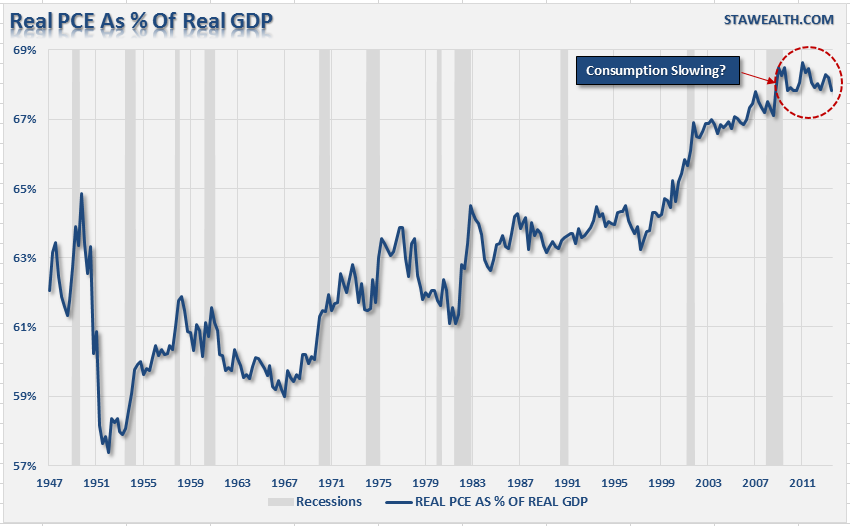

There has been much debate in Washington about how to get the economy growing again. Unfortunately, fiscal policy has done little to address the core of economic growth, which is the consumer, or the productive investment required to generate real employment and wage growth. Currently, real (inflation adjusted) personal consumption expenditures make up 67.82% of real gross domestic product as of the third quarter of 2013. This is currently at the same level as seen in 2010.

In a consumption based economy, fiscal policy measures should be focused solely on job creation which inevitably leads to higher levels of consumption. The problem currently is that the fiscal policies that have been foisted upon the economy since the financial crisis have stifled job creation more than encouraging it. As I stated in the latest review of the NFIB survey:

"Business owners are some of the best allocators of capital and resources. They spend money to increase production, expand facilities and hire employees to meet increasing demand. They operate within the confines of the real economic environment, rather than theory, and artificially inflated asset prices does little to increase consumptive capacity for a vast majority of Americans that live paycheck to paycheck."

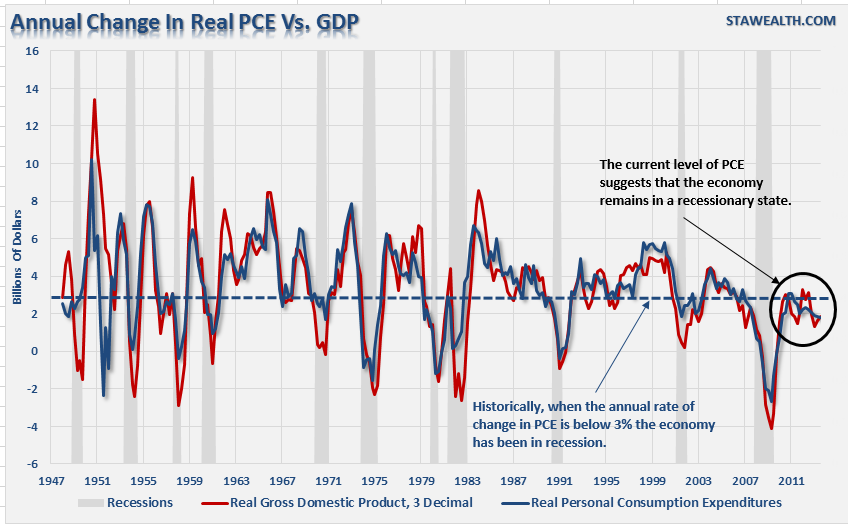

This is clearly shown in the chart below which is the annual rate of change in real GDP as compared to real PCE.

While the monetary interventions of the Federal Reserve have lifted asset prices since the end of the financial crisis; there has been little translation into the real underlying economy. As the chart above shows, PCE is currently at levels that have historically been associated with economic recessions. This is why when you look at many economic and confidence indicators, while improved, they are still at levels normally associated with recessionary trends.

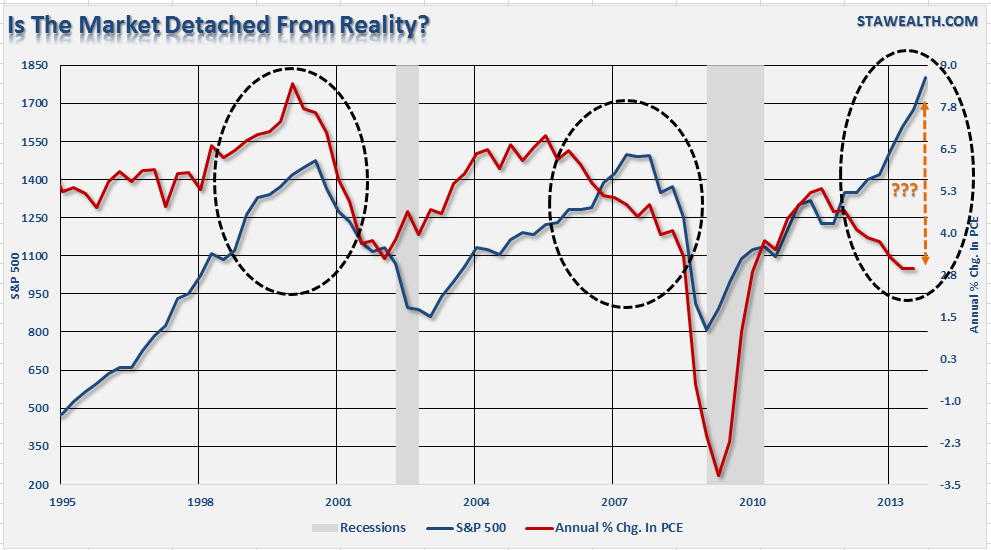

As stated above, the Federal Reserve's interventions have inflated asset prices which have been a boon to the top 20% of the economy that actually have investible assets but has left a large swath of Americans unaffected. The chart below shows the current detachment of the S&P 500 from PCE which clearly shows the issue.

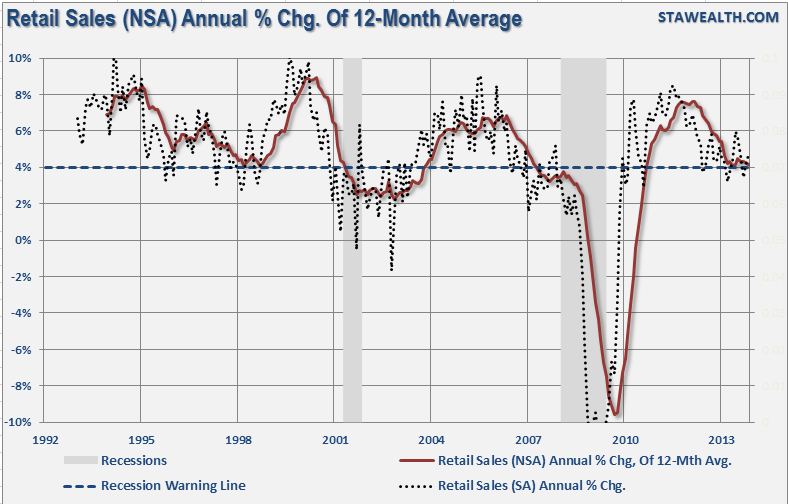

The retail sales figures for November did NOT improve this analysis despite the media's excitement over a better than expected headline number. The report showed that, ex-automobiles, retail sales for November rose 0.4%. The problem with any single data point is that it obscures the trend of the data, as shown in the chart below, which is more telling of the overall strength or weakness of the consumer. [Note: retail sales make up roughly 40% of the PCE calculation]

The chart above is the 12-month average of non-seasonally adjusted retail sales data. This eliminates all of the questionable gimmickry of the seasonal adjustments to reveal the underlying trend of actual retail sales data. Surging asset prices have done little to boost retail sales which have stagnated in recent months just above the level which has normally been indicative of recessionary drags in the economy. We saw a similar occurrence of this in 1998 which did ultimately turn up as the "tech bubble" spurred many startup internet companies leading to real employment gains. This is not the case currently.

With consumption making up such a large part of economic growth, there seems to be little attention paid to the drivers that support it. While the current administration has focused on restructuring healthcare, increasing the regulatory requirements on businesses and increasing the working population by legalizing illegal immigrants; there have been few efforts to reduce taxes, increase productive investment opportunities or clear the uncertainty that currently stifles business owners.

John Tamny, Real Clear Markets, just recently penned an article stating:

"Indeed, as Joseph Schumpeter long ago observed, and his observation was a tautology, there are no entrepreneurs without capital. Taking Schumpeter's basic insight even further, it's stating the obvious to assert that there are no companies, and no jobs, without investment first. For anyone irrespective of ideology to deny the latter brings new meaning to willful blindness.

So once the obvious is accepted, that companies need investment in order to open for business and hire people, we then can ask where investment comes from. It comes from all of us who save and invest, but the rich, by virtue of being rich, have the most to invest. Investment is what creates jobs, rich people can claim the vast majority of investable wealth in this country, and because they can it's another tautology to say that their savings and investment create the vast majority of jobs."

The important point here is that until we focus on creating an environment that leads to greater investment opportunities by business owners we will likely see a further deterioration in personal consumption. There is currently a fine line between expansion and contraction within the overall economy, and while hopes are that 2014 will be a "breakout" year for the economy, the current economic data trends suggest otherwise.

Which stock should you buy in your very next trade?

With valuations skyrocketing in 2024, many investors are uneasy putting more money into stocks. Unsure where to invest next? Get access to our proven portfolios and discover high-potential opportunities.

In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. That's an impressive track record.

With portfolios tailored for Dow stocks, S&P stocks, Tech stocks, and Mid Cap stocks, you can explore various wealth-building strategies.