Intel shares surge as SoftBank Group agrees to invest $2bln in chipmaker

The coming week is shaping up to be another crucial one for gauging recession risks and monetary policy paths. It’s NFP week in the United States and the RBA and Bank of England will decide whether to accelerate their hiking cycles. The ISM PMIs are bound to attract a lot of attention as well in the US as growth concerns intensify. Elsewhere, employment figures in Canada and New Zealand, and manufacturing PMIs out of China will be the highlights. Meanwhile, a meeting of OPEC+ countries might yet result in a decision to produce more oil.

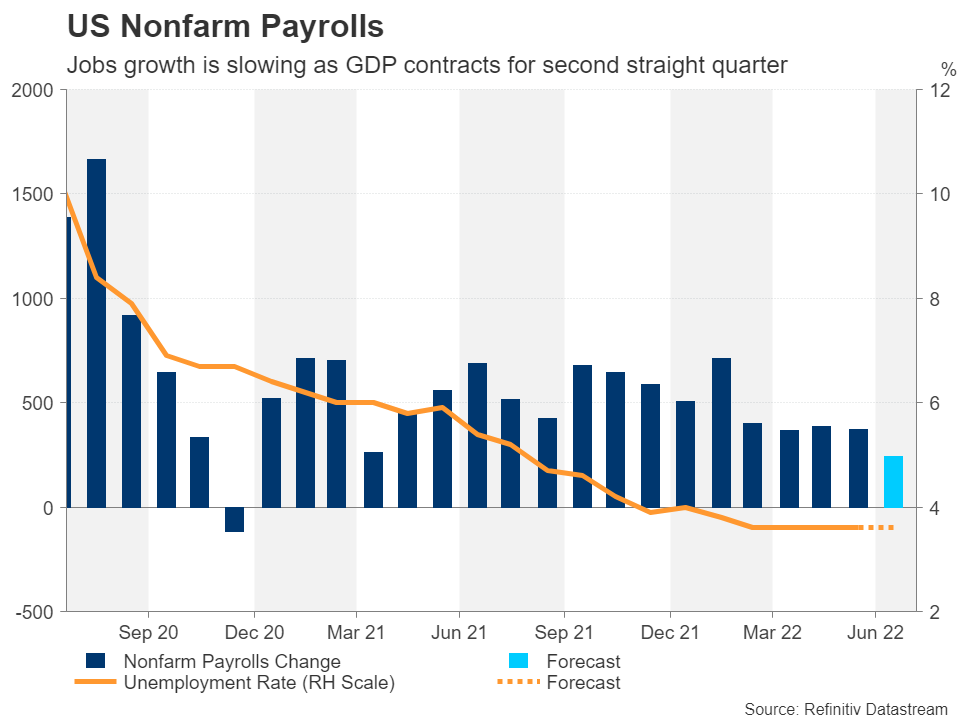

US jobs report eyed as Fed admits economy is slowing

US jobs report eyed as Fed admits economy is slowing

The US economy is officially in a technical recession after GDP shrank in both the first and second quarters. But by its own definition, the Fed does not see a broad-based decline in economic activity as there appears to be several pockets of growth still. Moreover, the strong jobs growth and wage pressures are “not consistent with a recession” according to Chair Jerome Powell.

Nevertheless, there can be no doubt that hiring is slowing and if the latest earnings season is any indication, some companies have even started to lay off staff. But on balance, the economy continues to churn out more new jobs than what is being lost. The forecast for Friday’s nonfarm payrolls print is 250k in July versus 372k in June.

The jobless rate and growth in average hourly earnings are expected to have held unchanged at 3.6% and 0.3% m/m, respectively, in July.

However, the NFP report will not be the only thing at the top of investors’ agenda as the ISM manufacturing and non-manufacturing PMIs, due on Monday and Wednesday, respectively, will also be watched closely for further evidence of a cooling economy.

If worse-than-expected readings are complemented by a drop in the ISM’s prices paid component, the markets might not react too adversely to poor data. Powell hinted in his post-meeting press conference that the Fed will slow down its rate hikes at some point. Although the timing isn’t clear, tightening bets have been pared back notably, boosting risk assets but knocking down the US dollar. A soft batch of numbers could further lift stocks and weigh on the greenback.

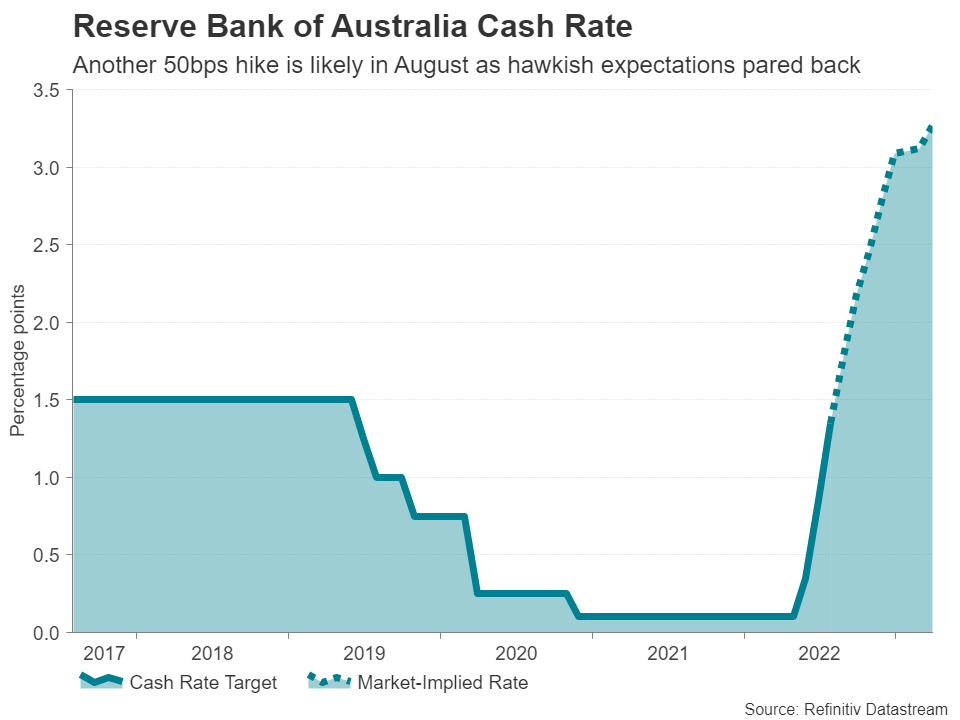

RBA to stay the course

The Reserve Bank of Australia will kick off next week’s two central bank meetings on Tuesday and a fourth straight rate increase is on the cards. After raising rates by 50 basis points at the last two meetings, there was some speculation that the RBA would get more aggressive in July and hike by 75 bps. However, following the Fed’s not so hawkish tone at July’s FOMC meeting and weaker-than-forecast inflation in Australia in the second quarter, investors now expect the RBA will stick with 50-bps increments.

But as long as the greenback stays subdued, the absence of a hawkish surprise by the RBA will probably not hurt the Australian dollar much. The aussie could even gain if Governor Philip Lowe keeps the option of bigger hikes on the table. The bank’s quarterly economic projections, which are due on Friday, could also bolster the aussie if the forecasts for CPI are revised higher.

Aussie traders will also be keeping an eye on Chinese PMIs. China’s official and Caixin manufacturing PMIs are both released on Monday and are not predicted to point to much of a quickening of the rebound from the lockdown-induced contraction in the spring. Any disappointment in the PMIs poses a downside risk for the aussie.

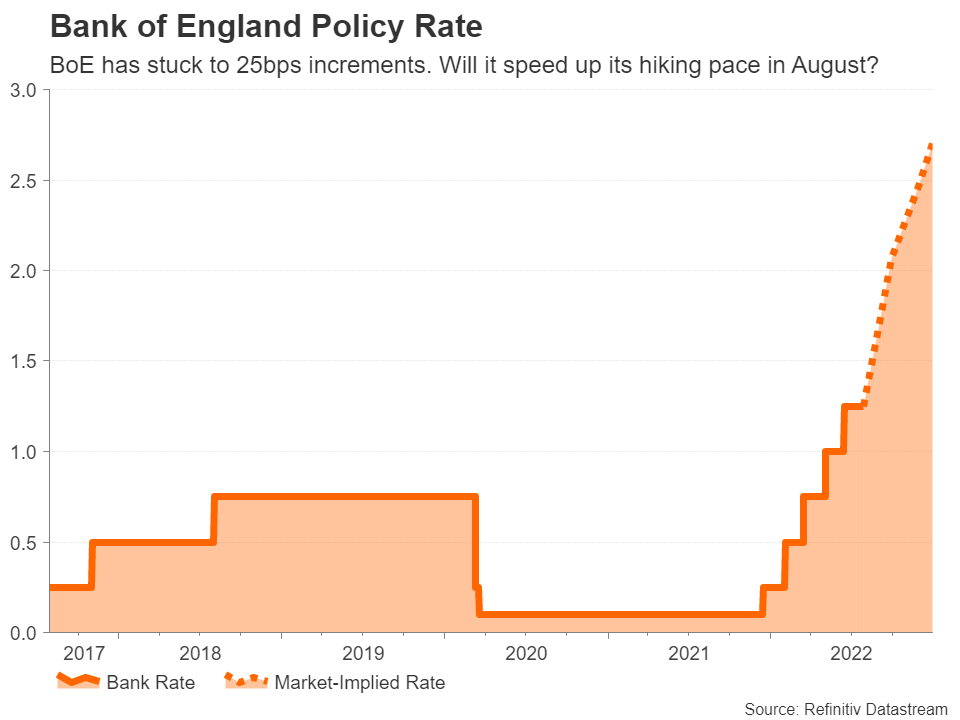

Will BoE join the 50-bps club?

The Bank of England may have been one of the first major central banks to start lifting borrowing costs, but it has been doing so at a pace of 25-bps increments. This could change in August as UK inflation is fast approaching 10% despite having raised rates at every meeting since December. BoE policymakers have been a lot more cautious than their global counterparts as they expect higher prices to do part of the job of denting demand for them. But the fact that most of the price pressures are stemming from supply-side factors – something that central banks have no control over – is also why the BoE hasn’t pressed on the brakes too hard.

However, with the labour market still going strong and PMI surveys not yet showing a contraction for the UK economy, policymakers will likely come to the conclusion that a larger increase may be necessary this time, as flagged by Governor Andrew Bailey.

If the BoE does go ahead with a 50-bps hike and signals that it could repeat this at one or more of the remaining meetings of the year, sterling could extend its current rebound against the US dollar. On the other hand, if Bailey suggests that the double hike was a one off and the BoE’s quarterly forecasts paint an even gloomier picture than they already do, the pound’s upswing will be put to the test.

Jobs in focus in Canada and New Zealand too

Other economies enjoying the phenomenon of a tight labour market are Canada’s and New Zealand’s. But unlike the UK, their central banks have been a lot more aggressive. Investors expect at least two more 50-bps rate increases from the Bank of Canada and the Reserve Bank of New Zealand and the upcoming employment reports are not anticipated to have a significant bearing on those probabilities.

New Zealand’s quarterly jobs numbers are up first on Wednesday and Canada’s will follow on Friday.

With the greenback being worse off after the Fed meeting, the local dollars might appreciate from better-than-expected employment figures.

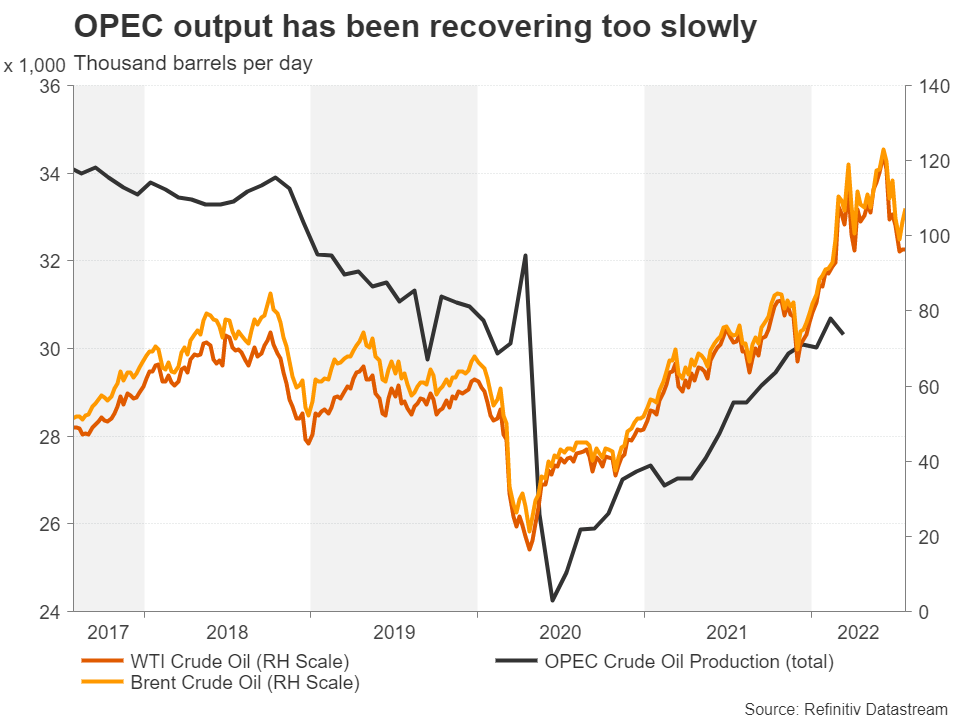

OPEC might raise output

For the Canadian dollar, traders will also be keeping an eye on OPEC’s monthly meeting on Wednesday.

There’s a chance that OPEC and non-OPEC producers may decide to raise their production quotas, extending the planned output increases beyond September.

Saudi Arabia, OPEC’s de facto leader, has so far refused to pump additional oil as requested by the White House. But following President Biden’s trip to the kingdom in July, it’s possible that Saudi Arabia will push other members for a further supply boost.

Should OPEC+ announce a new deal that involves substantially higher output rather than merely a symbolic increase, oil prices are likely to come under pressure as a big move is not being widely anticipated.