2016: Not The Start We Expected

Brian Gilmartin | Jan 14, 2016 12:22AM ET

The S&P 500 fell 2.5% yesterday, and is down 5% in the last week.

With the S&P 500 down about 7.5% YTD already, needless to say, this wasn’t the start expected to 2016.

At a Chicago CFA Society luncheon yesterday, Jason Trennert, the managing partner of Strategas Research Partners, noted he thought the S&P 500 would be up 10% in 2016, exactly what I was thinking here in mid to late December ’15.

With JP Morgan (N:JPM) and Intel (O:INTC) set to report this today, finally, Q4 ’15 earnings and ’16 guidance aren’t just a guess.

So what’s been a surprise so far in 2016 ?

- Freeport (N:FCX) looks like it is going bankrupt, the way it is trading. Jason Trennert mentioned yesterday we might see one major energy sector bankruptcy before this correction ends. Chesapeake (N:CHK)? Freeport? Peabody (N:BTU)? (All my suggestions, not Jason’s).

- Neither Value nor Growth is working this year. The FANG stocks have gotten crushed. Amazon (O:AMZN) is down $100 from its all time, late December ’15, high. The stock is testing its upward sloping trendline off the ’15 low. It needs to hold here.

- Back in the bull market of the 1990’s, there used to be a graph or chart that circulated that showed that bear market bottoms were put in usually when a big Financial blew up. Continental Bank in the mid 80’s, Drexel Burnham in 1990, Orange County and the Mexico devaluation in late 1994 may not have been bear market finales but they typically marked the end of major corrections. Could be something like that is looming today, in another sector.

- The dollar index closed at 98.94 yesterday. Hasn't changed much as all and in fact is still under its March ’15 multi-year high near 100. A steady dollar or a lower dollar is still, “net-net” a positive in my opinion.

- Banks and Financials have gotten just hammered YTD, possibly due to the flatter yield curve. I do think Financials offer good value here. Corporate loan growth should be decent. When we hear from JP Morgan, Wells Fargo (N:WFC), Citigroup (N:C), and US Bancorp (N:USB), it will give us a good look at the consumer and corporate loan books.

- The Russell 2000 is down over 20% from its all time highs. That is a real bear market.

- The iShares iBoxx $ High Yield Corporate Bond ETF (N:HYG) has not made a new 52-week low even with the equity carnage.

Our only change to portfolios thus far this year is to sell the Brazil ETF (iShares MSCI Brazil Capped (N:EWZ)) and depending on the client, some Energy exposure, both of which was added in October ’15.

Clients have no exposure to the Russell 2000 or to biotechs (those two are related), Transports, Basic Materials, and have just a 3%-4% exposure to Emerging Markets (Long some Vanguard FTSE Emerging Markets (N:VWO) and iShares MSCI Emerging Markets (N:EEM)) and Energy (Energy Select Sector SPDR (N:XLE) and iShares US Energy (N:IYE)), and yet I still feel pretty stupid.

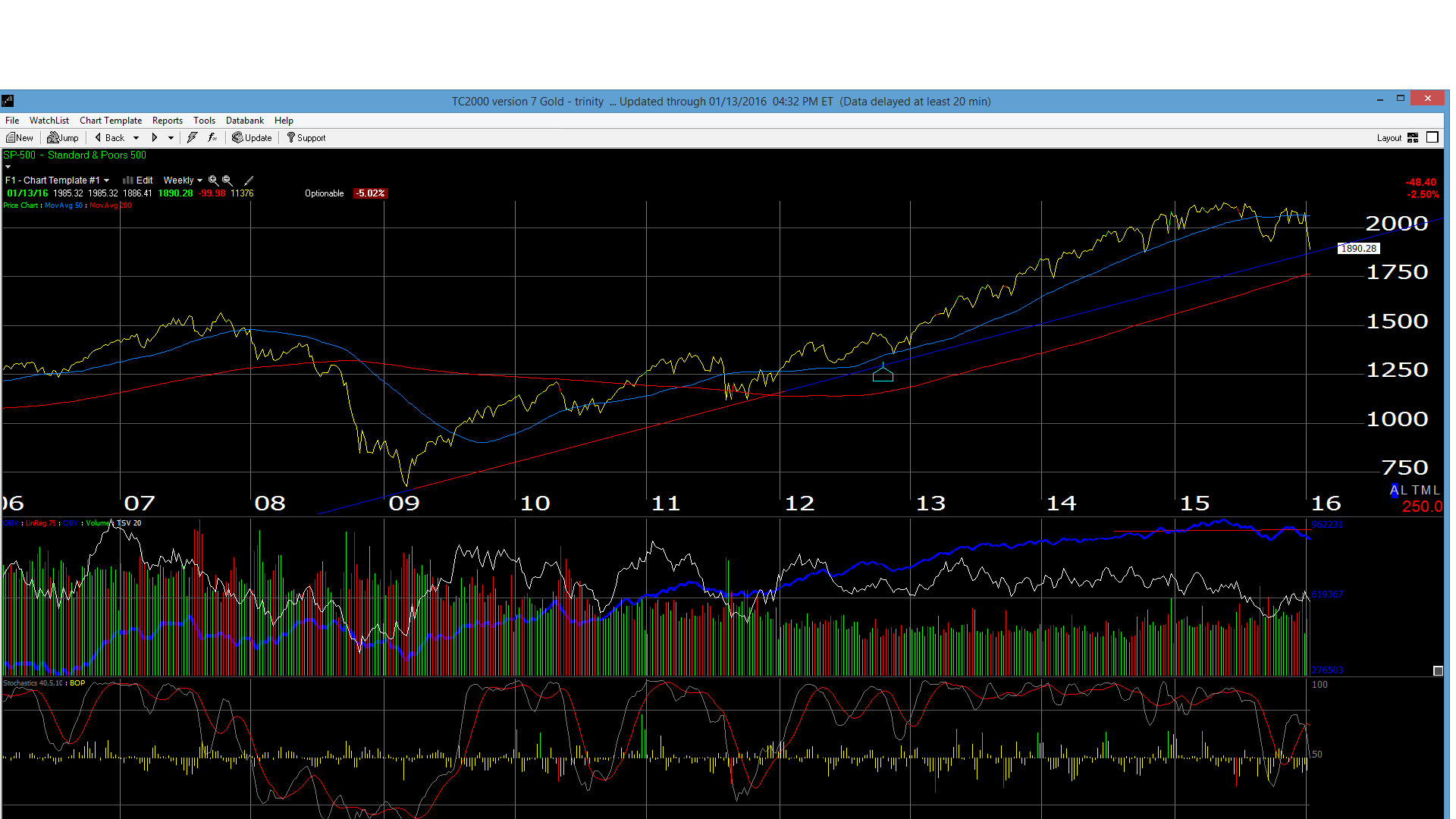

We’ll leave readers with one chart. Some technicians think the August ’15 lows of 1,867 could be tested now. The overnight futures low in August ’15 was 1,831. Note the 200-week moving average on the chart above, near 1,750.

We'll get a great look at the big bank earnings over the next two days. Read the conference call notes.

![]()

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.