we chose AMLP. No K-1!

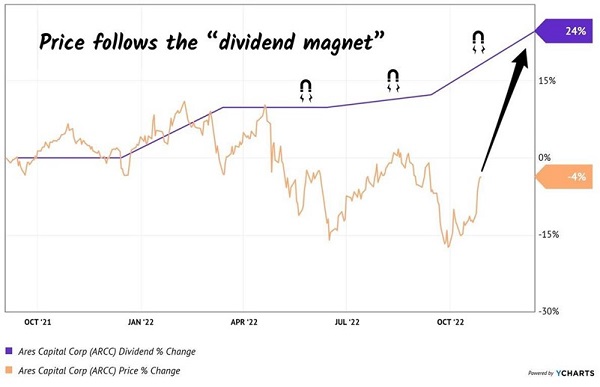

2. “BDC Bully” ARCC Dishes 10.5%

Ares Capital Corporation (NASDAQ:ARCC) is a business development company (BDC). It was already the biggest BDC on the block. (in that “bad is good” way) after displaying the audacity to be open in a year when its competitors were essentially closed.

ARCC is a “rich guy favorite” because it pays a lot, and it bullies around its competition. And the great thing about being a bully? Dividend raises.

Not only does ARCC yield a terrific 10.5% but the firm just hiked its payout by 12%. Here we see ARCC’s “dividend magnet” starting to pull its “slow to follow” share price higher:

ARCC Poised to Pop

The knee-jerk reaction from vanilla window shoppers is that ARCC is going to struggle if we slip into a recession. Well, this is obviously not happening as fast as the mainstream media thought it would.

Much to the Fed’s chagrin, the economy is still humming!

As long as the economy chugs along or even muddles through, ARCC is out there lending. Remember it is the lender of choice in the BDC space. Price gains are likely from here thanks to its rising dividend.

3. Recession-Resistant Landlord Yields 5.4%

W P Carey Inc (NYSE:WPC) is an industrial landlord. The company leases out business space to individual tenants. Its portfolio is diversified across 1,216 properties, with its largest tenant (U-Haul) making up just 3.4% of its total portfolio.

Virtually all (99%) of WPC’s leases include contractual rent increases. The majority of them are linked to the consumer price index (CPI), which is a nice hedge for those of us who are concerned about inflation down the road.

CEO Jason Fox and his team are among the best in the industrial real estate business. They raise WPC’s dividend every single quarter. We welcome this landlord into our retirement portfolio any day.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, "7 Great Dividend Growth Stocks for a Secure Retirement ."

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.