Nvidia becomes first company to reach $4 trillion market cap amid AI boom

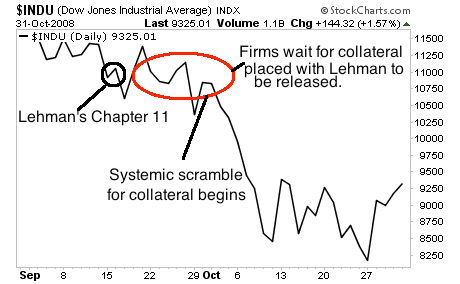

Countless pages have been written about why Lehman caused the system to almost implode. However, the reality is that Lehman nearly took down the entire financial system for two reasons:

- Lehman’s $155 billion worth of bonds were used as collateral in hundreds of billions of Dollars’ worth of trades.

- Lehman’s 8,000 clients who were all using Lehman to make trades saw the collateral that they had placed with the firm (to backstop their portfolios) frozen.

The below story reveals that both Bank of America and Dubai’s sovereign wealth fund both saw collateral frozen when Lehman went bust. I can assure you many other big names were caught in a similar situation.

Lehman: One Big Derivatives Mess

It turns out that Lehman, like other big dealers, was running a perfectly legal but highly risky game moving money from firm to firm. It used the collateral from one trading partner to fund more deals with other firms. The same $100 million collected in one deal can be used for many other transactions. “Firms basically can use [the money] as their own collateral for anything they want,” says Kenneth Kettering, a former derivatives lawyer and currently a professor at New York Law School. But when the contracts terminate as the result of bankruptcy, the extra collateral is supposed to be returned.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

As part of those transactions, buyers had put up collateral in the event of losses. But weeks after Lehman’s demise, large sums of leftover collateral have yet to be returned to the trading partners. Bank of America (BAC) executives tried several times to persuade Lehman officials via e-mail and phone calls to fork over funds, according to a suit. But BofA was rebuffed. In one e-mail exchange, a Lehman employee wrote to BofA: “All activity has been suspended until further notice.”

Nasreen Bulos, a lawyer for one of Dubai’s sovereign wealth funds, got the same chilly response. The Global Strategic Equities Fund of Dubai, part of the gulf state’s $12 billion investment portfolio, gave Lehman $40 million in June as part of a deal pegged to energy giant BP’s (BP) stock. According to an affidavit, Bulos started contacting Lehman on Sept. 15 to get back $27 million in collateral. Four days later, Lehman told Bulos it would not honor the request or say anything further on the matter.

Source: Bloomberg Businessweek

Normally, a client’s collateral would be unfrozen soon after the bankruptcy of a broker dealer. In Lehman’s case it wasn’t. And that, combined with Lehman’s $155 billion worth of bonds becoming worthless, created a severe collateral shortfall in the system.

This is why the market held together for a little over a week after Lehman went bust: the players who had collateral with Lehman thought they’d get the money freed. When they didn’t, the system imploded as collateral calls were issued. What followed was widespread liquidation as banks did everything they could to free up capital to meet funding needs or to buy new higher grade collateral (hence the skyrocketing rally in Treasuries at the time).

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

This is the reality of what happened in 2008, though few know it. And this is why a default in Spain or Italy (whose €1.78 and €1.87 trillion in sovereign bonds are collateral for likely more than €100 trillion in trades) would bring about a collapse that would make Lehman appear minor in comparison.

Remember, if Spain goes bust, they over €1 trillion in collateral would vanish triggering a chain reaction in at least €50 trillion if not €100+ trillion in trades at the large banks/ financial institutions.

Again, and I cannot stress this enough: when Spain defaults (and it will) the system will experience a collateral crunch that will be exponentially higher than that which occurred following the Lehman bankruptcy.

This is why I’ve been warning that the 2008 was just a warm-up. It’s why the Powers That Be in Europe are absolutely terrified of what’s happening there. And it’s why those investors who do not prepare in advance for what’s coming will lose everything.

If you do not want to be one of them, you need to get moving.

Which stock should you buy in your very next trade?

AI computing powers are changing the stock market. Investing.com's ProPicks AI includes 6 winning stock portfolios chosen by our advanced AI. In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. Which stock will be the next to soar?

Unlock ProPicks AI